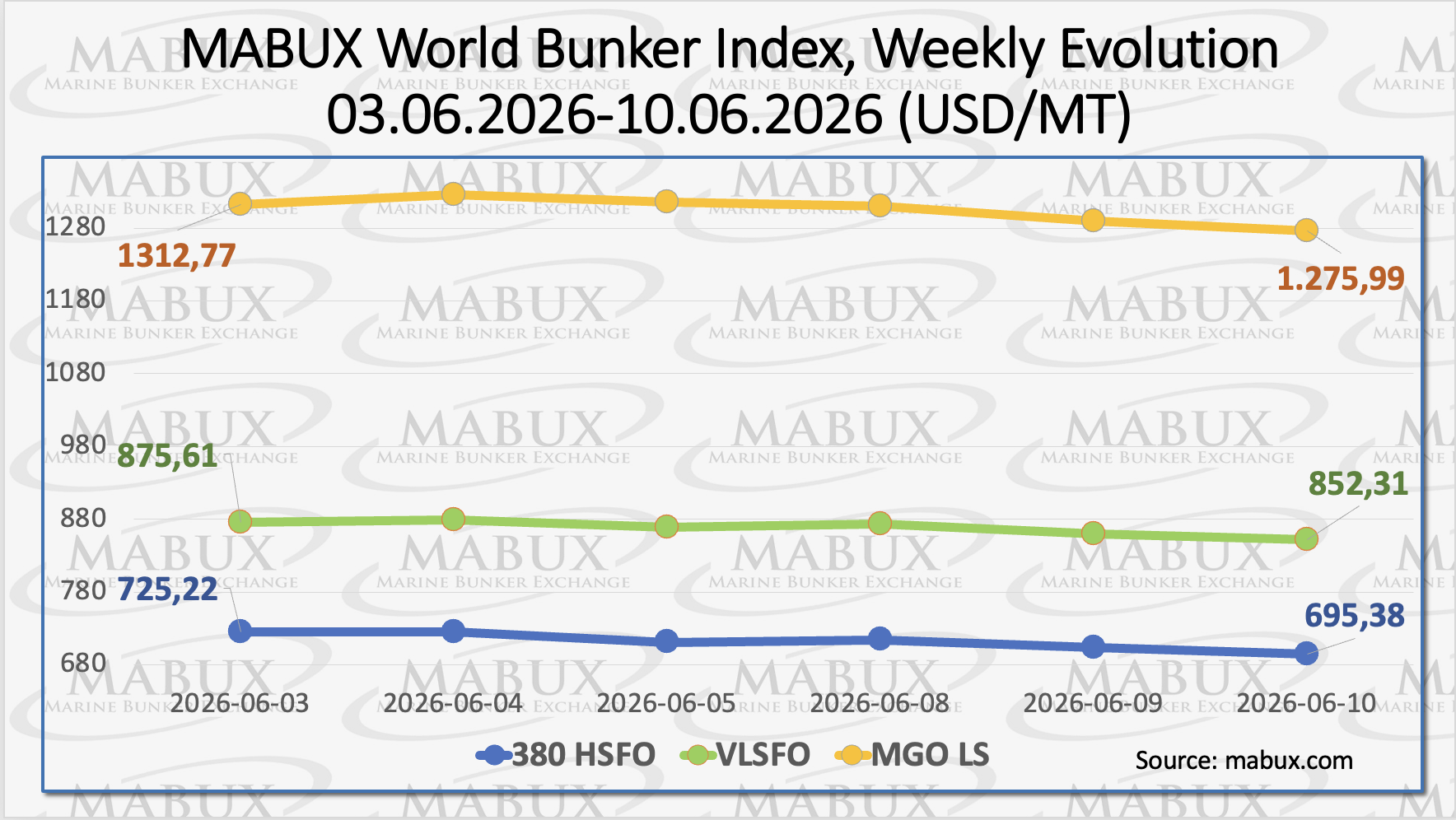

The global bunker market maintained a downward trajectory during Week 24 as a temporary stabilization of the geopolitical situation in the Middle East eased concerns over potential supply disruptions, Sergey Ivanov, Director at MABUX, noted.

