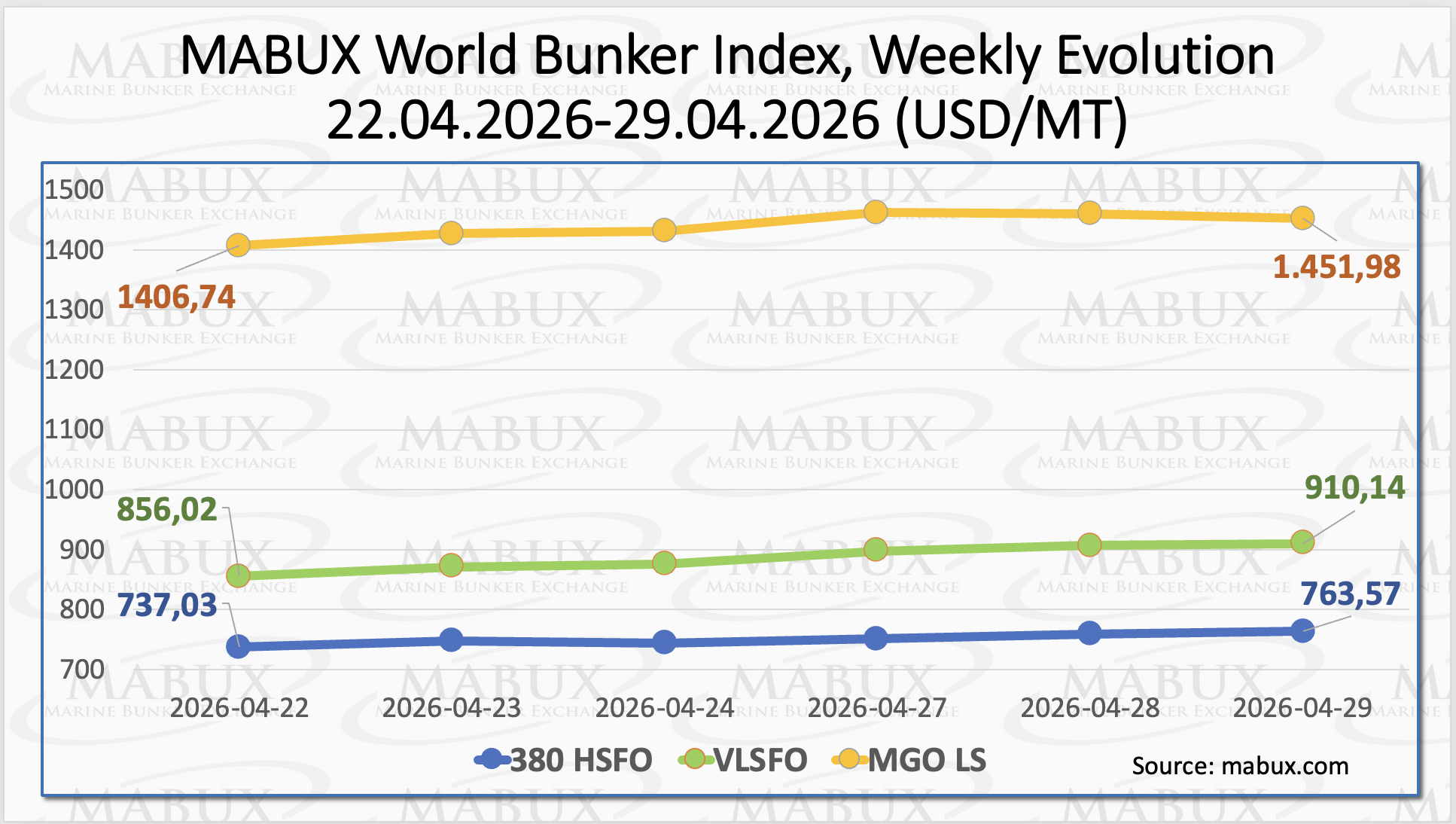

During the week, the global bunker market resumed a clear upward trajectory, driven by persistent geopolitical tensions in the Middle East and the absence of any visible de-escalation signals. Market sentiment remained firmly supported by supply-side concerns and elevated risk premiums.

