![]()

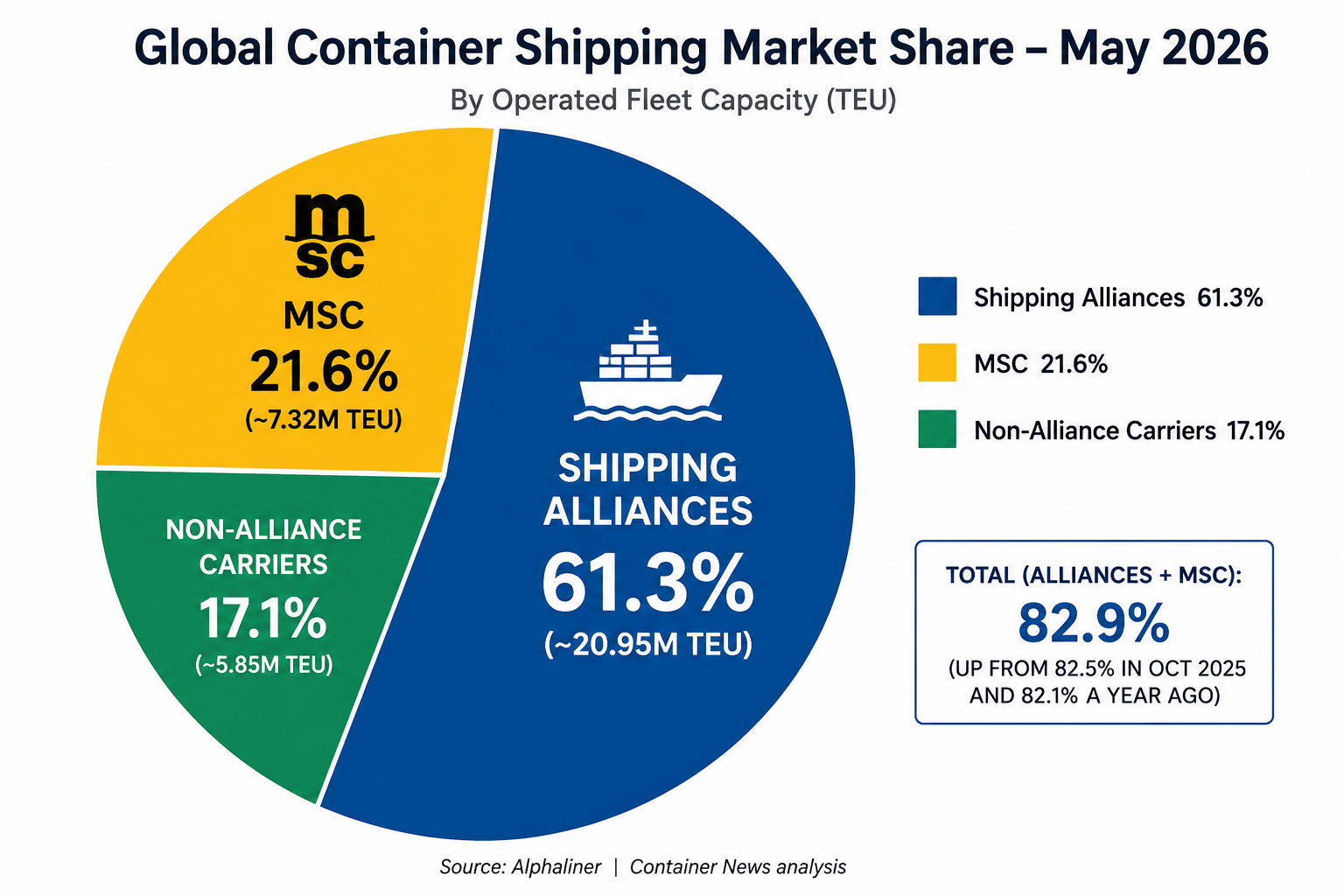

Shipping alliances continue to strengthen their dominance across the global container shipping industry, with the latest fleet data showing that alliance carriers together with MSC now control almost 83% of the market.

According to the latest figures from Alphaliner, shipping alliances and MSC currently account for approximately 82.9% of global container shipping capacity, compared with 82.5% recorded in October 2025 and 82.1% one year ago. The latest increase confirms the continued concentration of market power among the industry’s largest liner operators.