The 380 HSFO index declined by US$29.84, falling from US$725.22/MT last week to US$695.38/MT and dropping below the psychological US$700 threshold. The VLSFO index also moved lower, decreasing by US$23.30 from US$875.61/MT to US$852.31/MT.

The MGO LS index recorded the largest loss among the main bunker grades, falling by US$36.78 from US$1,312.77/MT last week to US$1,275.99/MT. At the time of writing, bearish sentiment continued to dominate the market, with bunker prices extending their decline at a moderate pace, Ivanov explained.

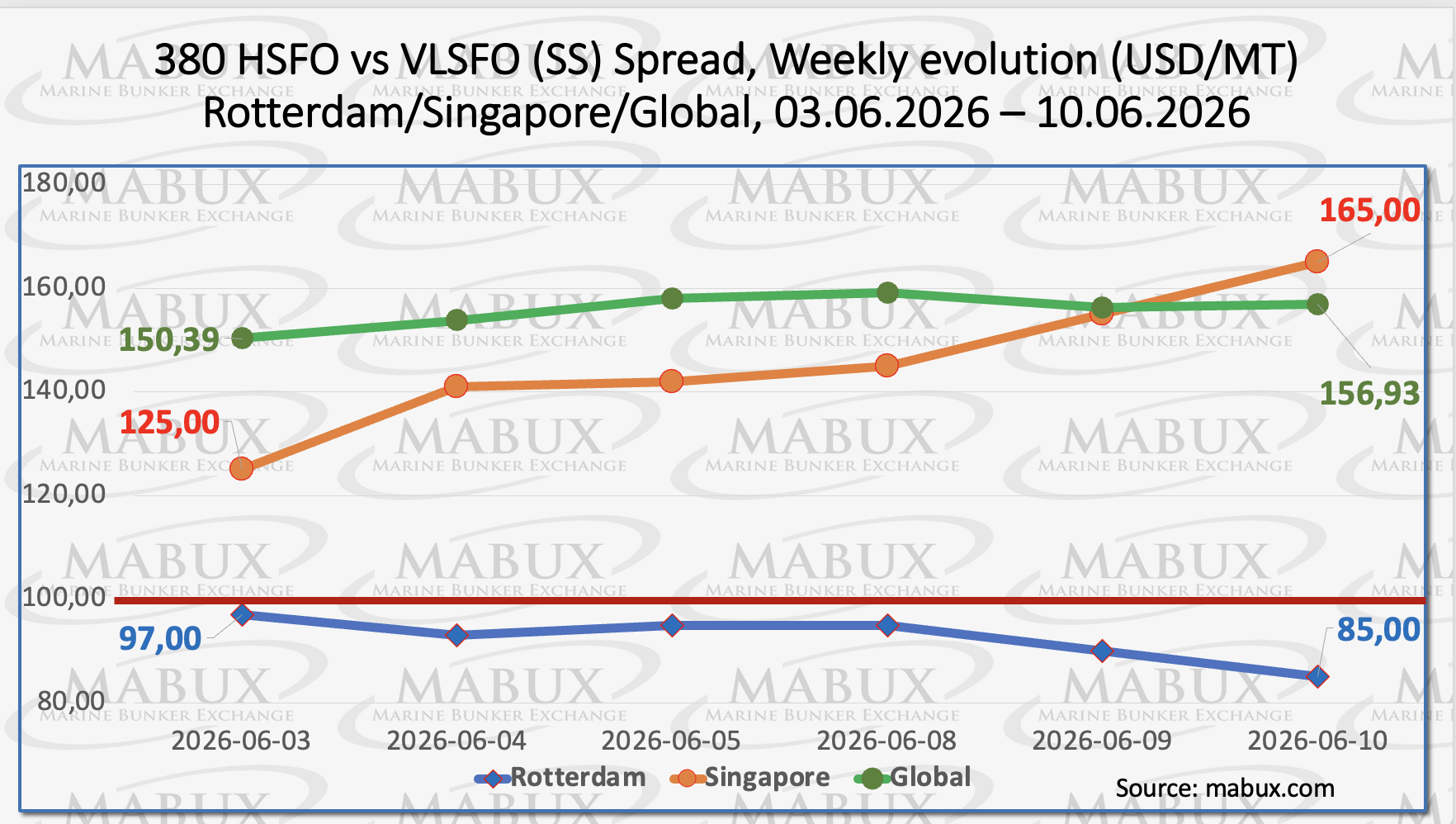

The MABUX Global Scrubber Spread (SS) — the price differential between 380 HSFO and VLSFO — continued its moderate upward movement, increasing by US$6.54 from US$150.39 last week to US$156.93. The index surpassed the US$150.00 level and remained comfortably above the psychological US$100.00 threshold, which is generally regarded as the SS breakeven point.

The weekly average of the Global SS Spread also strengthened, rising by US$11.66.

In Rotterdam, however, the SS Spread moved in the opposite direction, declining by US$12.00 from US$97.00 last week to US$85.00. The index remained below the US$100.00 mark, while its weekly average decreased by US$5.83.

In Singapore, the 380 HSFO/VLSFO spread widened significantly by US$40.00, increasing from US$125.00 last week to US$165.00 and exceeding the US$150.00 level. At the same time, the port’s weekly average SS Spread edged lower by US$7.17.

Overall, the SS Spread continues to lack a clear directional trend, with regional indices moving in opposite directions. Nevertheless, spread values above US$100.00 continue to indicate stronger economic incentives for scrubber-equipped vessels consuming 380 HSFO compared to ships operating on conventional VLSFO.

Looking ahead, Ivanov expects SS Spread dynamics to remain volatile and mixed next week as market participants continue to assess geopolitical developments and the prospects for a sustainable settlement in the Middle East.

