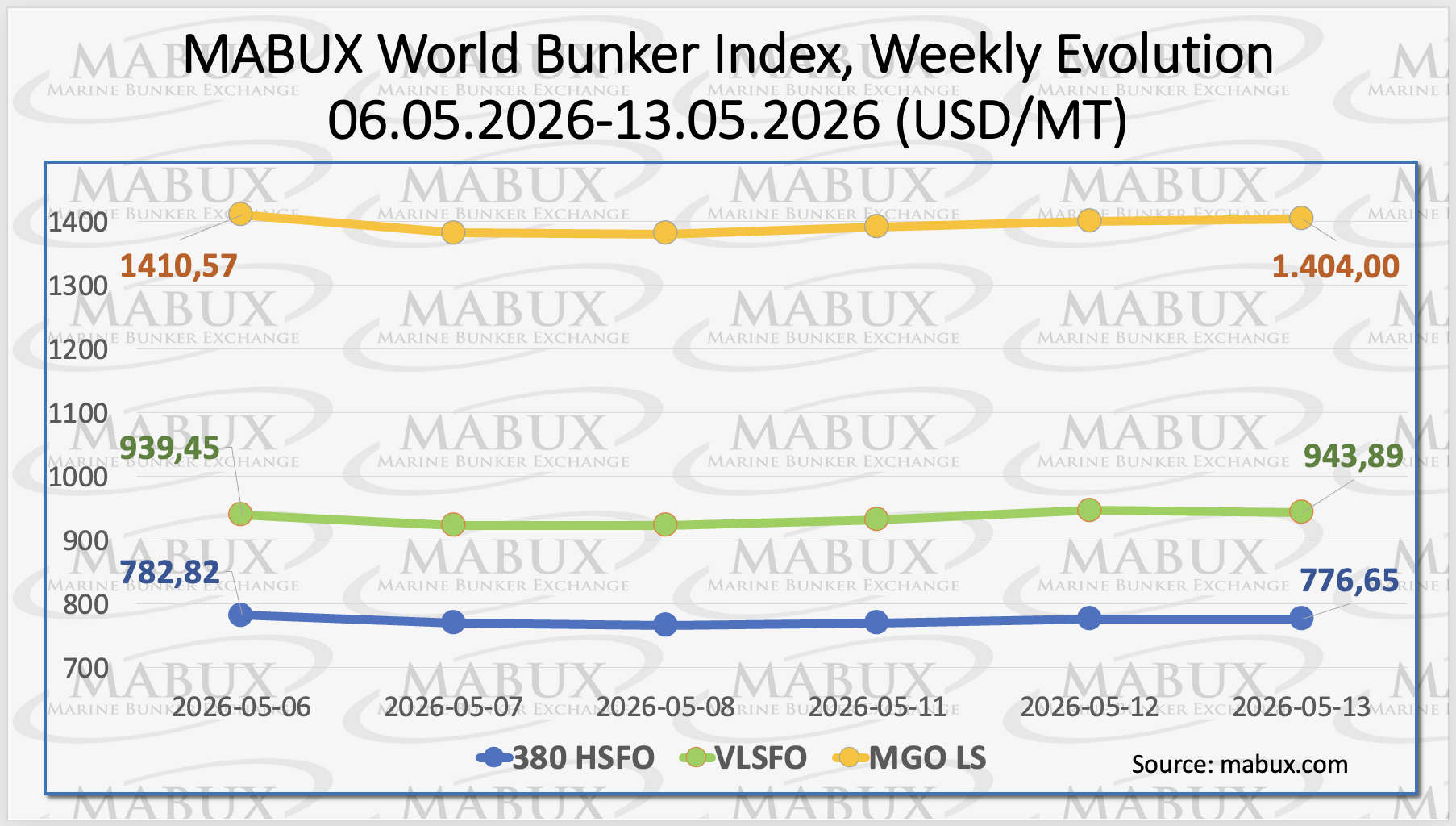

The global bunker market entered a phase of relative stabilisation during Week 20, although mixed price fluctuations continued to persist. At the same time, the volatility amplitude narrowed considerably compared to previous periods.

By the end of the week, the 380 HSFO index declined by US$ 6.17, falling from US$ 782.82/MT last week to US$ 776.65/MT. In contrast, the VLSFO index recorded a moderate increase of US$ 4.44, rising from US$ 939.45/MT to US$ 943.89/MT. Meanwhile, the MGO LS index decreased by US$ 6.57, from US$ 1,410.57/MT last week to US$ 1,404.00/MT. At the time of writing, mixed movements remained the dominant trend across the global bunker market.

