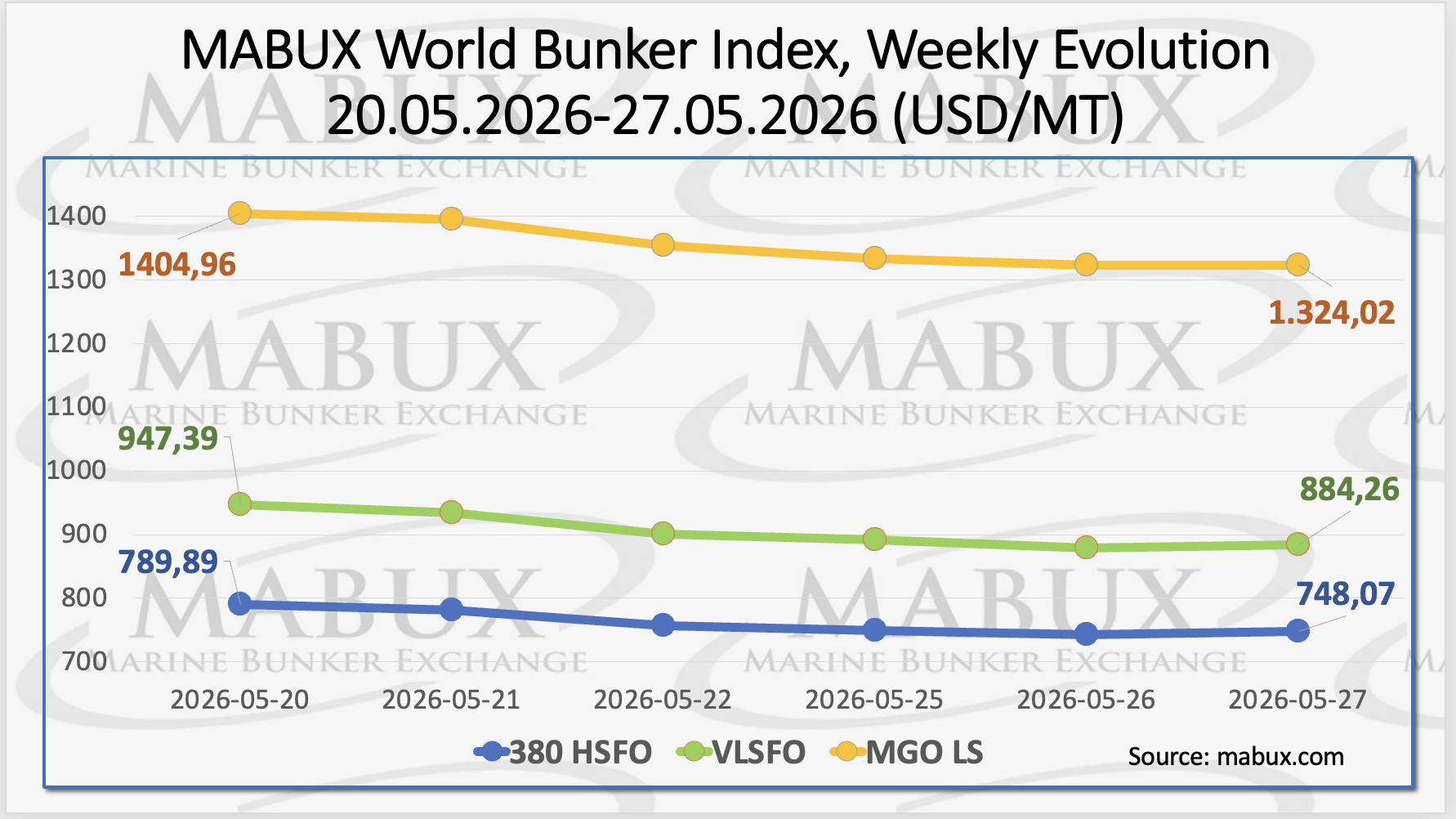

The global bunker market moved downward during Week 22, 2026, amid reports of a possible peace agreement between the US and Iran, Sergey Ivanov, Director at MABUX, noted.

By the end of the week, the 380 HSFO index had fallen by US$41.82, declining from US$789.89/MT last week to US$748.07/MT. The VLSFO index decreased by US$63.13, reaching US$884.26/MT compared with US$947.39/MT the previous week, breaking below the US$900.00 mark. Meanwhile, the MGO LS index dropped by US$80.94, falling from US$1,404.96/MT to US$1,324.02/MT, moving below US$1,400.00 and approaching US$1,300.00.

