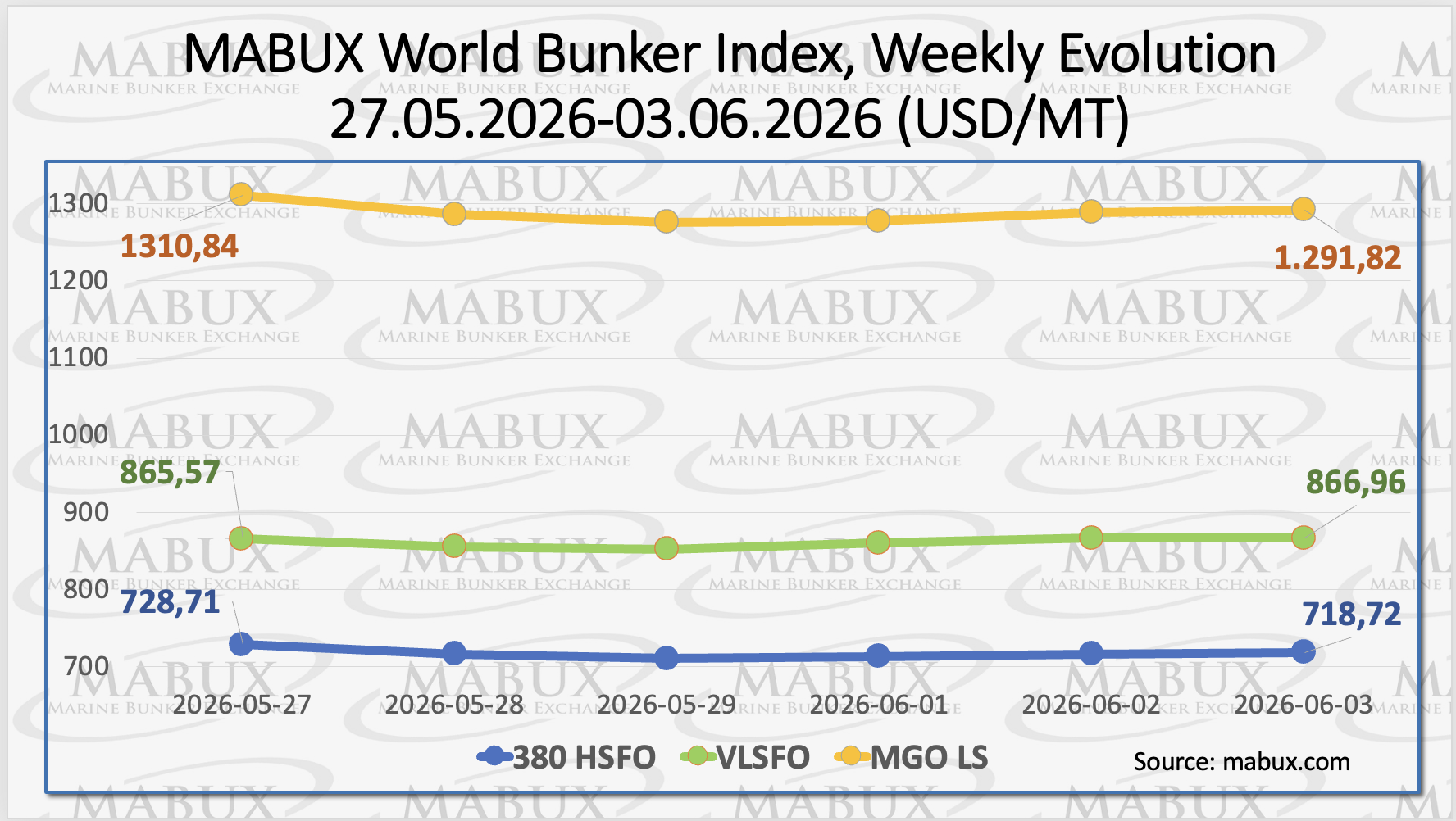

The global bunker market remained volatile during Week 23, with fuel indices moving in different directions amid ongoing uncertainty surrounding prospects for a resolution of the conflict in the Middle East, Sergey Ivanov, Director at MABUX, noted.

The MABUX 380 HSFO Index declined by US$9.99, falling from US$728.71/MT last week to US$718.72/MT. In contrast, the MABUX VLSFO Index posted a modest gain of US$1.39, rising from US$865.57/MT to US$866.96/MT.

Meanwhile, the MABUX MGO LS Index decreased by US$13.02, dropping from US$1,304.84/MT to US$1,291.82/MT and falling below the US$1,300.00/MT threshold for the first time since March 6, 2026.

