The Commission’s five priorities give every port in the Hamburg-Le Havre range

identical policy language. The ports that translate shared frameworks into

differentiated stakeholder narratives will capture disproportionate competitive

positioning value.

Within a week of the European Commission publishing its EU Ports Strategy on 4 March

2026, major port associations across the continent had issued responses. Not one of

those responses distinguished one port from its competitors.

The Commission’s framework – five priorities, twenty-eight pages, a new high-level

Maritime Industries and Ports Board – gives every European port the same policy

language, the same funding instruments, and the same strategic reference points. It

treats ports as infrastructure. It does not treat them as institutions competing for

stakeholder preference.

This is where the competitive implications begin. The ports that can translate this shared

framework into a differentiated competitive narrative will extract disproportionate value

from it. The ones that cannot will have co-signed a document that primarily strengthens

their rivals’ positioning.

Same policy framework, different narrative readiness

The five priorities in the EU Ports Strategy are sound: competitiveness and digitalisation,

energy transition, security, access to finance, and skills. The Commission correctly

recognises that EU ports handle 74% of external trade, move 3.4 billion tonnes of goods

annually, and support over 423,000 direct jobs. The document calls ports

“multi-functional industrial hubs,” which they are.

But the document does not address the widening gap between ports that communicate

their strategic position effectively and those that do not. Call it the narrative gap: the

distance between a port’s operational reality and its ability to make that reality visible to

the stakeholders who allocate capital, approve permits, and route cargo.

Consider what happened in the weeks before the Strategy launched. On 26 January, the

Port of Rotterdam officially published its Vision 2050, a generational positioning

document developed with more than 100 organisations, adopted by the Rotterdam City

Council in December 2025, and presented with the outgoing Dutch Minister of Economic

Affairs standing alongside CEO Boudewijn Siemons.

The five themes of that Vision – smart and clean logistics, competitive, climate-neutral and circular industry, healthy living environment, future-proof labour market, and agile and resilient – align closely with the EU Ports Strategy’s priorities.

That alignment is not coincidental. It is the result of a communication strategy operating

at the same level as operational strategy. When the EU Ports Strategy landed five weeks

later, Rotterdam was already the reference point. One port shaped how the policy

framework was interpreted. Others responded to it.