At the time of writing, Ivanov explained that the market remained in a phase of multidirectional fluctuations.

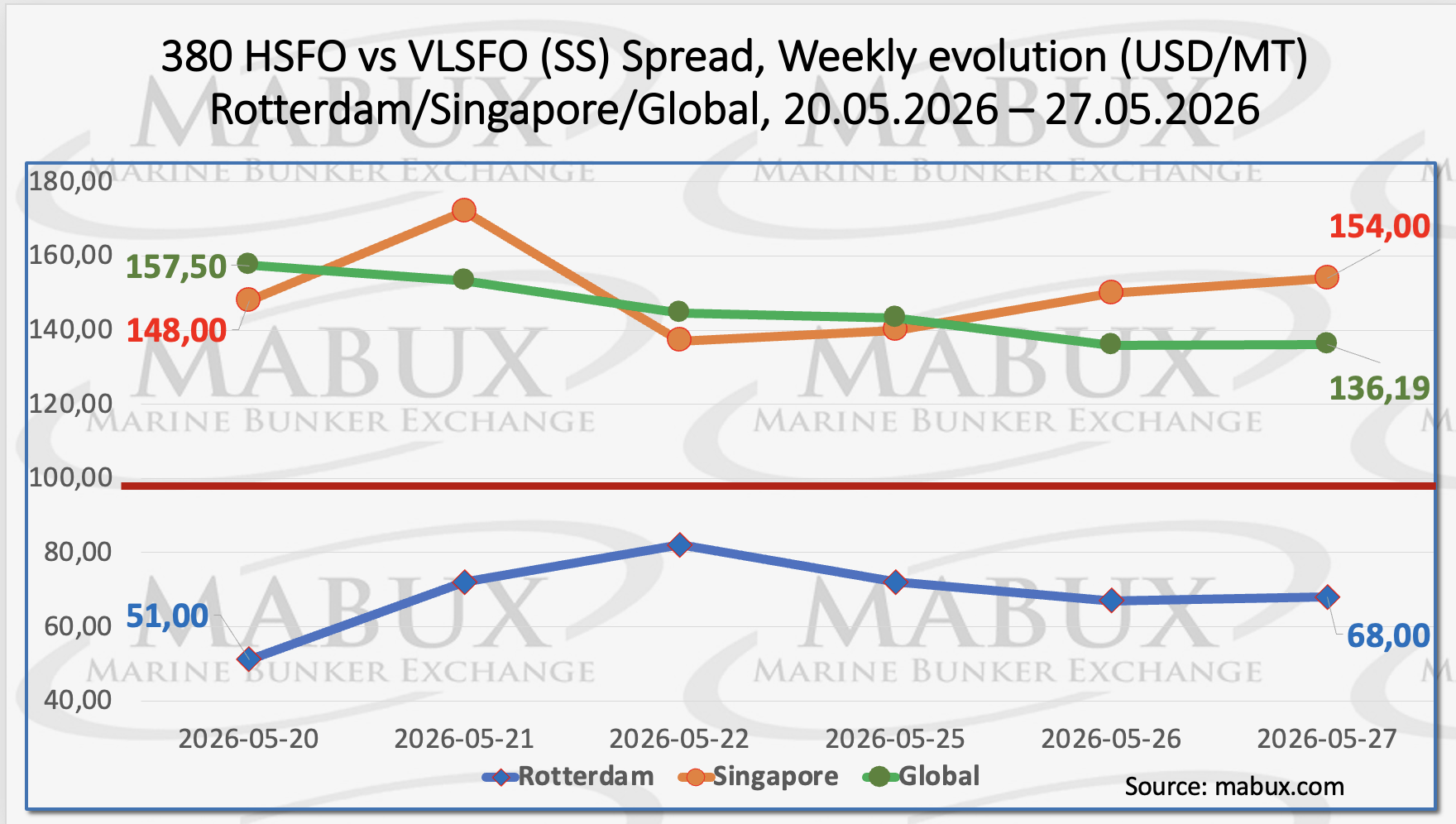

The MABUX Global Scrubber Spread (SS), representing the price differential between 380 HSFO and VLSFO, continued to narrow during the week, declining by a further US$21.31 from US$157.50 last week to US$136.19. Despite the decrease, the spread remained comfortably above the psychological US$100.00 breakeven threshold. The weekly average of the index also fell by US$18.09.