By the end of the week, the 380 HSFO index increased by US$ 26.54, rising from US$ 737.03/MT to US$ 763.57/MT. The VLSFO index recorded a more pronounced gain of US$ 54.12, climbing from US$ 856.02/MT to US$ 910.14/MT and decisively breaching the US$ 900.00 threshold. The MGO LS index also strengthened, advancing by US$ 45.24 from US$ 1,406.74/MT to US$ 1,451.98/MT. At the time of writing, the market exhibited early signs of relative stabilization, with bunker indices transitioning into a phase of moderate and mixed fluctuations.

“The market has resumed its upward trajectory, supported by persistent supply-side risks and geopolitical uncertainty,” said Sergey Ivanov, Director, MABUX.

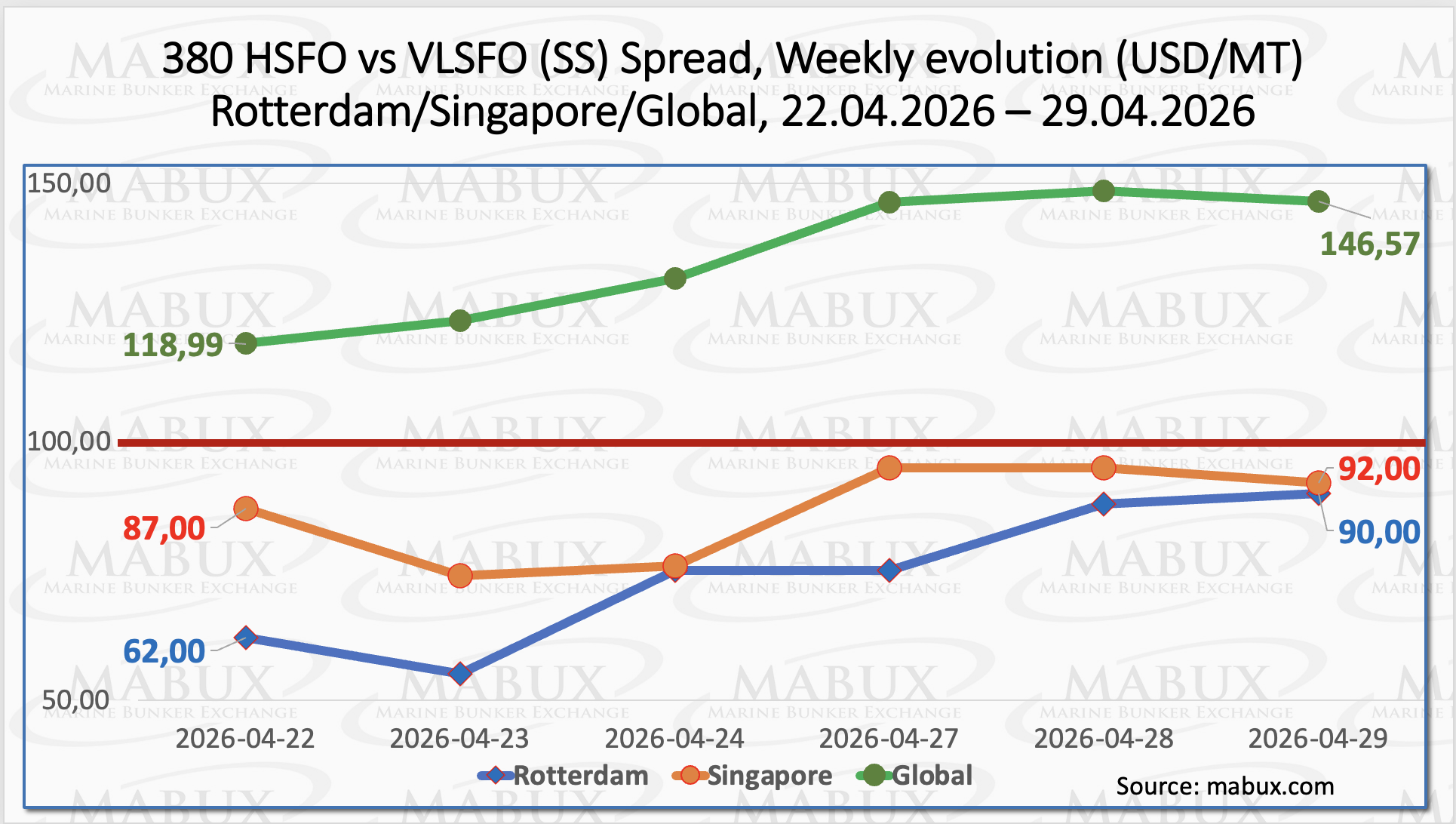

The MABUX Global Scrubber Spread (SS) – representing the price differential between 380 HSFO and VLSFO – posted a significant increase of US$ 27.58, rising from US$ 118.99 last week to US$ 146.57. The index remains firmly above the key psychological threshold of US$ 100.00 (SS breakeven), reinforcing the economic attractiveness of scrubber installations. The weekly average SS index also advanced by US$ 11.43. At the regional level, Rotterdam recorded a substantial gain, with the SS Spread rising by US$ 28.00 from US$ 62.00 to US$ 90.00. In Singapore, the spread expanded by US$ 5.00 from US$ 87.00 to US$ 92.00.

“The widening scrubber spread continues to strengthen the economic case for scrubber-fitted vessels,” Ivanov added.

