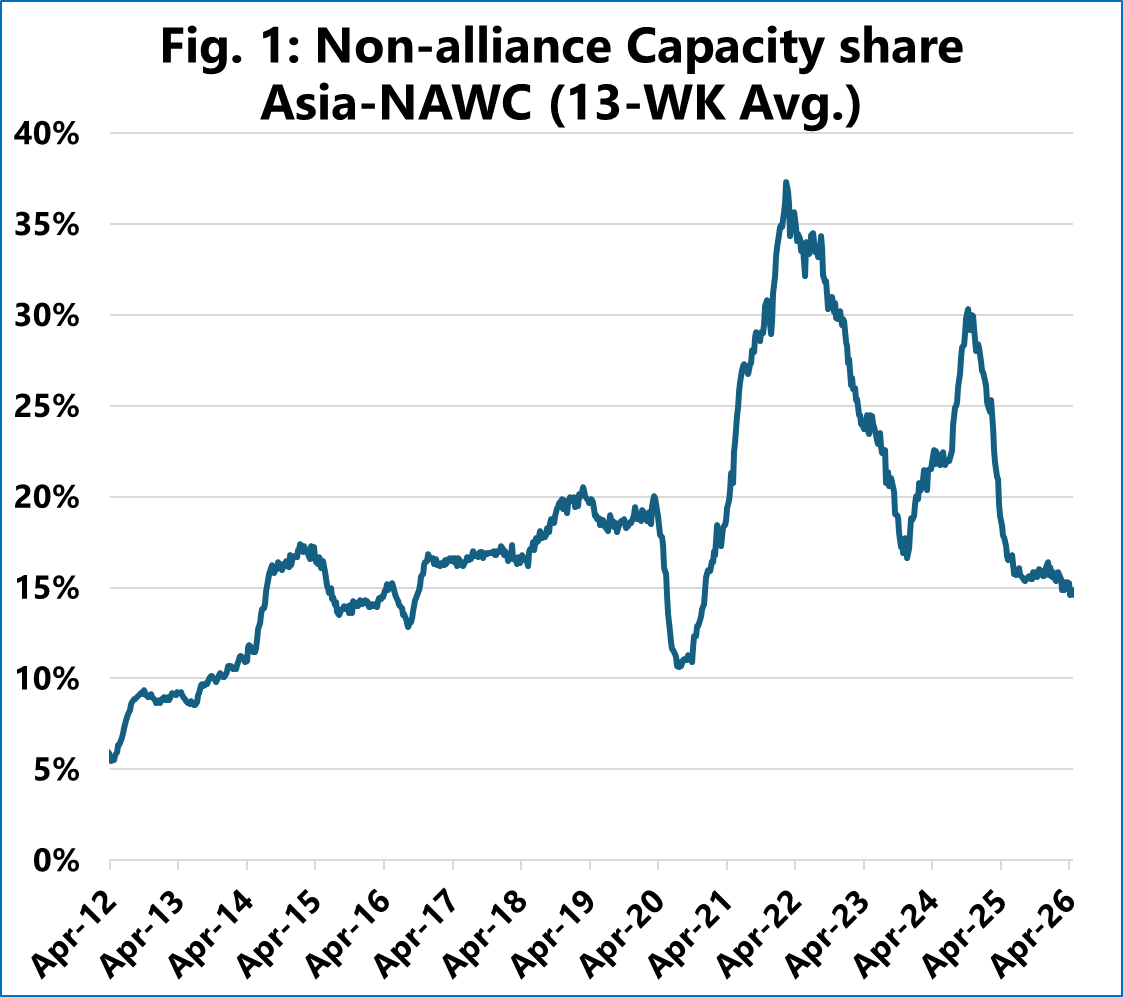

Figure 1 shows the development of Asia-NAWC non-alliance capacity over the past 14 years, calculated as a 13‑week rolling average, to account for short‑term volatility. The historical spikes during periods of market turmoil clearly demonstrate that the barriers to entry for non‑alliance services are relatively low.

However, over the past year, the capacity share of non‑alliance services has steadily declined to a 10‑year low, excluding a brief withdrawal period at the immediate onset of the pandemic.

Furthermore, projections based on current carrier deployment plans point to a continued reduction, with non‑alliance services slated to drop below 15% of the total capacity on offer.

The primary driver of this variability is the prevailing freight rate environment. Historical data shows a clear pattern: high spot rates lead to large injections of new non‑alliance capacity, while low rates prompt rapid withdrawals. Our analysis reveals a strong 79% correlation between spot rate levels and non‑alliance capacity, featuring an 18‑week delay.

Ultimately, this structural elasticity demonstrates that competition remains highly active on the Transpacific trade. Independent carriers are effectively using their agility to scale their presence dynamically, entering and exiting the market in direct response to the economic viability dictated by spot rates.