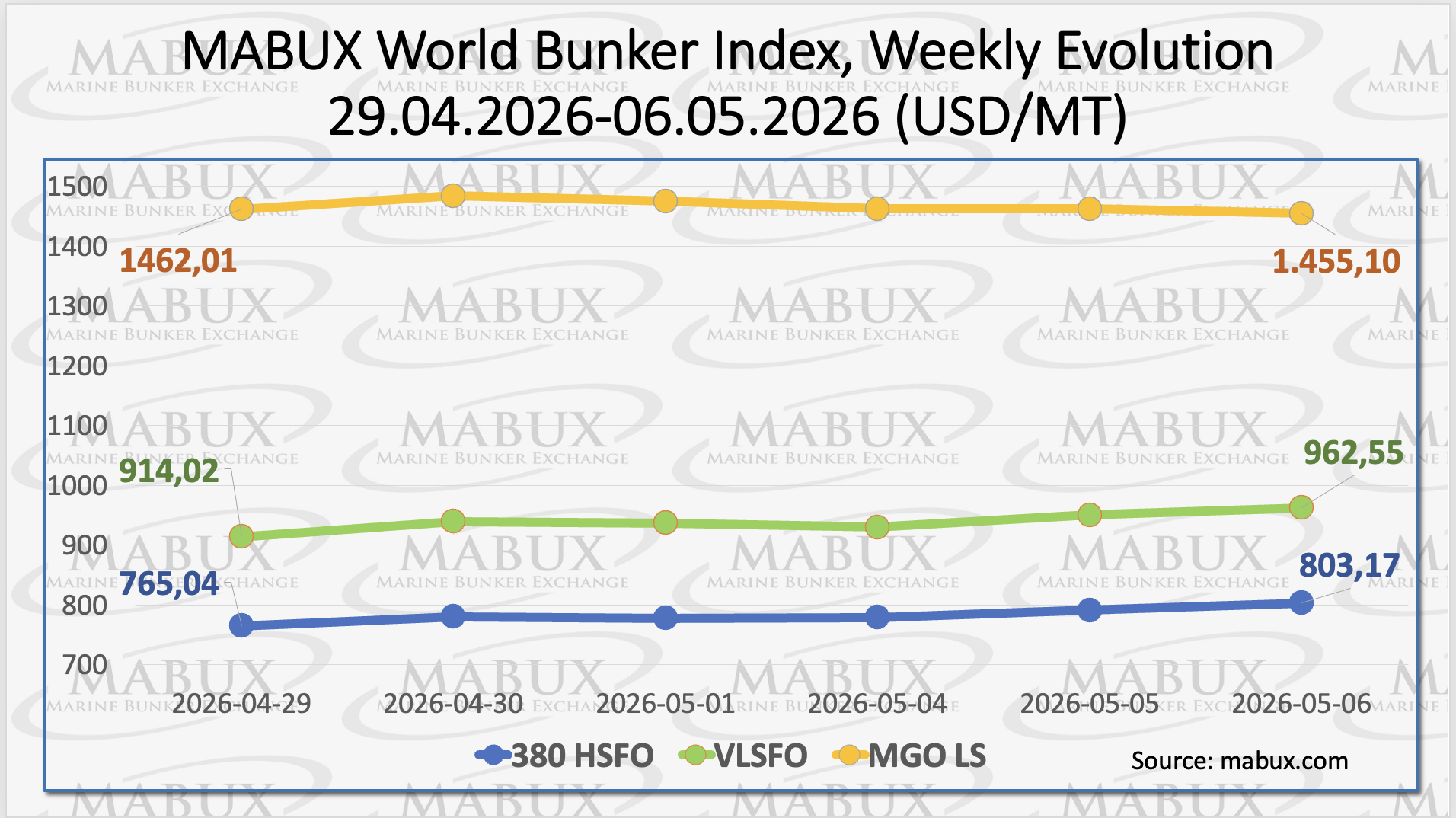

The global bunker market recorded mixed performance over the week, with price fluctuations remaining significant amid ongoing tensions in the Middle East. The 380 HSFO index surged by US$38.13, rising from US$ 765.04/MT the previous week to US$ 803.17/MT and exceeding the US$ 800 threshold.

The VLSFO index also posted a strong gain of US$ 48.53, increasing from US$ 914.02/MT to US$ 962.55/MT, steadily approaching the US$ 1,000 mark. In contrast, the MGO LS index declined by US$ 6.91, falling from US$ 1,462.01/MT last week to US$ 1,455.10/MT. At the time of writing, the global bunker market continued to display a mixed trend, reflecting persistent volatility across fuel segments.

“The market remains highly volatile, with diverging trends across bunker fuel segments,” said Sergey Ivanov, Director, MABUX.