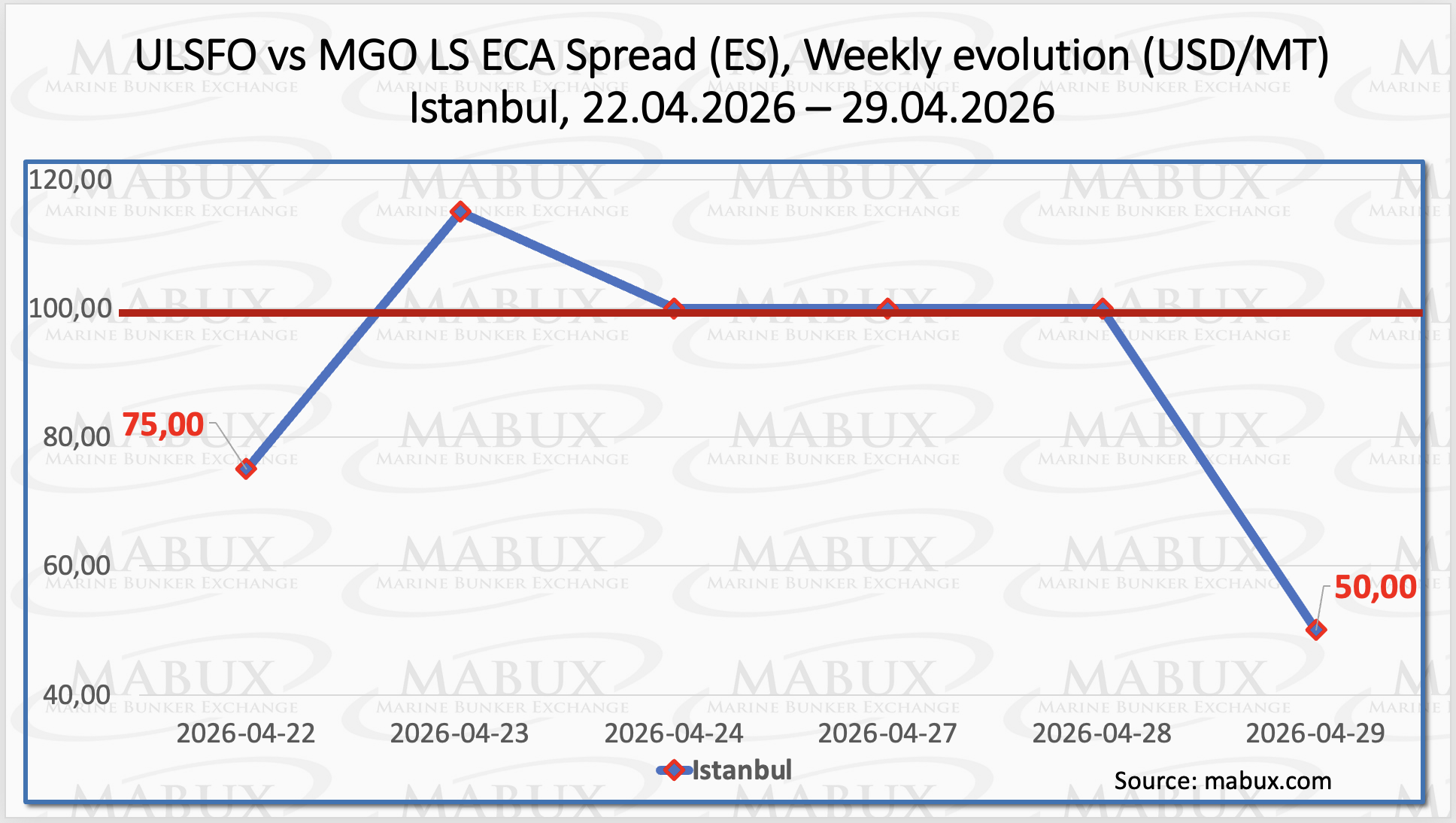

The Istanbul ECA Spread (ES) continued its downward movement over the week, declining by US$ 25.00 from US$ 75.00 to US$ 50.00. Despite the overall decrease, the market remained highly volatile, with intermittent spikes reaching as high as US$ 115.00. The weekly average ES also fell by US$ 14.17.

“ECA spreads remain volatile and highly sensitive to short-term supply disruptions,” Ivanov commented.

According to the Gas Exporting Countries Forum (GECF), the ongoing conflict in the Middle East is significantly disrupting global gas supply dynamics while also triggering demand