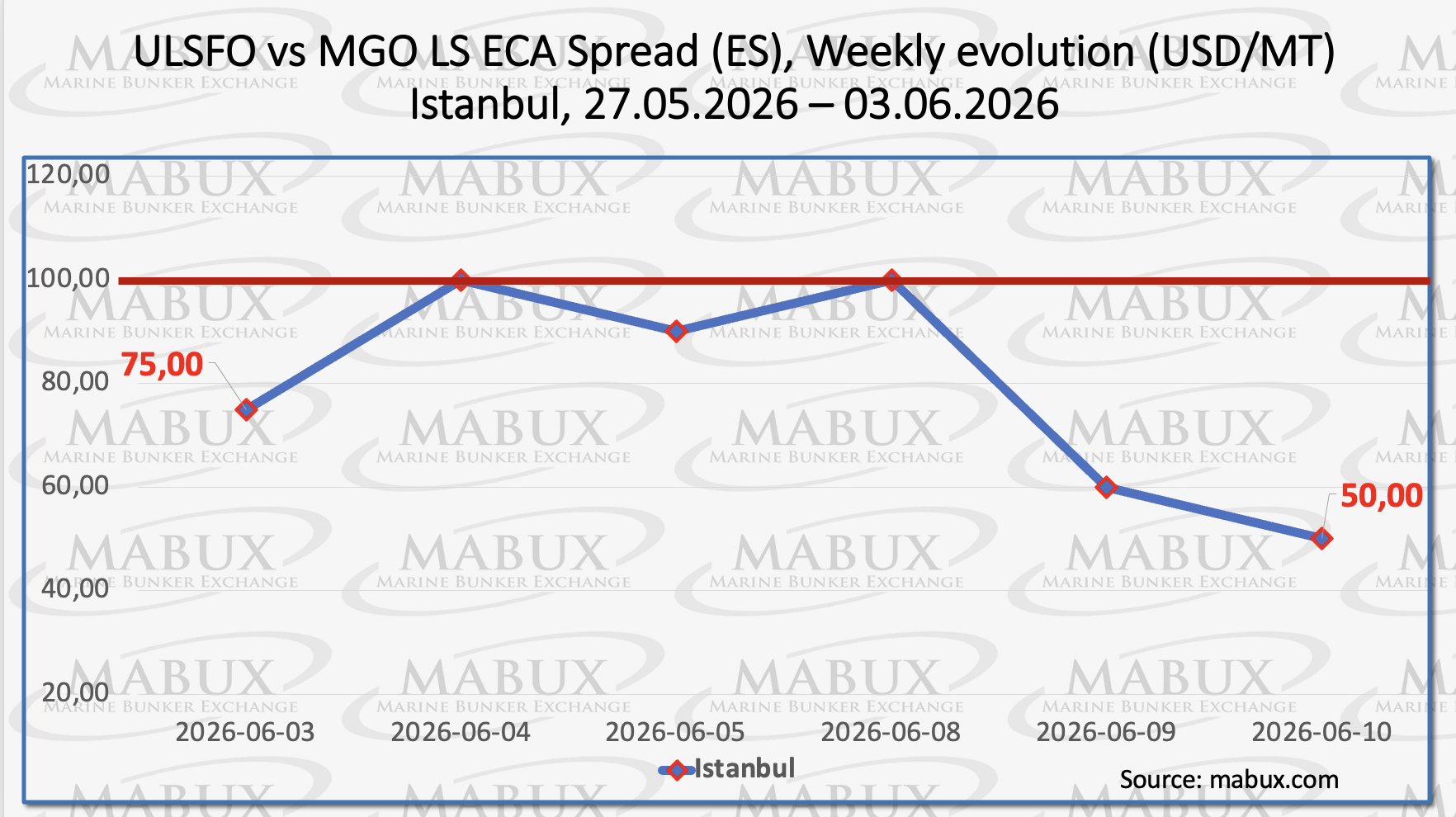

At the end of the week, the ECA Spread (ES) — the price differential between ULSFO and MGO LS — in Istanbul narrowed by US$25.00, declining from US$75.00 last week to US$50.00.

During the reporting period, however, the index briefly reached the US$100.00 level, while its weekly average increased by US$29.17. The Venice ECA Spread was not calculated due to the absence of regular market quotations.

Overall, the ECA Spread continues to demonstrate mixed dynamics, with no clear directional trend emerging. Index values have yet to establish themselves above the psychological US$100.00 threshold, indicating a still-limited premium of MGO LS over ULSFO in ECA-compliant operations.

Given the elevated volatility across the global bunker market, Ivanov expects the ECA Spread to remain subject to multidirectional fluctuations next week, driven by ongoing uncertainty in energy markets and geopolitical developments.

Europe’s regasification capacity jumped 32% between 2022 and 2025 to roughly 270 BCM per year, propelled by rapid FSRU deployments in Germany and expansions in Poland and the Netherlands.

Germany alone commissioned 44.8 BCM of import capacity across Wilhelmshaven, Brunsbüttel, Lubmin and Stade within 24 months. Poland’s Gdańsk FSRU and Świnoujście upgrade now provide 14.4 BCM combined, giving Warsaw surplus volumes for regional exports.

Lithuania’s Klaipėda terminal underscores the rise of small-scale reloads, posting 1,834 truck loadings in 2025. Forecast additions could lift capacity to 405 BCM by 2030, implying significant overbuild if demand trends hold. As a result, asset owners are increasingly seeking long-term offtake partners to mitigate utilisation risk.

European underground gas storage levels continued to increase at a moderate pace. As of June 8, storage facilities were filled to 42.79% of total capacity, up 2.03 percentage points from the previous week.

However, inventories remained 18.67 percentage points below the year-end level of 61.46% and continued to lag behind the seasonal average of 50%, highlighting the slower pace of stock replenishment compared to historical norms.

