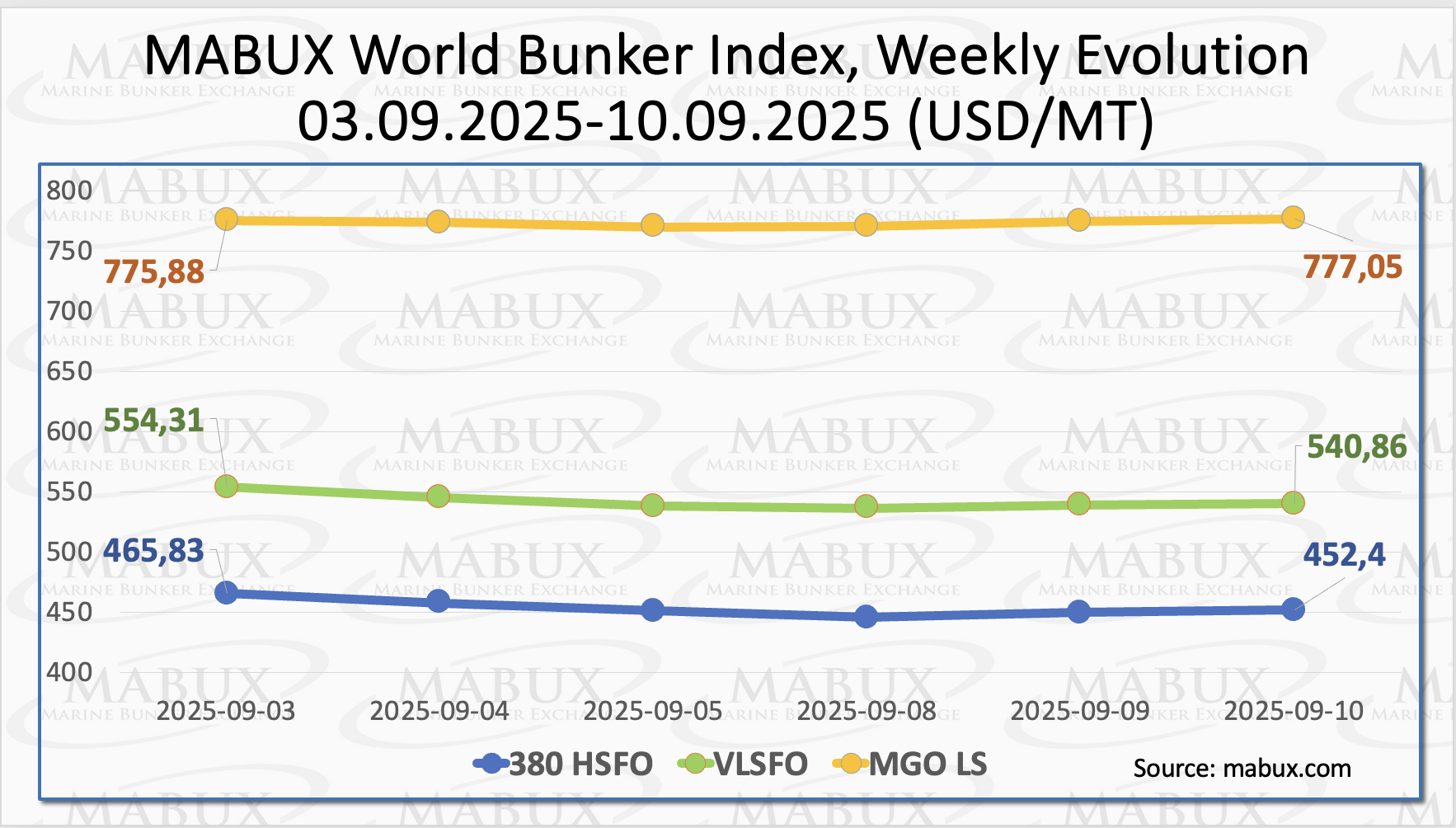

At the close of the 37th week, the global bunker indices MABUX showed mixed dynamics without a clear overall trend. The 380 HSFO index fell by US$13.43, to US$452.40/MT, once again approaching the US$450 mark.

The VLSFO index also declined by US$13.45, to US$540.86/MT, breaking below the US$550 threshold. In contrast, the MGO index recorded a modest gain of US$1.17, rising to US$777.05/MT.