In Rotterdam, the SS Spread moved in the opposite direction, increasing by US$17.00 from US$51.00 last week to US$68.00, while its weekly average declined by US$9.83. In Singapore, the 380 HSFO/VLSFO spread widened by US$6.00, rising from US$148.00 last week to US$154.00, although the port’s weekly average edged down by US$2.50.

Overall, Ivanov commented that the SS Spread remained relatively stable throughout the week, preserving the broader trend toward improved scrubber cost-efficiency when using 380 HSFO compared to conventional VLSFO. He added that mixed movements in the SS Spread are expected to persist in the near term amid continued uncertainty surrounding the Middle East conflict and elevated market volatility.

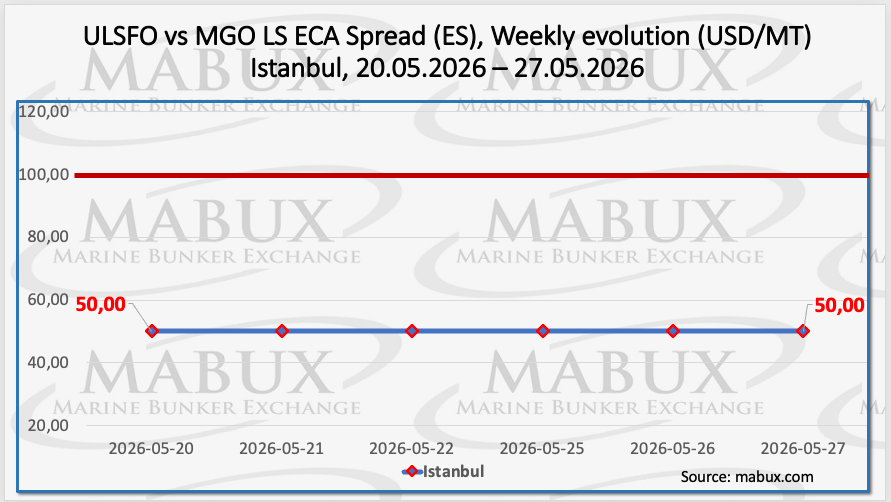

The Istanbul ECA Spread (ES) remained unchanged at US$50.00 during the week, while its weekly average declined by US$28.33. The Venice ECA Spread remains uncalculated due to the absence of regular market quotations. Amid the ongoing holiday period in Turkey, the MABUX director said he expects the ECA Spread to remain relatively stable next week.

American LNG suppliers are urging the EU to delay enforcement of methane emissions rules until at least 2028, warning that regulatory uncertainty is already slowing long-term gas contracting at a critical stage for the market.

Under the EU methane law, gas imports from 2027 must either meet monitoring and verification standards equivalent to those in Europe or comply with strict certification requirements. The regulation remains a central element of the EU’s climate agenda.

The rules have faced mounting industry criticism in recent months. Earlier this year, oil and gas companies, including major European firms, called on Brussels to suspend implementation, warning that the measures could disrupt fuel imports and undermine supply security.

The level of natural gas reserves in European underground storage facilities continued to increase moderately as of May 26, reaching 38.52% of total capacity, up by 1.85 percentage points compared to the previous week. Nevertheless, the pace of injections remains relatively weak, with storage occupancy still 22.94% below the level recorded at the beginning of the year, when reserves stood at 61.46%.