According to Sergey Ivanov, the market continues to remain highly sensitive to geopolitical developments and supply concerns.

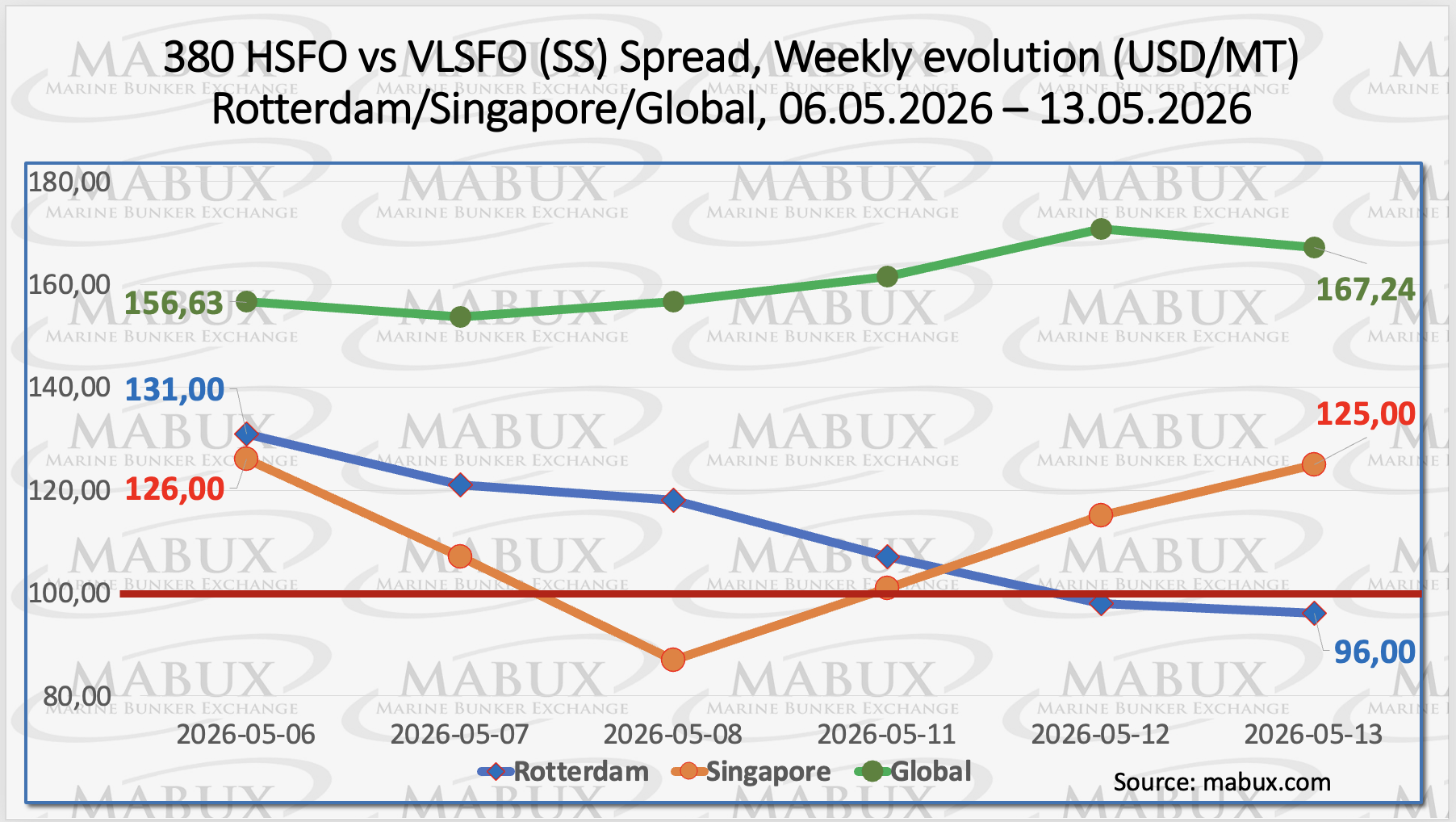

The MABUX Global Scrubber Spread (SS) — the price differential between 380 HSFO and VLSFO — recorded a moderate increase of US$ 10.61, rising from US$ 156.63 last week to US$ 167.24, and remaining comfortably above the psychological threshold of US$ 100.00 (SS Breakeven). The weekly average of the index also advanced by US$ 4.69.