”At the time of writing, the global bunker indices were showing signs of moderate growth”, commented Sergey Ivanov, Director, MABUX.

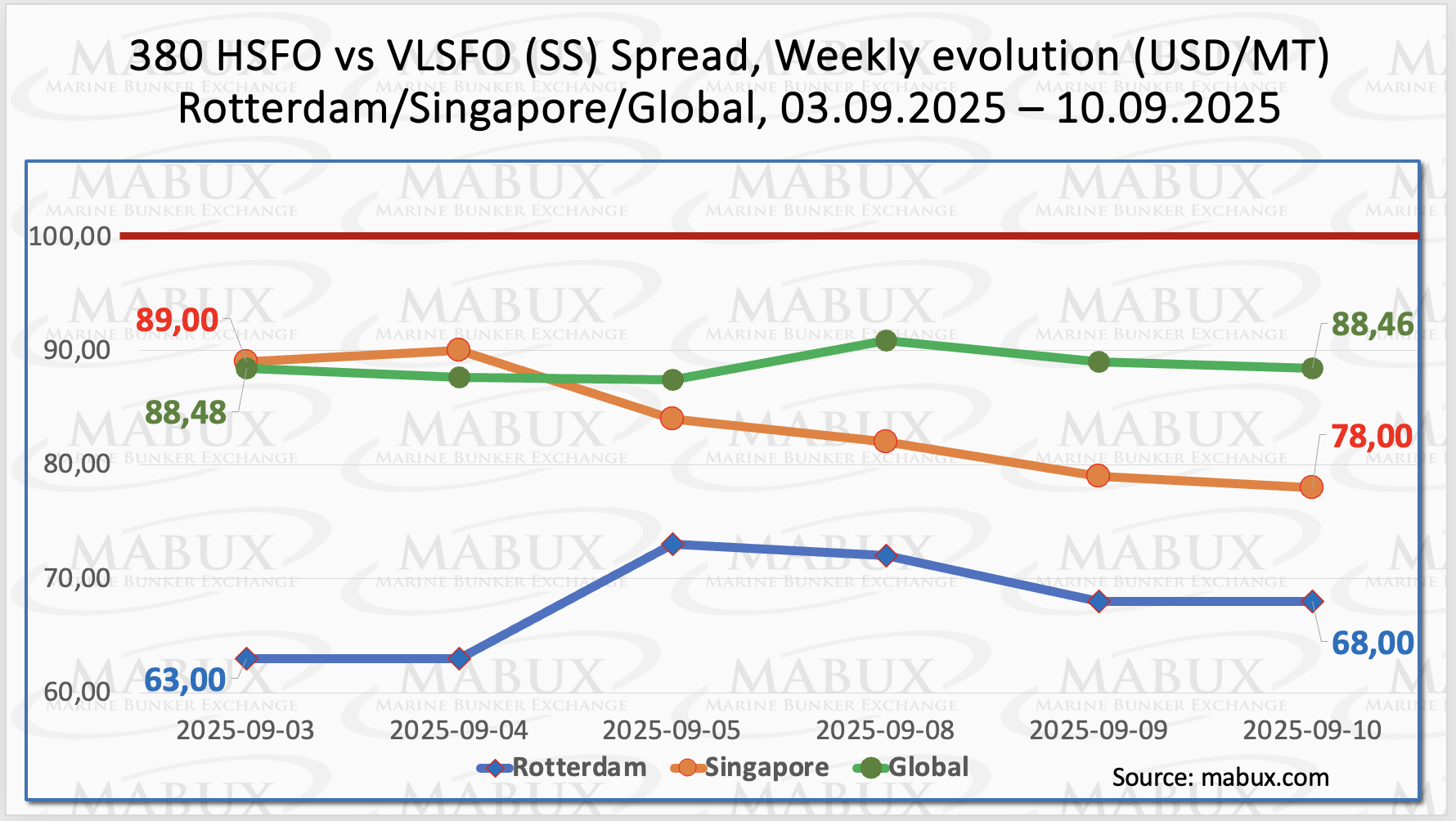

The MABUX Global Scrubber Spread (SS)—the price difference between 380 HSFO and VLSFO—remained practically unchanged over the week, edging down by a symbolic US$0.02 from US$88.48 to US$88.46, and continuing to hold steadily below the psychological breakeven mark of US$100.