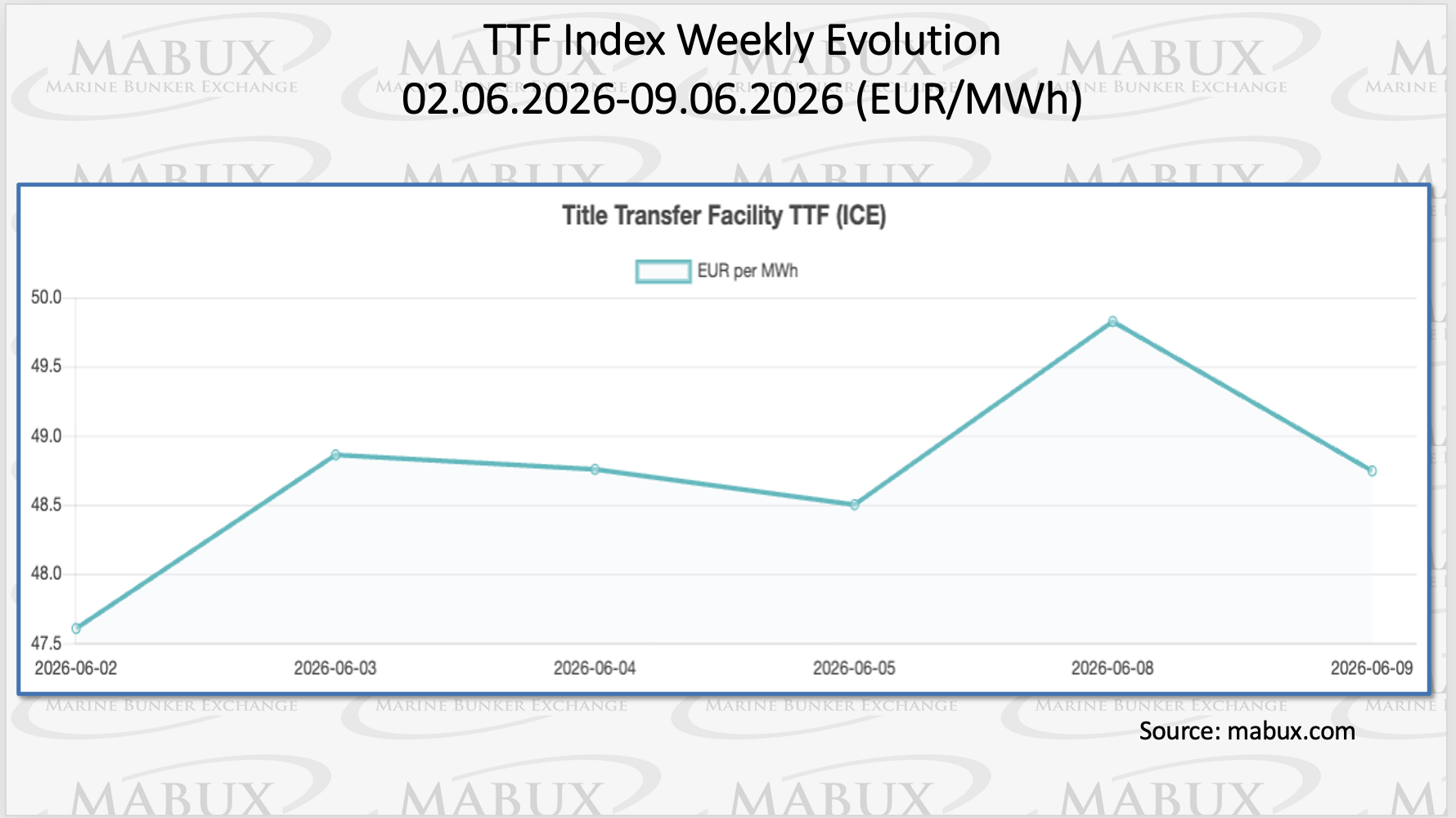

The European TTF gas benchmark maintained its upward trajectory during Week 24. The index increased by €1.137/MWh, rising from €47.607/MWh last week to €48.744/MWh, reflecting ongoing market sensitivity to supply-demand fundamentals and geopolitical developments.

The price of LNG as a bunker fuel at the port of Sines, Portugal, recorded a sharp increase this week, rising by US$90.00/MT to US$1,189/MT compared to US$1,099/MT the previous week.

As a result, the price spread between LNG and conventional marine fuel shifted in favour of conventional fuel for the first time since March 25, 2026. On June 8, MGO LS was assessed at US$1,184/MT in Sines, placing LNG at a US$5/MT premium to MGO LS.

By comparison, LNG had maintained a US$32/MT price advantage over conventional fuel one week earlier. Ivanov noted that the shift highlights changing economics between LNG and conventional marine fuels amid recent price volatility.