In Rotterdam, the SS Spread contracted sharply by US$ 35.00, declining from US$ 131.00 last week to US$ 96.00 and falling below the US$ 100.00 breakeven level. At the same time, the port’s weekly average SS Spread increased by US$ 6.16. In Singapore, the 380 HSFO/VLSFO spread narrowed marginally by US$ 1.00, from US$ 126.00 last week to US$ 125.00. During the week, the spread temporarily dropped to US$ 87.00, while the weekly average in the port increased by US$ 4.34.

Overall, the SS Spread lacked a clear directional trend throughout the week. Nevertheless, values remaining predominantly above the US$ 100.00 threshold continued to support the strong economic attractiveness of scrubber usage in combination with 380 HSFO versus conventional VLSFO consumption. Despite ongoing relative stability, bunker fuel price volatility remains elevated, which may create conditions for a renewed upward trend in the SS Spread next week.

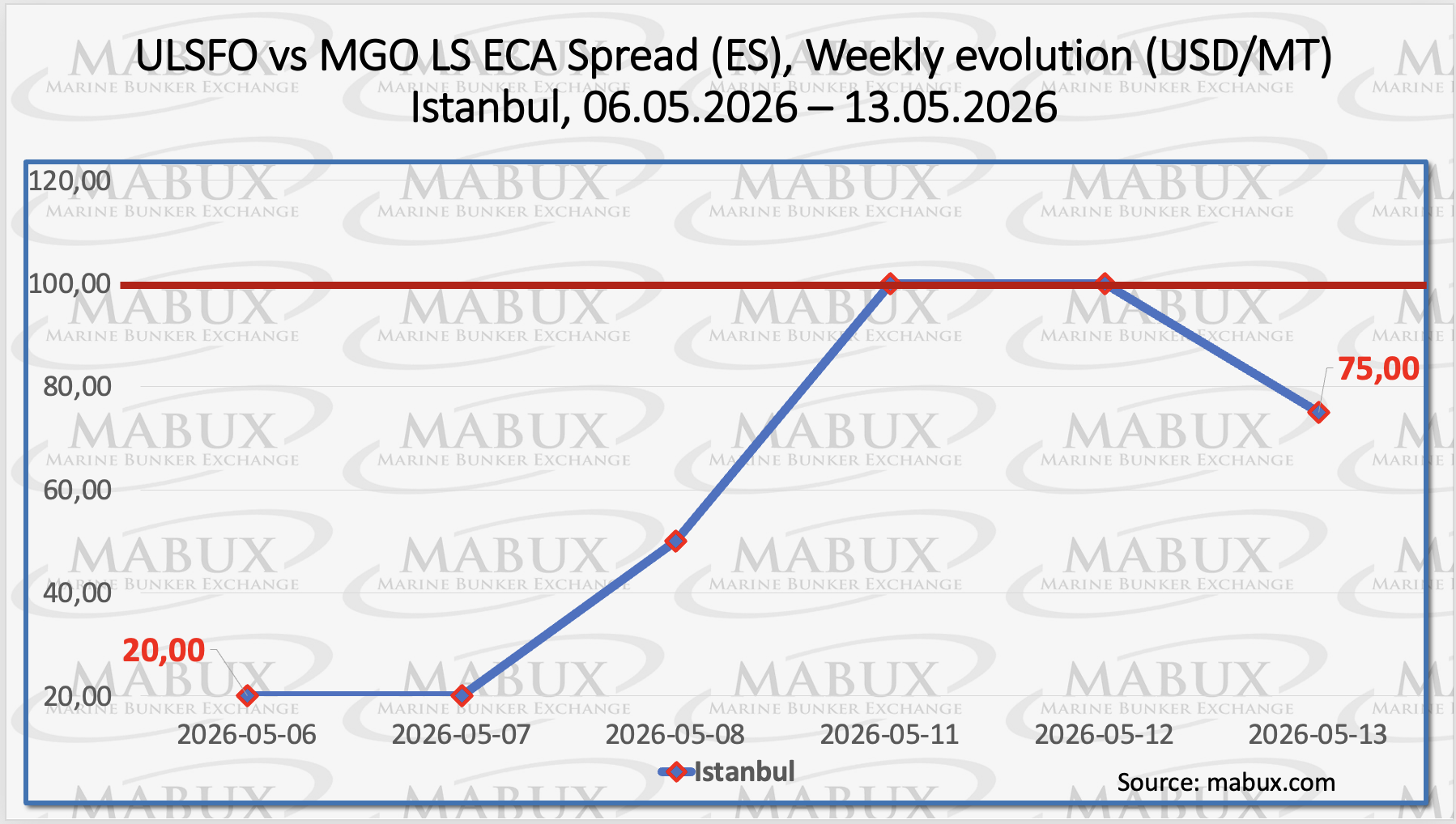

The Istanbul ECA Spread (ES) ended the week with a sharp increase of US$ 55.00, rising from US$ 20.00 last week to US$ 75.00, while the weekly average advanced by US$ 15.00. The Venice ECA Spread remains uncalculated due to the absence of regular market quotations.

Overall, the ECA Spread has fully recovered the losses recorded over the previous weeks and is now approaching the US$ 100.00 threshold, gradually improving the economic attractiveness of conventional ULSFO compared to traditional MGO LS fuel. According to Sergey Ivanov, the ECA Spread is expected to remain close to the US$ 100.00 level next week.