The weekly average of the index also showed a slight decline of US$0.37. In Rotterdam, the SS Spread rose by US$5.00, reaching US$68.00, while the weekly average in the port remained unchanged at US$67.83.

In Singapore, by contrast, the 380 HSFO/VLSFO differential narrowed by US$11.00, falling to US$78.00, with the weekly average down by US$6.66. Overall, the SS Spread indices show no clear trend and continue to fluctuate in different directions within the previously established range.

The current pattern is expected to persist next week, with conventional VLSFO fuel likely to maintain its higher profitability compared with the HSFO plus scrubber option.

The United States exported more liquefied natural gas in August than in any previous month. Exports reached 9.33 million tons, surpassing the April record of 9.25 million tons. Europe remains the main destination for US LNG, accounting for 6.16 million tons, or two-thirds of the total — an increase of 0.91 million tons compared with July. Shipments to Asia declined slightly in August, to 1.47 million tons from 1.8 million tons in July.

There is, however, a risk of oversupply in the LNG market, which could drive prices lower. According to Bloomberg, while the market is expected to remain balanced over the next two years, supply is projected to outpace demand from 2027 onward. With new liquefaction terminals coming online, the baseline scenario suggests that by 2030 supply will exceed demand by 63 million tons.

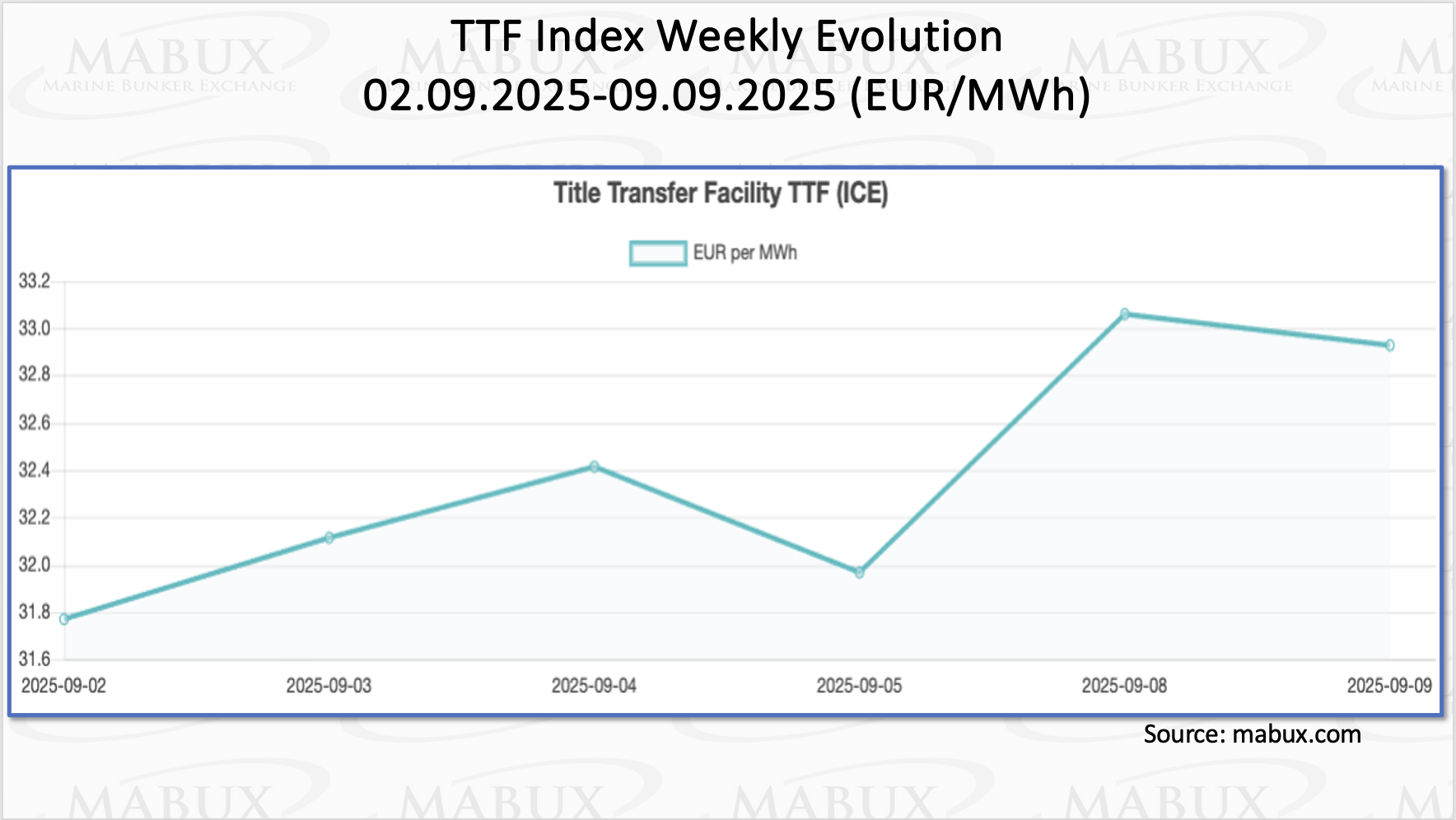

As of September 9, European regional gas storage facilities were 79.63% full, up by 1.55% compared with the previous week. The current level is 8.30% higher than at the start of the year, when storage stood at 71.33%, although the pace of injections has continued to slow moderately. By the end of the 37th week, the European gas benchmark TTF recorded a modest increase of 1.159 euros/MWh, moving from 31.772 euros/MWh the previous week to 32.931 euros/MWh.