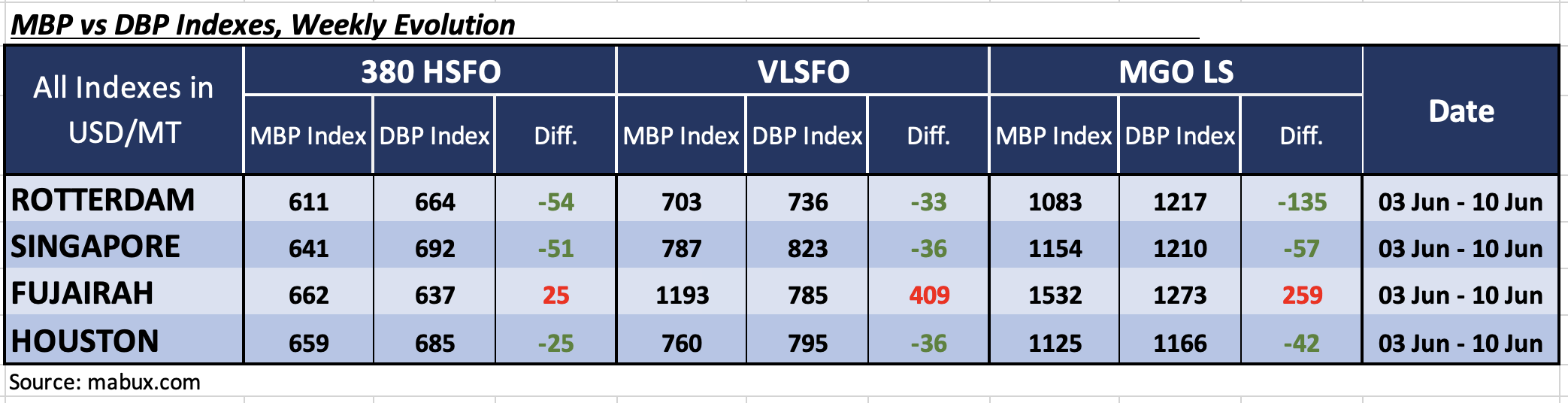

At the end of Week 24, the MABUX Market Differential Index (MDI) — the ratio of Market Bunker Prices (MBP) to the MABUX Digital Bunker Benchmark (DBP) — continued to reflect mixed pricing dynamics across Rotterdam, Singapore, Fujairah and Houston.

380 HSFO segment

Three ports were assessed as undervalued. Houston returned to the undervalued zone, joining Rotterdam and Singapore. Average weekly discount levels increased by six points in Rotterdam and 27 points in Houston, while declining by seven points in Singapore.

Fujairah remained the sole overvalued port, with its overvaluation level rising by one point during the week.

VLSFO segment

Rotterdam, Singapore and Houston also remained undervalued. Average MDI levels increased by 11 points in Rotterdam and 29 points in Houston but edged down by one point in Singapore.

Fujairah continued to be the only overvalued port in this segment, with its overvaluation level surging by 251 points and remaining significantly above the US$100.00 threshold.

MGO LS segment

Rotterdam, Singapore and Houston retained their undervalued status. MDI levels increased by 16 points in Rotterdam but declined by 49 points in Singapore and by two points in Houston.

Fujairah remained the only overvalued port, with its overvaluation level increasing by a further 12 points. The MDI values for both Rotterdam and Fujairah continued to remain consistently above the US$100.00 mark.

Overall, the balance between overvalued and undervalued ports remained largely unchanged during the week, with Houston’s return to the undervalued zone in the 380 HSFO segment representing the only notable shift.

The prevailing trend in the DBP assessment remains mixed; however, undervalued bunker prices continue to dominate across the major global hubs amid persistently elevated market volatility, Ivanov commented.

Persistently high volatility across the global bunker market, combined with ongoing uncertainty surrounding the prospects for a resolution of the conflict in the Middle East, continues to hinder the formation of a stable pricing trend in the bunker sector.

Against this backdrop, Ivanov expects mixed bunker fuel price dynamics to remain the prevailing market pattern next week, with prices likely to continue fluctuating in response to geopolitical developments and changes in energy market sentiment.