At the time of writing, Ivanov explained that bunker fuel prices were showing signs of renewed upward momentum, suggesting a potential recovery phase following the week’s mixed performance.

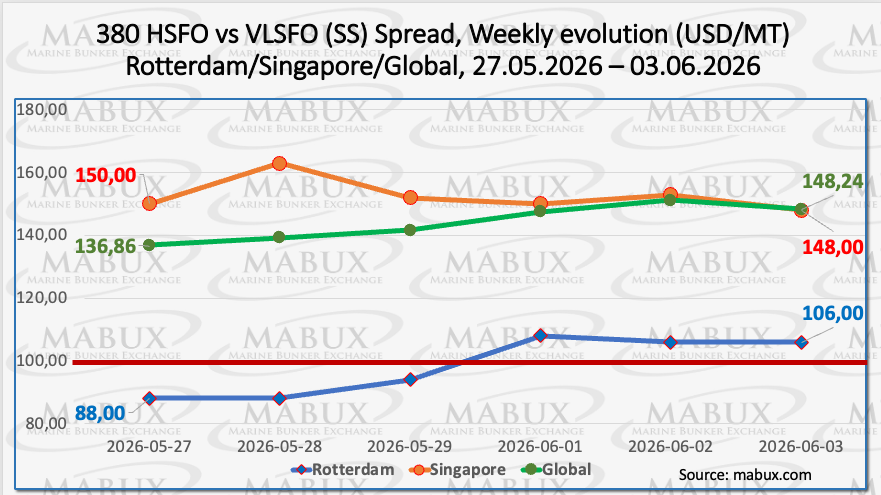

The MABUX Global Scrubber Spread (SS) — the price differential between 380 HSFO and VLSFO — widened by US$11.38 during the week, increasing from US$136.86 to US$148.24. The index continued its upward trajectory, approaching the US$150.00 mark and remaining comfortably above the key breakeven threshold of US$100.00.

At the same time, the weekly average of the Global SS Spread edged down marginally by US$0.98.

In Rotterdam, the SS Spread gained a further US$18.00, rising from US$88.00 last week to US$106.00 and once again moving above the US$100.00 level. The port’s weekly average SS Spread increased significantly by US$29.66, reflecting improving scrubber economics.

By contrast, in Singapore, the 380 HSFO/VLSFO differential narrowed slightly by US$2.00, declining from US$150.00 to US$148.00. Nevertheless, the weekly average SS Spread in the port increased by US$2.50.

Although regional dynamics remained mixed, the Global SS Spread demonstrated overall stability throughout the week and consistently held above the US$100.00 breakeven level. This continued to support the economic advantage of operating vessels equipped with scrubbers and consuming 380 HSFO rather than conventional VLSFO.

Looking ahead, Ivanov expects the SS Spread to remain subject to mixed fluctuations in the near term, driven by persistent uncertainty surrounding the Middle East conflict and elevated volatility across global energy and bunker fuel markets.