According to the International Energy Agency (IEA), the conflict involving Iran and the resulting disruptions to LNG exports from the Middle East are reshaping the medium-term outlook for the global gas market, with tighter supply conditions expected to persist longer than previously anticipated. LNG availability has already declined by an estimated 15% due to the conflict and the closure of the Strait of Hormuz, one of the world’s key energy transit routes.

At the same time, the EU faces additional pressure to replenish depleted gas inventories, which fell to multi-year lows by the end of the heating season. Europe is expected to require an additional 10 bcm of natural gas this summer to support storage refilling efforts. The IEA estimates that the combination of current supply disruptions and slower LNG capacity growth could result in a cumulative loss of around 120 bcm of global LNG supply between 2026 and 2030, reinforcing expectations of a structurally tighter gas market over the medium term.

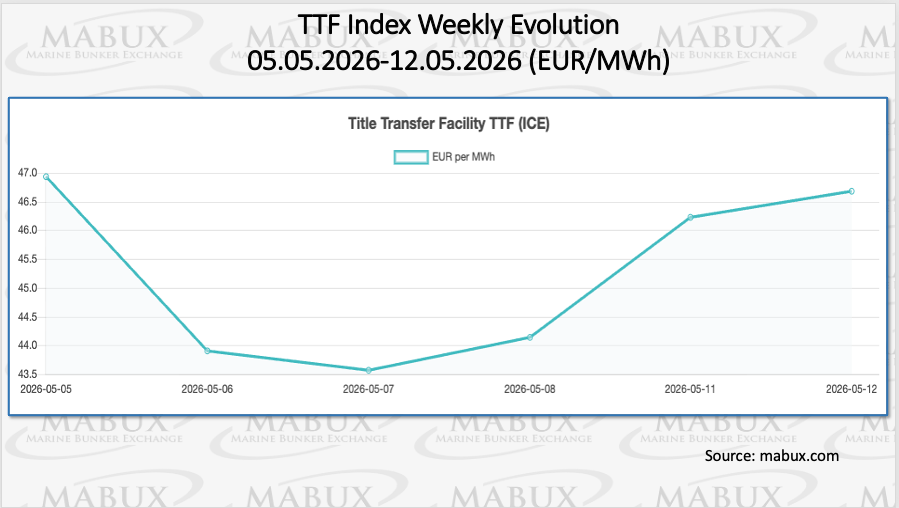

European underground gas storage levels continued their moderate recovery trend as of May 12, reaching 35.57% of total capacity, up 1.50 percentage points compared to the previous week. Nevertheless, current storage levels remain 25.89% below those recorded at the beginning of the year, when inventories stood at 61.46%. Meanwhile, the European TTF gas benchmark remained broadly stable, easing marginally by EUR 0.242/MWh, from EUR 46.926/MWh last week to EUR 46.684/MWh.

The price of LNG as a bunker fuel at the port of Sines (Portugal) decreased by US$ 46.00 this week (US$ 1,059/MT compared to US$ 1,105/MT last week). The price differential between LNG and conventional fuel also narrowed to US$ 220 in favor of LNG (compared to US$ 294 the week before): MGO LS was quoted at US$ 1,279/MT at the port of Sines on May 11.

