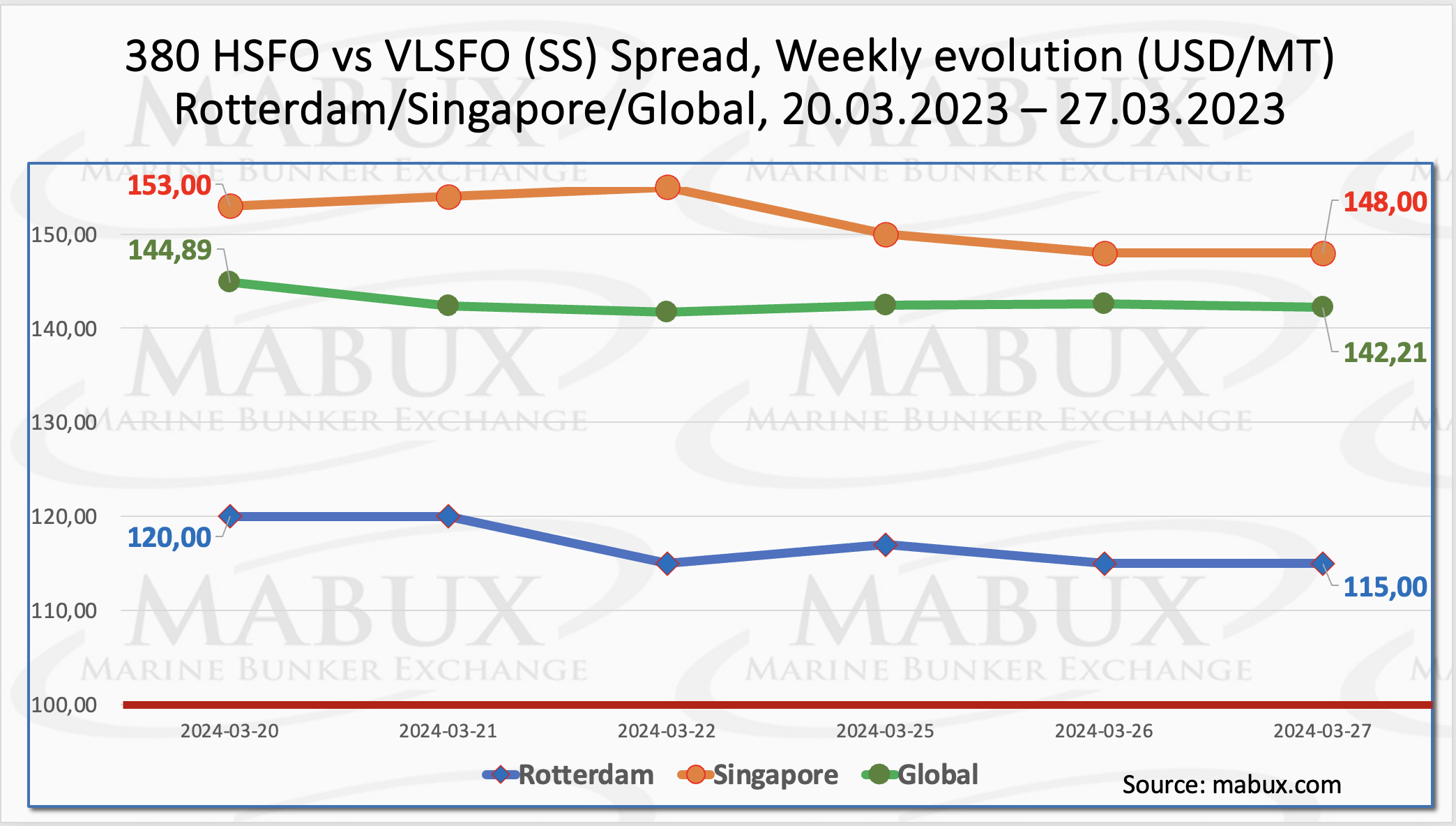

The MABUX Global Scrubber Spread (SS), representing the price gap between 380 HSFO and VLSFO, saw a moderate reduction of US$2.68, dropping from US$144.89 to US$142.21 compared to the previous week.

The average weekly value experienced a minimal decrease of US$0.01. Rotterdam observed a US$5 decrease in the SS Spread, declining from US$120 to US$115, approaching the US$100 benchmark (SS Breakeven).

The average weekly value in the port also decreased by US$7.83. Similarly, in Singapore, the price difference between 380 HSFO/VLSFO narrowed by US$5, from US$153 to US$148 compared to last week, with the average weekly value decreasing by US$5.50.

“We expect this moderate decline in the SS Spread to persist in the upcoming week,” said a MABUX official.

By 2030, it is forecasted that the launch of new liquefaction projects will significantly boost LNG production, potentially exceeding today’s global LNG trade by approximately 50%. This expansion is anticipated to mitigate market constraints and promote price stability. LNG supply is predicted to offer significant flexibility in adapting to fluctuations in European gas demand.

As of February 2024, global LNG imports exhibited minimal growth compared to the previous year, totalling 33.74 Mt. However, regions such as Asia Pacific, LAC, and MENA saw increases in LNG imports, offsetting the subdued imports observed in Europe and North America. From January to February 2024, global LNG imports rose by 3.7% (equivalent to 2.61 Mt year-on-year), reaching a total of 72.79 Mt, with the Asia Pacific region being the primary driver of this growth.

On 25 March, the price of LNG as bunker fuel at the port of Sines, Portugal, decreased to US$658/MT, marking a decline of US$21 compared to the previous week. Simultaneously, the price difference between LNG and conventional fuel remained steady, with LNG maintaining a US$242 advantage. Additionally, on the same day, MGO LS was priced at US$900/MT in the port of Sines.

During Week 13, the MDI index, which compares market bunker prices (MABUX MBP Index) to the MABUX digital bunker benchmark (MABUX DBP Index), displayed the following trends in four selected ports: Rotterdam, Singapore, Fujairah, and Houston.

In the 380 HSFO segment, all four selected ports continued to be undervalued. The average weekly undercharge margins decreased by 7 points in Rotterdam, 3 points in Fujairah, and 5 points in Houston. Throughout the week, Fujairah’s MDI index remained above the US$100 mark.

In the VLSFO segment, Rotterdam remained the sole undervalued port, with the average weekly ratio increasing by 2 points. The other ports were overpriced, with Singapore and Fujairah experiencing an 8-point decrease and Houston a 6-point increase in average weekly margins.

Regarding the MGO LS segment, Houston was the only overpriced port, with a 1-point weekly margin increase. The remaining three ports were underpriced, with Rotterdam and Fujairah experiencing decreases of 4 and 10 points, respectively, while Singapore saw a 4-point increase. Rotterdam and Singapore’s MDI indices remained slightly above the US$100 mark.

Throughout the week, the equilibrium between undervalued and overvalued ports across the 380 HSFO, VLSFO, and MGO LS segments remained consistent. The MDI index trends for the 380 HSFO and VLSFO segments are slowly shifting towards the undervaluation zone.

“We foresee a continued moderate downward trend in the global bunker market in the

upcoming week,” pointed out Sergey Ivanov, director of MABUX.