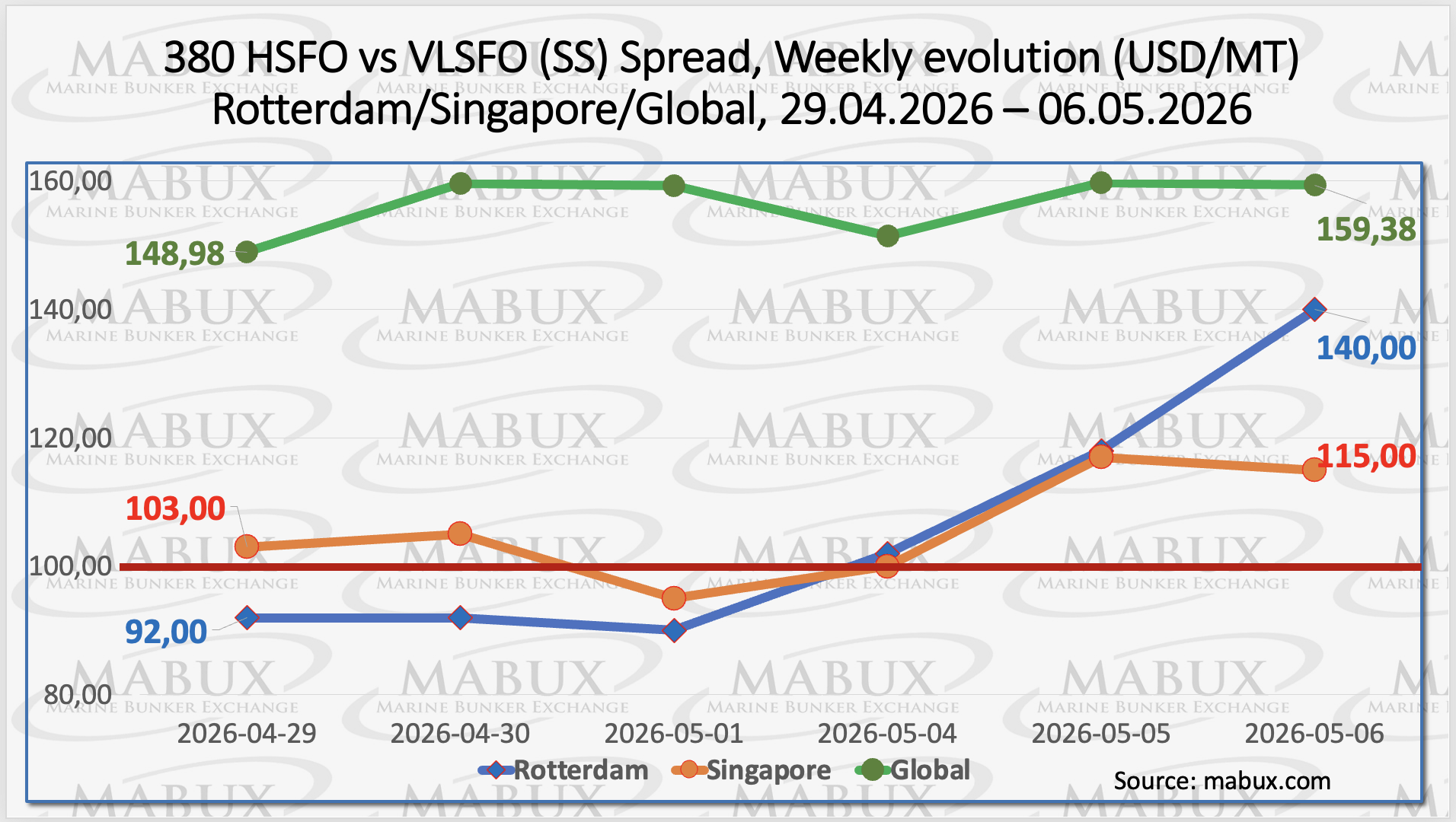

The MABUX Global Scrubber Spread (SS) — the price differential between 380 HSFO and VLSFO — continued its upward trajectory, rising by US$ 10.40 from US$ 148.98 last week to US$ 159.38. The index remained firmly above the psychological US$ 100.00 breakeven threshold and additionally surpassed the US$ 150.00 mark. The weekly average of the global SS Spread also increased by US$ 20.49. In Rotterdam, the SS Spread posted a substantial gain of US$ 48.00, climbing from US$ 92.00 last week to US$ 140.00. The port’s weekly average SS Spread rose by US$ 31.50. In Singapore, the 380 HSFO/VLSFO spread increased by US$ 12.00, from US$ 103.00 last week to US$ 115.00, while the weekly average advanced by US$ 19.33.

“The widening scrubber spread is significantly improving the economics of scrubber-equipped vessels,” Ivanov added.