destruction. LNG imports, particularly in Asia, have declined sharply due to high prices and limited availability. The imbalance between constrained supply and weakening demand is expected to sustain market tightness over the medium term.

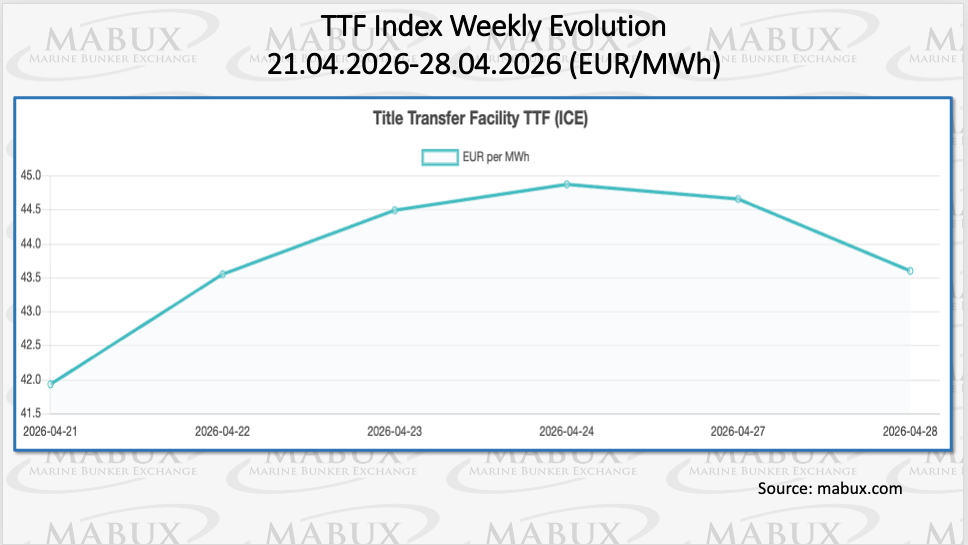

European underground gas storage levels continued to rise modestly as of April 28, reaching 31.97% of total capacity, up by 1.36 percentage points week-on-week. However, storage levels remain significantly below the start of the year. At the same time, the European TTF gas benchmark moved higher, rising by EUR 1.663/MWh to EUR 43.594/MWh.