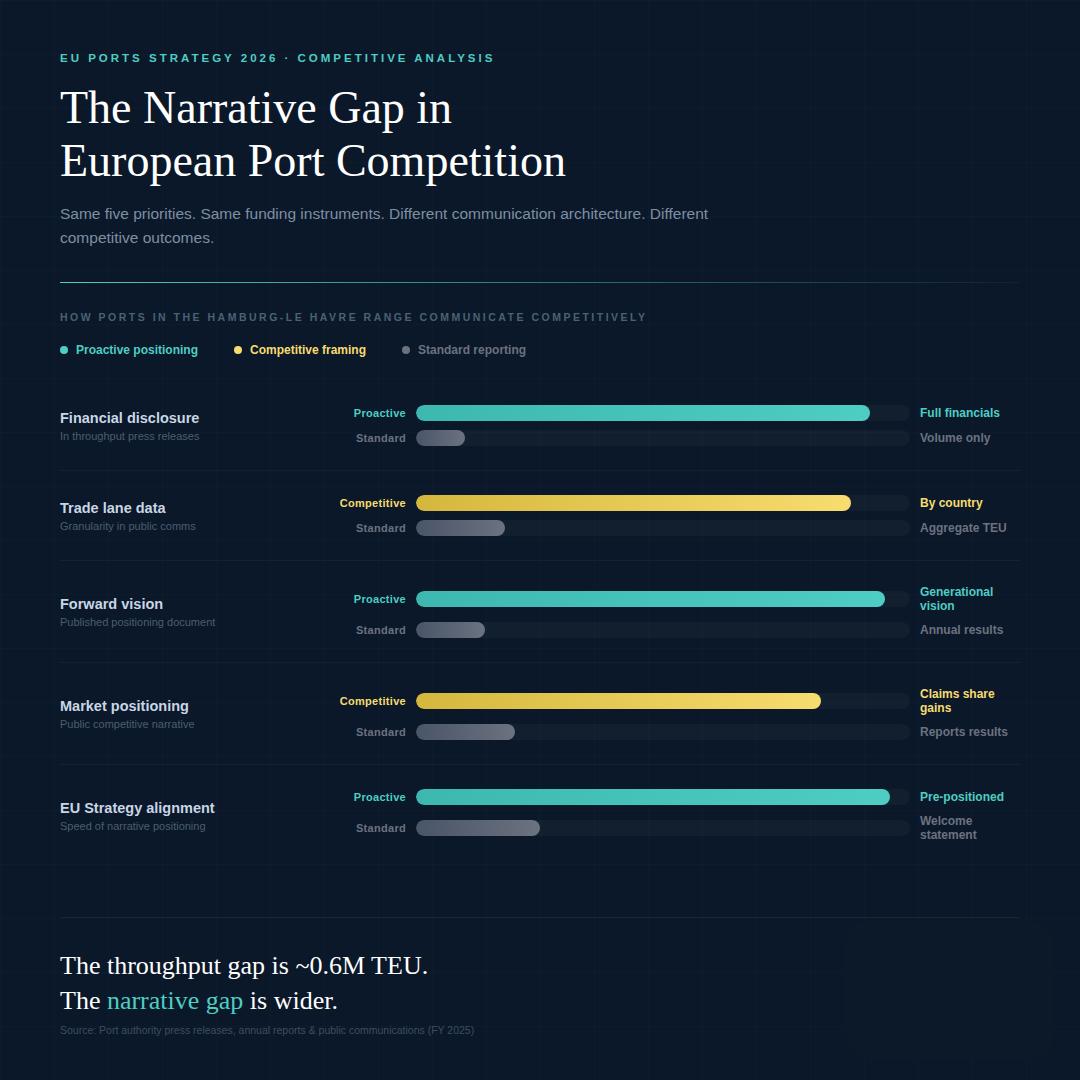

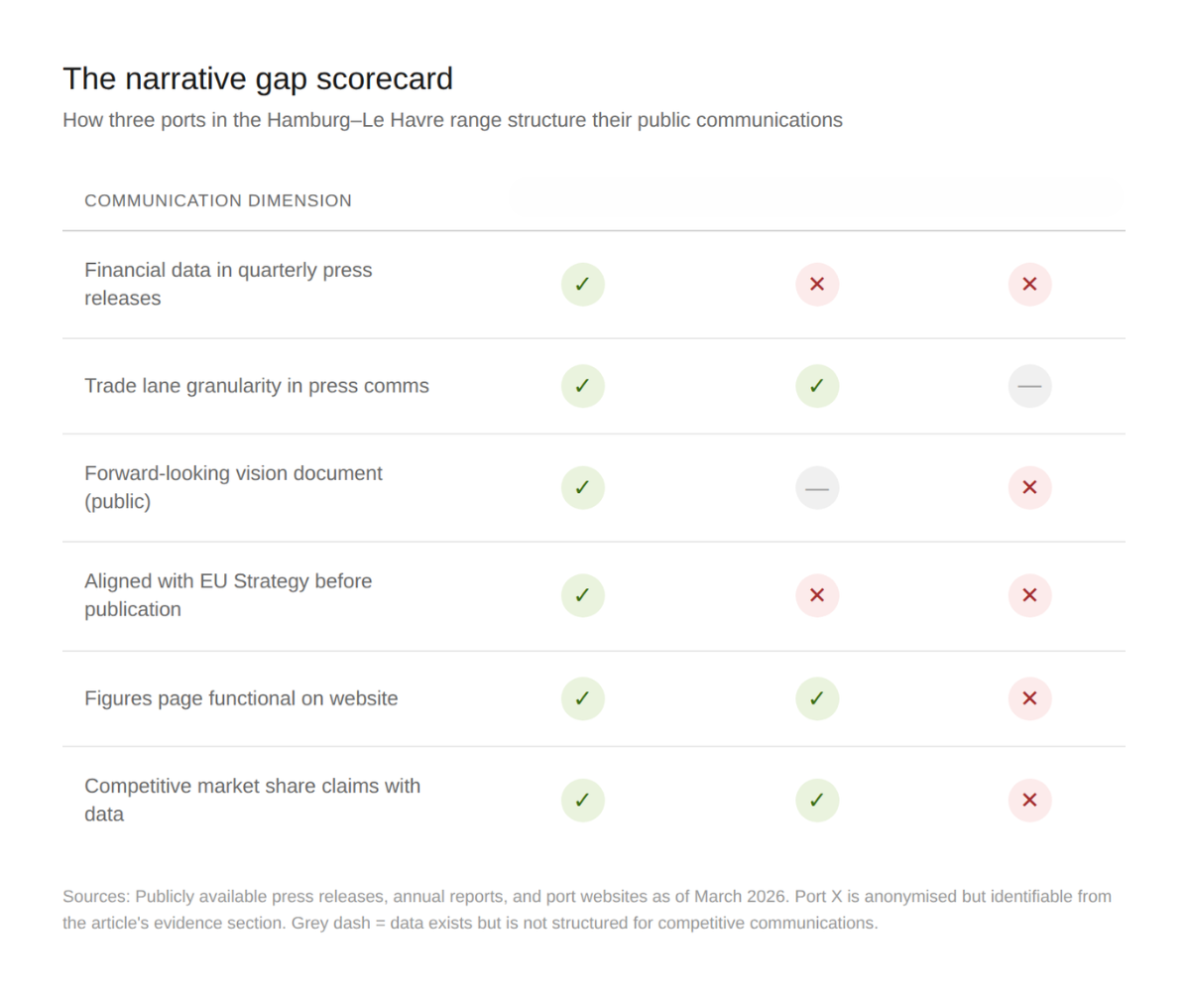

The narrative gap across the Hamburg-Le Havre range: information architecture, not data

The most common misreading of competitive positioning in this sector is that some ports

publish data and others do not. The evidence across the Hamburg-Le Havre range tells

a more specific story: the data often exists, but it is not structured to compete.

Hamburg puts country-by-country trade lane performance in its press release headlines:

China up 6.5%, India up 49.2%, Malaysia up 84.3% for full-year 2025, according to

Hafen Hamburg Marketing’s annual results. When Axel Mattern, CEO of Port of

Hamburg Marketing, stated during the H1 2025 results that Hamburg was “setting an

extremely positive example” compared to rival ports and gaining market share, the

granular data in those same communications supported the claim. The data was not just

available. It was positioned for a competitive narrative.

Rotterdam publishes port authority revenue (€940.4 million in 2025), EBITDA (€583.6

million), net profit (€266 million), and capital investment (€291.4 million) in every

throughput press release, according to the Port of Rotterdam Authority’s 2025 annual

results. Every journalist, analyst, policymaker, and industrial investor who reads a

Rotterdam quarterly update receives a financial health signal alongside the cargo

numbers.

Other ports in the range report throughput comprehensively but do not include financial

metrics in their press communications. The structural reasons vary. A corporatised entity

with national government co-ownership operates under different transparency

expectations than a public law company owned by municipal shareholders. Governance

models, disclosure obligations, and shareholder structures differ markedly across the

range. But the competitive effect is the same regardless of the cause. When one port

quantifies its institutional strength, and another describes it in qualitative terms,

stakeholders default to the quantified story.

This is where the nuance matters. Port of Antwerp-Bruges, Europe’s second-largest

container port and home to the continent’s largest integrated petrochemical cluster,

generating €21 billion in annual added value across 164,000 direct and indirect jobs, according to the port authority’s 2025 annual results, publishes comprehensive trade

area container breakdowns by region in its annual Statistical Yearbook. Europe, Africa,

North America, Latin America, the Middle East, the Far East: the data is detailed,

current, and downloadable.

But across the range, the pattern repeats: granular competitive data often lives in annual

publications rather than in the quarterly press communications and landing pages where

analysts and journalists look first. The data exists. The question is whether it reaches the

stakeholders making routing and investment decisions at the moment those decisions

are being shaped.