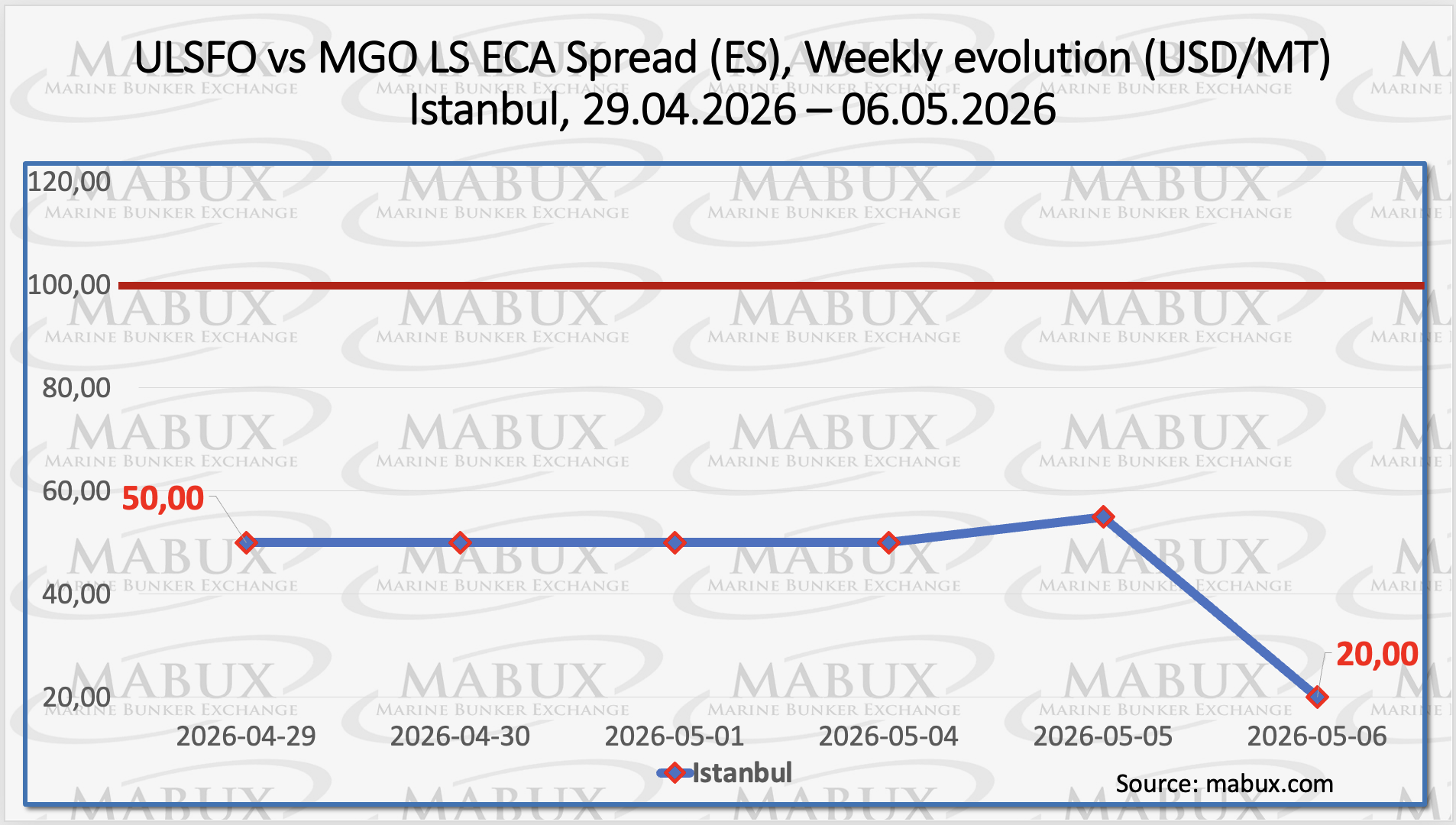

The Istanbul ECA Spread (ES) closed the week at US$ 20.00, down sharply from US$ 50.00 recorded the previous week, while the weekly average declined by US$ 44.17. The Venice ECA Spread remains uncalculated due to the absence of regular market quotations.

“ECA spreads continue to weaken, reducing the competitiveness of conventional ULSFO against MGO LS,” Ivanov commented.

According to Lansdowne Moritz, global LNG bunker volumes declined below 1 million tonnes in Q1 after exceeding this threshold in the previous quarter. The downturn was primarily driven by prolonged cold weather in January, which tightened global gas balances, constrained US LNG exports, and pushed prices higher. Additional pressure came from geopolitical factors, notably the closure of the Strait of Hormuz amid Middle East tensions. Elevated LNG prices also encouraged dual-fuel vessels to switch to conventional fuels, further reducing LNG bunker demand.