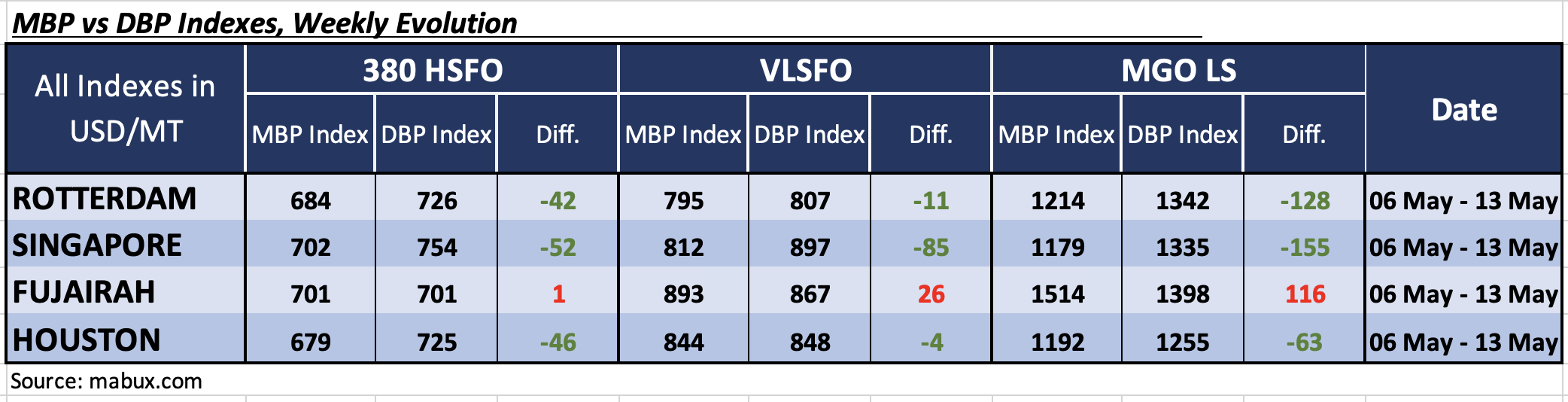

At the end of Week 20, the MABUX Market Differential Index (MDI) — the ratio between market bunker prices (MBP) and the MABUX Digital Bunker Benchmark (DBP) — reflected the following trends across the world’s major bunkering hubs: Rotterdam, Singapore, Fujairah, and Houston:

• 380 HSFO segment: Fujairah moved into the overvalued zone, becoming the only overvalued port in this fuel category, with the overpricing premium increasing by 61 points. The remaining hubs continued to trade in the undervalued zone, although discount levels narrowed by 56 points in Rotterdam, 55 points in Singapore, and 29 points in Houston. Singapore’s MDI fell below the US$ 100.00 mark, while Fujairah’s index approached the 100% MBP/DBP correlation line.

• VLSFO segment: Fujairah also entered the overvalued zone, with the premium rising by 70 points. The other ports remained undervalued. Over the week, the MDI discount narrowed by 110 points in Rotterdam and by 68 points in Singapore, while increasing marginally by 2 points in Houston. Rotterdam’s MDI crossed below the US$ 100.00 threshold, whereas Houston’s index remained close to the 100% MBP/DBP correlation level.

• MGO LS segment: Rotterdam, Singapore, and Houston remained in the undervalued zone. MDI levels declined by 120 points in Rotterdam, while increasing by 23 points in Singapore and by 10 points in Houston. Fujairah continued to be the only overvalued port in this segment, with the overpricing premium rising by 51 points. The MDIs in Rotterdam, Singapore, and Fujairah all exceeded the US$ 100.00 mark.

Overall, the balance between overvalued and undervalued ports shifted once again toward overvaluation during the week, with one port in both the 380 HSFO and VLSFO segments moving into the overvalued zone. Nevertheless, it remains premature to conclude that a sustained overvaluation trend is emerging in the global bunker market.

According to Sergey Ivanov, the global bunker market remains highly volatile amid persistent geopolitical tensions in the Middle East and the continuing disruption of shipping operations in the Strait of Hormuz. Ongoing military and political uncertainty in the region continue to exert strong pressure on global energy and bunker fuel markets, contributing to sharp and irregular price movements.

MABUX expects bunker market indices to maintain mixed fluctuations next week as traders continue to react to geopolitical developments, supply concerns, and elevated freight and insurance costs. However, any further escalation in the military confrontation between the United States and Iran could trigger another sharp upward spike in bunker prices.