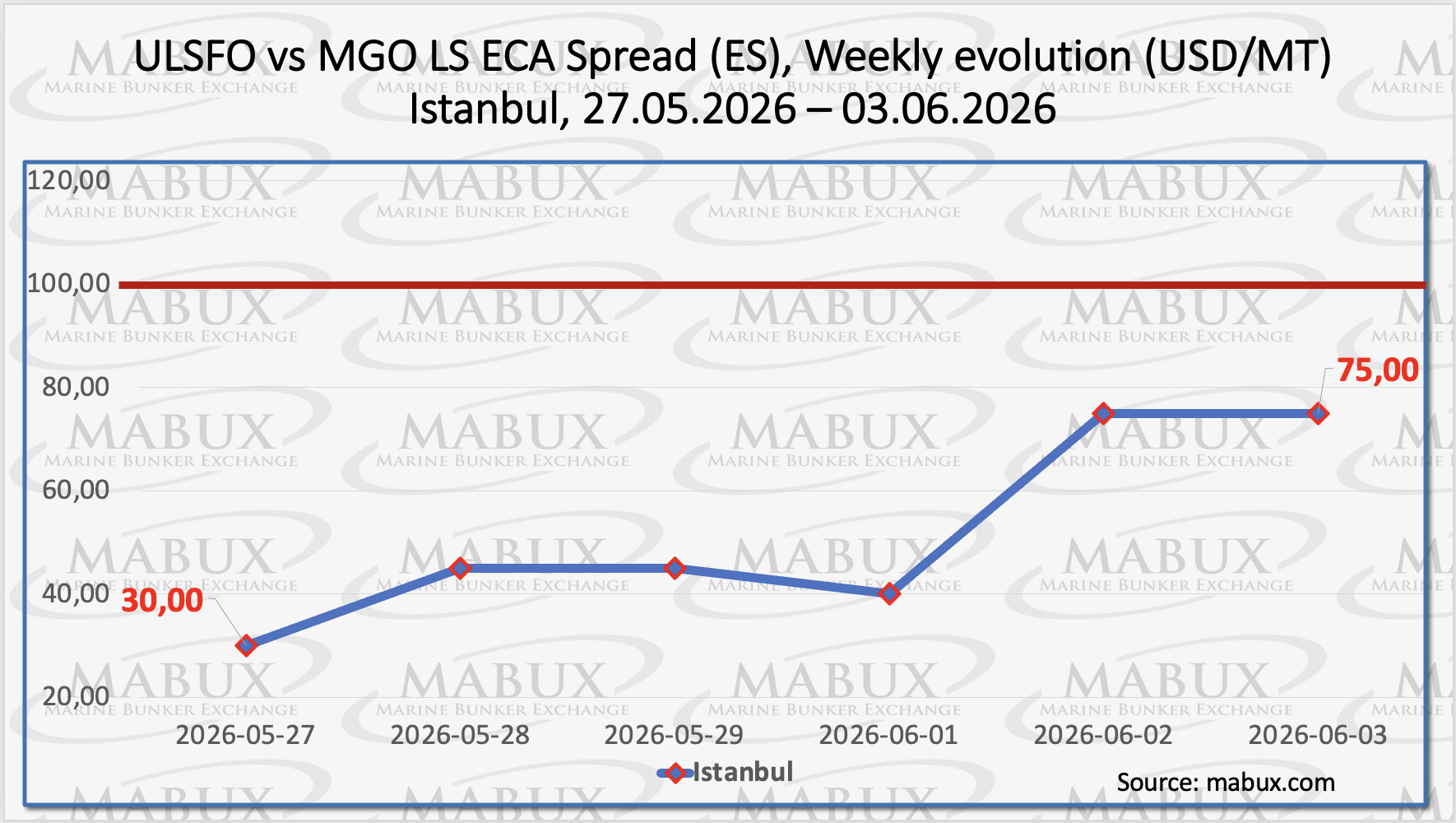

The Istanbul ECA Spread (ES) ended the week with a strong increase of US$45.00, rising from US$30.00 last week to US$75.00. The index continued to recover from recent lows, gradually moving toward the US$100.00 level, while its weekly average increased by US$1.67.

The Venice ECA Spread remains unavailable due to the continued lack of regular market quotations required for index calculation.

Given recent signs of market stabilisation, Ivanov said he expects the ECA Spread to maintain upward momentum in the coming week, although its direction will remain dependent on broader developments in the bunker fuel market.

Europe entered the current gas injection season with unusually low inventories after a prolonged winter, with storage facilities only 28% full at the start of the refill period. As a result, Europe faces a growing risk of falling short of its typical winter readiness target of 90% storage capacity.

Under EU regulations, member states are expected to maintain storage levels in the 80–90% range before the start of the heating season.

According to Equinor, a rapid resolution of current supply disruptions could still allow Europe to reach a manageable storage level of around 75% by the end of the injection season. However, a disruption lasting one to three months would significantly tighten the market and could push TTF gas prices toward €90/MWh.

Higher gas prices would likely trigger demand-side adjustments, including an estimated 10 bcm reduction in gas-fired power generation demand and increased fuel switching by industrial consumers.

As of June 2, gas inventories in European underground storage facilities continued their gradual recovery, reaching 40.76% of total capacity. This represents an increase of 2.24 percentage points compared to the previous week.

Nevertheless, storage levels remain 20.70 percentage points below those recorded at the beginning of the year (61.46%) and continue to lag significantly behind the seasonal norm of 50%.