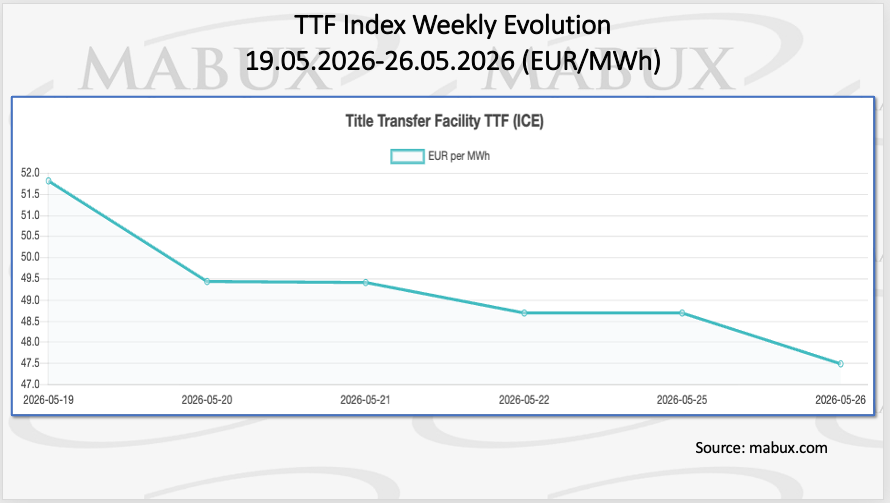

At the end of Week 22, the European gas benchmark TTF declined by EUR 4.344/MWh, falling from EUR 51.816/MWh last week to EUR 47.472/MWh.

The price of LNG as a bunker fuel at the port of Sines, Portugal, declined further this week, falling by US$115.00 to US$1,094/MT compared to US$1,209/MT the previous week. At the same time, the price spread between LNG and conventional fuel widened to US$169.00 in favour of LNG, versus US$96.00 a week earlier. On May 25, MGO LS was assessed at US$1,263/MT at the port of Sines.

Discussing LNG pricing trends, Ivanov noted that the widening spread increasingly favours LNG over conventional fuel in Sines.

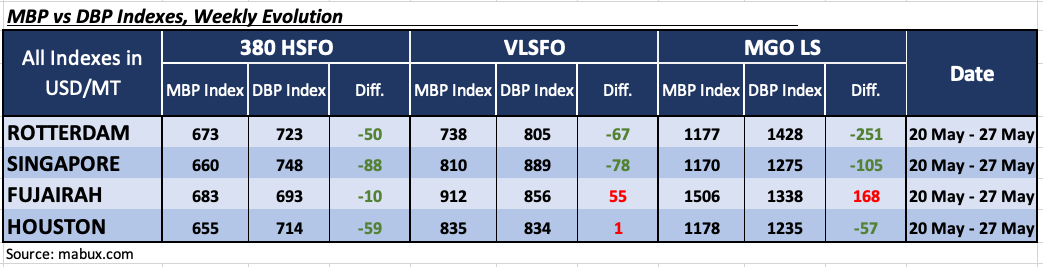

The Week 22 MABUX Market Differential Index (MDI), which measures the ratio between Market Bunker Prices (MBP) and the MABUX Digital Bunker Benchmark (DBP), recorded varying trends across Rotterdam, Singapore, Fujairah and Houston.

In the 380 HSFO segment, all four ports remained in the undervalued zone. The level of discount widened by one point in Rotterdam and by two points in Singapore, while narrowing by 22 points in Fujairah and by 37 points in Houston. Notably, Fujairah’s MDI approached the 100% correlation level between MBP and DBP.

In the VLSFO segment, Houston moved into the overvalued zone, joining Fujairah. The overpricing premium increased by 45 points in Fujairah and by 40 points in Houston, with Houston remaining close to the 100% MBP/DBP correlation mark. Rotterdam and Singapore continued to be undervalued, although the MDI discount widened by 12 points in Rotterdam and narrowed by two points in Singapore.

In the MGO LS segment, Rotterdam, Singapore and Houston remained undervalued. MDI levels increased by 132 points in Rotterdam and by two points in Singapore, while declining by four points in Houston. Fujairah continued to be the only overvalued port in this fuel category, with its premium increasing by a further 17 points. MDI values in Rotterdam, Singapore and Fujairah remained consistently above the US$100.00 level.

Overall, the balance between overvalued and undervalued ports shifted slightly further toward overvaluation during the week, as Houston entered the overvalued zone in the VLSFO segment. Nevertheless, Ivanov stated that this development did not alter the broader DBP trend, where multidirectional fluctuations continue to dominate amid elevated market volatility.

The market continues to be influenced by two opposing factors. Reports about a possible peace agreement in the Middle East are putting pressure on prices, raising expectations for more stable traffic through the Strait of Hormuz. At the same time, ongoing geopolitical tensions and limited military activity near the strait continue to support prices, highlighting the uncertainty surrounding the current ceasefire.

Against this backdrop, Ivanov expects mixed movements in global bunker indices to continue in the near term, with high market volatility likely to persist.