Over the past week, LNG bunker fuel prices at the Port of Sines (Portugal) recorded a significant decline of US$51.00, falling to US$711.00/MT. The price differential between LNG and conventional bunker fuel also shifted in favor of LNG. As of the latest assessment, LNG was priced US$51 below conventional fuel, compared with the prior week when conventional fuel held a US$32 advantage. On the reporting date, MGO LS was quoted at US$755.00/MT at the Port of Sines.

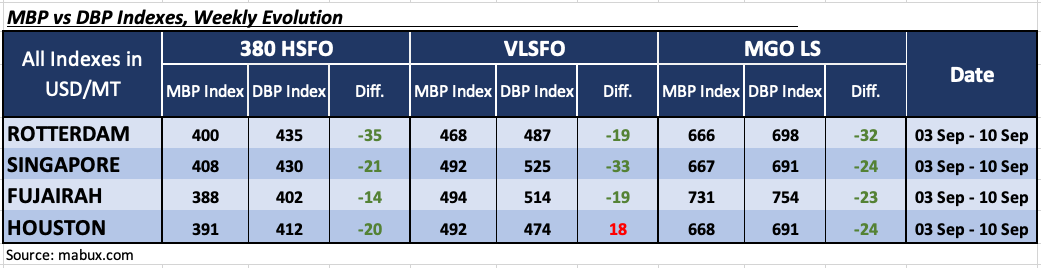

At the end of the 37th week, the updated MABUX Benchmark Market Differential Index (MDI)—the ratio of market bunker prices (MBP) to the MABUX digital bunker benchmark (DBP)—showed the following trends across the world’s major hubs: Rotterdam, Singapore, Fujairah and Houston:

• 380 HSFO segment: All ports remained in the undervalued zone. The average weekly MDI increased by 2 points in Rotterdam but fell by 15 points in Singapore, 55 points in Fujairah, and 22 points in Houston. Overall, MDI values in this fuel segment remain close to the 100% correlation level between MBP and DBP.

• VLSFO segment: Houston moved into the overvalued zone, becoming the only port in this category, with its MDI rising by 62 points. The other ports stayed undervalued, with weekly MDI undervaluation levels edging up by 1 point in Rotterdam and 2 points in Singapore, while Fujairah registered a 17-point decline.

• MGO LS segment: All ports remained undervalued. The MDI rose by 6 points in Rotterdam but fell sharply in the other hubs, decreasing by 34 points in Singapore, 125 points in Fujairah, and 32 points in Houston. Across all ports, MDI values remain well below the $100 mark.

In terms of overall structure, the indices reflected a gradual move toward 100% correlation between MBP and DBP, with the VLSFO segment showing the appearance of one overvalued port (Houston). Nevertheless, the undervaluation trend continues to dominate across all bunker fuel segments. Looking ahead, MDI indices are expected to continue moving toward restoring balance between MBP and DBP.

”We expect the global bunker market will retain the potential for moderate growth next week, with prevailing trends pointing toward a gradual alignment of market and benchmark values”, added Ivanov.