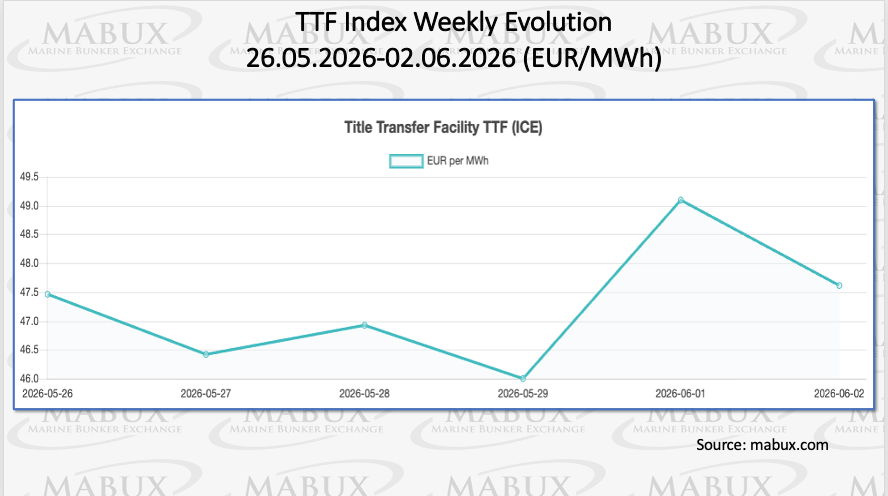

Meanwhile, the European gas benchmark TTF remained largely stable during Week 23. The index edged up by just EUR 0.135/MWh, increasing from EUR 47.472/MWh the previous week to EUR 47.607/MWh.

The price of LNG as a bunker fuel at the port of Sines, Portugal, increased by US$5.00 again this week, reaching US$1,099/MT compared to US$1,094/MT last week.

Meanwhile, the price difference between LNG and conventional fuel narrowed to US$32 in favour of LNG, compared with US$169 the week before. MGO LS was quoted at US$1,131/MT at the port of Sines on June 1.

Ivanov noted that the narrowing spread indicates changing economics between LNG and conventional marine fuels.

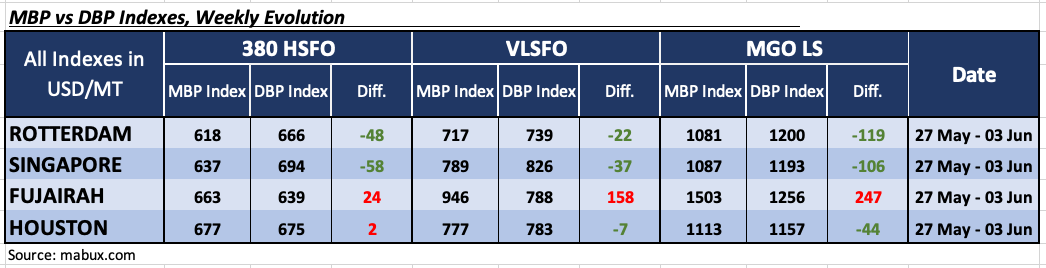

At the end of Week 23, the MABUX Market Differential Index (MDI) — the ratio between Market Bunker Prices (MBP) and the MABUX Digital Bunker Benchmark (DBP) — continued to display mixed dynamics across Rotterdam, Singapore, Fujairah and Houston.

380 HSFO segment:

Fujairah and Houston moved into the overvalued zone, with premium levels increasing by 34 and 61 points respectively. Rotterdam and Singapore remained undervalued, although their discount levels narrowed by two and 30 points. Houston’s MDI approached full parity between MBP and DBP, indicating near-perfect correlation between market prices and the digital benchmark.

VLSFO segment:

Houston returned to the undervalued zone, joining Rotterdam and Singapore. The degree of undervaluation decreased by 45 points in Rotterdam and 41 points in Singapore, while increasing by eight points in Houston. Fujairah remained the only overvalued port in this segment, with its premium widening by a further 103 points. Houston’s MDI also moved closer to the 100% correlation threshold between MBP and DBP.

MGO LS segment:

Rotterdam, Singapore and Houston continued to be assessed as undervalued. Discount levels widened by 132 points in Rotterdam and 13 points in Houston, while Singapore recorded a marginal increase of one point. Fujairah remained the sole overvalued port in the segment, with its premium expanding by an additional 79 points. MDI values in Rotterdam, Singapore and Fujairah continued to remain consistently above the US$100.00 level.

Overall, the balance between overvalued and undervalued ports evolved unevenly during the week. Two ports shifted into the overvalued zone in the 380 HSFO segment, while one port moved into the undervalued zone in the VLSFO segment.

These developments reflect the continuation of mixed trends in the relationship between market bunker prices and the MABUX digital benchmark amid persistently elevated market volatility, Ivanov commented.

Looking ahead, Ivanov expects global bunker indices to continue exhibiting mixed dynamics next week, as temporary market stabilisation is offset by persistent uncertainty surrounding prospects for a settlement of the Middle East conflict. Elevated market volatility is likely to remain the key driver of divergent price movements across bunker fuel segments.