This is not a question of organisational capability. Antwerp-Bruges demonstrated

precisely the kind of strategic communication that drives competitive positioning when

CEO Jacques Vandermeiren addressed the European Industry Summit in February 2026

with a direct call for EU industrial policy action. The port’s Inbound Release Platform,

developed by the port authority and its subsidiary NxtPort in collaboration with The Way

Forward and Belgian Customs, and processing 219,000 unloading messages in October

2025, is among the most advanced digital customs platforms in any European port. The

2022 merger of the Port of Antwerp and Port of Zeebrugge was itself an exercise in

institutional transformation that few port authorities in Europe have attempted, let alone

completed.

The gap is not between capability and incapability. It is between institutional strength and

the routine information architecture that makes that strength visible to every stakeholder,

every quarter, through the channels where capital allocation and routing decisions are

actually shaped.

Why the EU Ports Strategy accelerates the communication gap

Every government affairs team in the Hamburg-Le Havre range has carefully read the

EU Ports Strategy. They have responded to its regulatory implications, engaged with the

Commission’s consultation, and mapped its funding instruments. That is their job, and

they have done it.

But reading a policy document and mining it for competitive narrative are two distinct

organisational functions. The ports extracting positioning value from the Strategy – the

ones that had their forward-looking vision aligned with the Commission’s priorities before

the document was published – are not doing it from the government affairs department.

They are doing it because their communications function has a seat at the strategy table,

not merely a brief after decisions are made.

That organisational pattern becomes more consequential now. Each priority in the EU

Ports Strategy creates stakeholder decision points: funding allocations, permitting

approvals, foreign ownership guidance, and industrial partnerships. At each point,

policymakers, investors, and industrial partners will compare ports against one another.

The ports with communication infrastructure to frame their value for each audience will

be first into those conversations. The ports without it will discover that strong operations

are necessary but not sufficient.

The throughput data from 2025 illustrates the stakes. The container volume gap

between Europe’s two largest container ports narrowed from approximately 3 million

TEU in 2019 to fewer than 300,000 TEU in 2024, before widening again to roughly

600,000 TEU in 2025 as Antwerp-Bruges contended with terminal congestion and

industrial action while Rotterdam’s container volumes grew faster. The trajectory is not

linear, but the direction over five years is clear: market positions across the Hamburg-Le

Havre range that appeared settled are now contested. Hamburg posted full-year

container growth of 7.3%, driven by surging Asian trade lanes. HAROPA Port surpassed

three million TEU for the second consecutive year since recovering to that level.

In this environment, operational performance alone does not determine competitive

outcomes. Hamburg’s growth narrative, Rotterdam’s institutional credibility narrative, and

HAROPA’s momentum narrative are not merely reflections of throughput performance.

They are strategic instruments deployed to influence the next round of shipping line

routing decisions, carrier terminal investments, and policymaker capital allocations.

No amount of narrative can fix a capacity constraint or resolve a labour dispute. But the

ports gaining competitive ground right now are not just operationally strong. They are

communicationally organised. Their narrative gap is small. Their competitors’ is not.

The positioning window is open, and it will not stay open

The EU Ports Strategy creates a positioning window. Over the next twelve to eighteen

months, every major European port will align its strategy documents, funding

applications, and stakeholder communications with the Commission’s five priorities. The

ports that do this first and most specifically – not merely echoing the Strategy’s language

but connecting it to verifiable, regularly published competitive data – will anchor their

position with the stakeholders who matter most.

Strong individual positioning does not weaken the European port system. It strengthens

each port’s ability to contribute to it. But for port authorities whose operational substance

exceeds their public narrative – and there are several in the range whose assets, trade

volumes, and industrial ecosystems deserve more visible positioning – the strategic

question is no longer whether to invest in communication infrastructure. It is how quickly

that investment can close the gap before competitors make it permanent.

This article was written by Rasha Hamdan, a brand and marketing strategist specialising in competitive positioning for complex enterprise and industrial organisations across European

markets.

Source attribution: All data points attributed inline to named sources (Port of

Rotterdam Authority 2025 annual results, Hafen Hamburg Marketing annual results, Port

of Antwerp-Bruges 2025 annual results, EU Ports Strategy document of 4 March 2026,

Port of Antwerp-Bruges newsroom).

Disclosure: The author has no commercial relationship with any port authority referenced in this article.