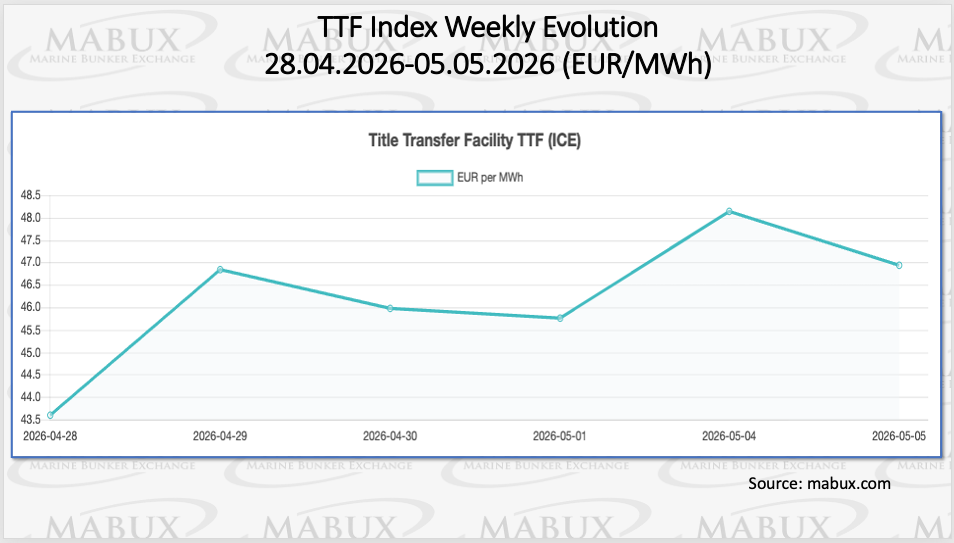

European underground gas storage facilities continued to record moderate gains as of May 5, with total storage occupancy reaching 34.07% of capacity, up 2.10 percentage points from the previous week. However, current occupancy levels remain 27.39% below the year-opening level of 61.46%. Meanwhile, the European TTF gas benchmark maintained its upward momentum, rising to EUR 46.926/MWh compared to EUR 43.594/MWh recorded last week.

The price of LNG as a bunker fuel at the port of Sines (Portugal) increased by another US$ 15.00 this week to US$ 1,105/MT, compared to US$ 1,090/MT last week. Meanwhile, the price difference between LNG and conventional fuel remained virtually unchanged at US$ 294 in favor of LNG. MGO LS was quoted at US$ 1,399/MT at the port of Sines on May 4.

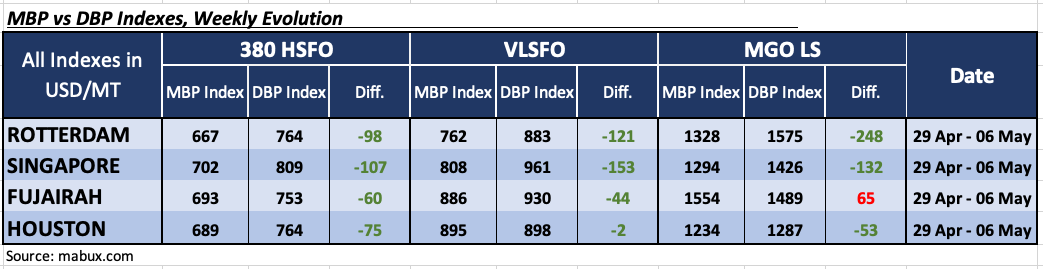

Amid persistently high market volatility and the ongoing blockade of the Strait of Hormuz, the MABUX Market Differential Index (MDI) — the ratio between market bunker prices (MBP) and the MABUX Digital Bunker Benchmark (DBP) — recorded the following trends across Rotterdam, Singapore, Fujairah, and Houston:

• 380 HSFO segment: All four ports remained in the undervalued zone. Discounts widened in Singapore and Houston, while Fujairah recorded a slight decline in undervaluation levels.

• VLSFO segment: Houston shifted into the undervalued zone, resulting in all four ports being undervalued. Rotterdam and Singapore maintained MDI levels above the US$ 100.00 threshold.

• MGO LS segment: Rotterdam, Singapore, and Houston remained undervalued, while Fujairah continued to be the only overvalued port in this segment.

“The prevailing trend toward undervaluation continues to strengthen across the bunker market,” Ivanov noted.

Ongoing tensions in the Middle East, combined with the continued blockade of the Strait of Hormuz and the absence of meaningful de-escalation, continue to leave the global bunker market highly sensitive to developments in the region.

“Any escalation could quickly trigger another sharp rise in bunker prices, while signs of diplomatic progress may support a corrective decline,” Ivanov concluded.