“100 days ago, on 29 September, the Minervagracht was to become the last ship to be attacked by the Houthis, at least for now. Forty-three days later, the Houthis declared an end to their attacks on ships. Despite this, traffic through the Suez Canal has not significantly increased and in the first week of 2026 remained 60% below the corresponding week in 2023, before ships started diverting around the Cape of Good Hope,” says Niels Rasmussen, Chief Shipping Analyst at BIMCO.

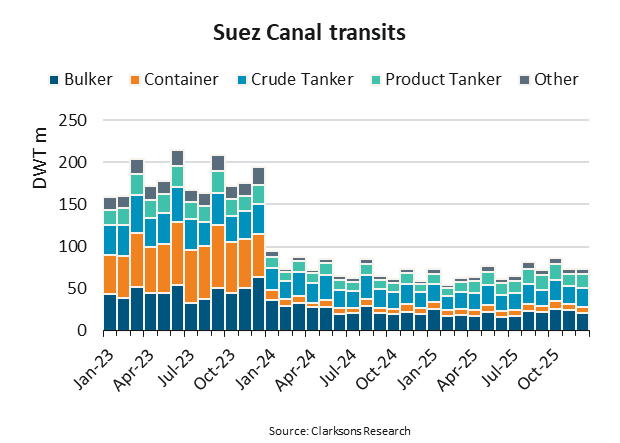

According to Lloyd’s List, the Houthis have attacked or hijacked ships 99 times since November 2023. Even though 15 ships were attacked during November and December of 2023, Suez Canal transits only saw significant reductions starting in January 2024. Since then, quarterly deadweight tonne (DWT) capacity transiting the Suez Canal have been 51-64% lower than in 2023.

“During 2025, Suez Canal DWT transits have been 57-64% lower than in 2023. In the fourth quarter, transits by bulkers, container ships, crude and product tankers were respectively 55%, 86%, 32% and 19% lower than in 2023,” says Rasmussen.

Throughout 2025, the reduction in Suez Canal transits has been stable for most shipping sectors. However, taking advantage of increasing freight rate premiums, product tankers have increasingly sailed via the Suez Canal. In the fourth quarter of 2025, transits were therefore only 19% lower than in 2023 compared to a 45% reduction in transits during 2024.

Nearly all container ships have avoided the Suez Canal since the attacks began. However, CMA CGM recently announced that their MEDEX and INDAMEX services would return to Suez Canal routings in January 2026.

Additionally, on 19 December 2025 the Maersk Sebarok become the first Maersk ship to transit the canal since early 2024. Maersk has not announced any further transits but has stated that “assuming that security thresholds continue to be met, we are considering continuing our stepwise approach towards gradually resuming navigation along the East-West corridor via the Suez Canal and the Red Sea.”

While the safety of crew, ship and cargo remains paramount, recent reductions in Red Sea war risk premiums may encourage more ships to revert to Suez Canal routings. In early December, S&P Global reported that premiums had fallen to 0.2% of hull values, the lowest since November 2023 and down from 0.5% before the Israel-Hamas ceasefire.

“A normalisation of ship transits now appears more likely than at any point during the last two years, but it remains unknown if, or how fast, this may happen. A return to the Suez Canal would reduce shipping companies’ costs significantly but also hurt ship demand. A full normalisation is estimated to reduce container ship demand by approximately 10% while other sectors could see 2-3% reductions,” says Rasmussen.