The price of LNG as bunker fuel at the port of Sines (Portugal) increased by US$ 105.00 this week to US$ 1,090/MT, compared to US$ 985/MT previously. The price differential between LNG and conventional fuel narrowed to US$ 290 in favor of LNG. MGO LS was quoted at US$ 1,380/MT at the port on April 27.

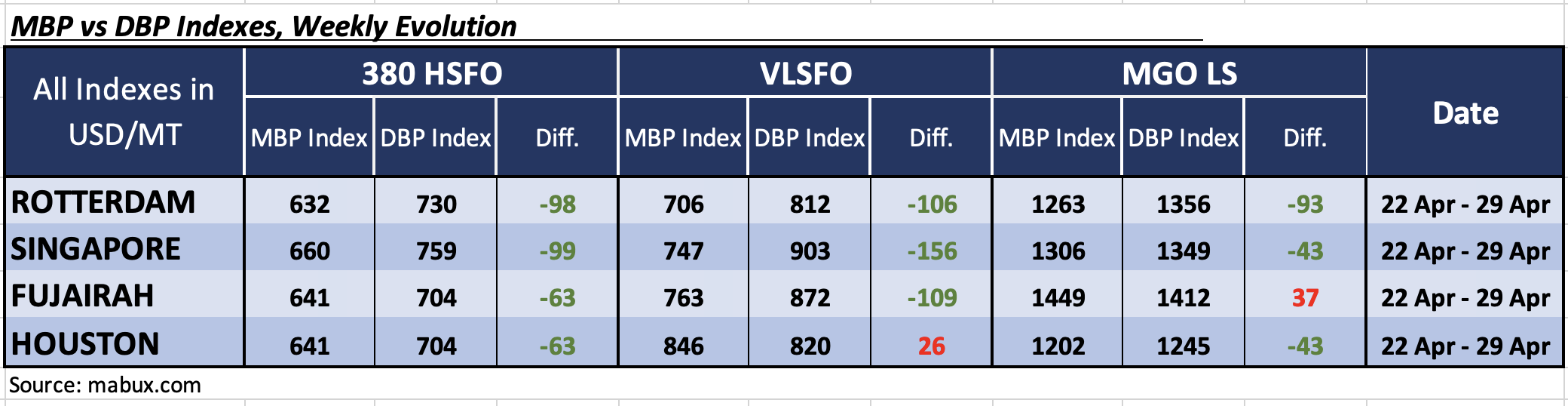

Amid persistent geopolitical tensions and the continued blockade of the Strait of Hormuz, the MABUX Market Differential Index (MDI) showed a clear shift toward deeper undervaluation across Rotterdam, Singapore, Fujairah, and Houston:

• 380 HSFO segment: all ports remained undervalued, with discounts widening across the board.

• VLSFO segment: Houston remained overvalued, while other ports saw further expansion in undervaluation.

• MGO LS segment: Singapore moved into undervaluation, while Fujairah remained the only overvalued port despite a sharp drop in premium.

“The market continues to shift toward undervaluation, reflecting growing divergence between market prices and benchmark levels,” Ivanov said.

Suppliers remain cautious, limiting volumes amid uncertainty around demand recovery and potential inventory risks. This strategy continues to support tight supply conditions and elevated prices.

“We expect bunker indices to maintain upward momentum, with geopolitical developments remaining the key driver of market direction,” Ivanov concluded.