Although alliance members do not deploy their entire fleets within joint services, the scale of cooperation between the major carriers continues to shape competition across the main East-West trade corridors.

MSC strengthens independent leadership

Despite operating outside a formal alliance structure following the end of the 2M partnership, MSC continues to dominate the global container shipping market independently.

The Geneva-based carrier now controls 21.6% of global container shipping capacity, up from 21% recorded in late 2025. MSC’s operated fleet has also surpassed the symbolic milestone of 1,000 ships, reaching approximately 7.32 million TEUs.

The carrier continues to pursue one of the industry’s most aggressive expansion strategies, supported by an orderbook of 126 vessels.

MSC’s scale now allows the company to compete directly against entire shipping alliances across both East-West and North-South trades, reinforcing its unique position within the liner shipping sector.

Gemini Cooperation approaches 21% market share

The Gemini Cooperation partners, Maersk and Hapag-Lloyd, continue to hold one of the strongest positions among global shipping alliances.

Together, the two carriers operate approximately 7.06 million TEUs across 1,027 ships, representing around 20.9% of global container shipping capacity.

Maersk currently controls 4.66 million TEUs across 737 vessels, while Hapag-Lloyd operates nearly 2.4 million TEUs across 290 ships.

The partnership also maintains a combined orderbook of 152 vessels, including 93 ships for Maersk and 59 for Hapag-Lloyd.

As the Gemini network moves closer to full implementation, both carriers continue prioritizing schedule reliability, operational efficiency and simplified network structures.

Ocean Alliance remains the largest shipping alliance

The Ocean Alliance continues to be the largest shipping alliance in terms of deployed fleet capacity.

Based on the latest available fleet figures, CMA CGM, COSCO Group and Evergreen collectively operate approximately 9.9 million TEUs across 1,522 ships, giving the alliance a market share exceeding 29%.

CMA CGM remains the alliance’s largest member, operating 4.31 million TEUs across 723 ships. The French carrier also maintains a massive orderbook of 152 vessels totaling nearly 1.77 million TEUs.

COSCO Group, together with OOCL, controls around 3.6 million TEUs across 559 vessels and maintains an orderbook of 141 ships. Meanwhile, Evergreen operates close to 2 million TEUs across 240 ships and currently has 74 vessels on order.

In total, the Ocean Alliance members maintain a combined orderbook of 367 vessels, highlighting their long-term commitment to fleet expansion and modernization.

Premier Alliance maintains strong regional presence

The Premier Alliance, consisting of ONE, HMM and Yang Ming, continues to maintain a strong position across the trans-Pacific and intra-Asia trades.

HMM currently operates approximately 1.03 million TEUs across 97 ships and maintains an orderbook of 35 vessels. Yang Ming controls around 742,000 TEUs across 98 ships, supported by 16 vessels on order.

ONE operates 2.13 million TEUs across 271 ships, with an additional 54 vessels in its orderbook.

The alliance continues investing in fuel-efficient vessels, fleet renewal and operational flexibility to remain competitive across key regional trades.

Non-alliance carriers continue losing market share

While shipping alliances and MSC continue strengthening their market position, non-alliance carriers now control only around 17.1% of global container shipping capacity.

Several independent operators nevertheless remain important players within regional and niche markets.

ZIM Integrated Shipping Services currently represents approximately 2.1% of global capacity, operating 699,472 TEUs across 116 ships. Taiwan-based Wan Hai Lines controls around 1.8% of the market, while Singapore-headquartered Pacific International Lines (PIL) accounts for approximately 1.3%.

Meanwhile, feeder and regional specialists such as X-Press Feeders and SITC continue to maintain solid positions, each controlling roughly 0.6% of global container shipping capacity.

Despite their smaller scale, these carriers remain critical for intra-regional connectivity and specialized trade coverage.

Potential ZIM developments could strengthen shipping alliances further.

The growing dominance of shipping alliances could intensify even further in the coming years.

Industry observers continue monitoring developments surrounding potential acquisition and cooperation discussions involving ZIM. If such a deal is ultimately finalized, the market share controlled by alliance-linked carriers could increase even more, further reducing the space available for truly independent operators.

At the same time, the liner shipping industry’s massive orderbook activity shows that competition among the world’s largest carriers remains extremely aggressive.

However, the next phase of competition is expected to focus increasingly on operational efficiency, schedule reliability, digital integration and decarbonization strategies, rather than fleet size alone.