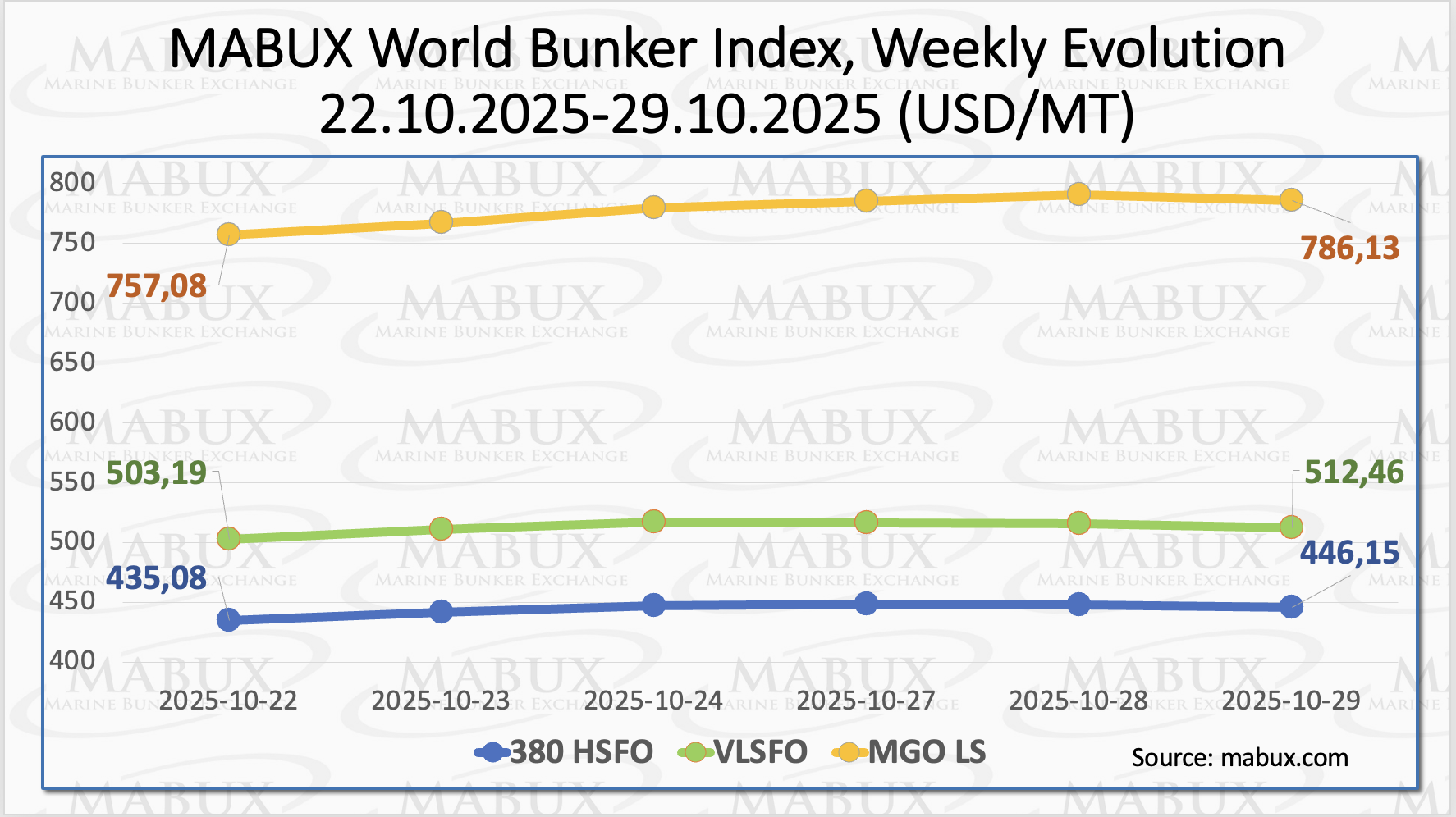

At the close of Week 44, global bunker indices by MABUX demonstrated an overall upward trend. However, by the end of the week, early signs of a downward correction began to emerge.

The 380 HSFO index increased by US$11.07, rising to US$446.15/MT, once again approaching the US$450 threshold. The VLSFO index added US$9.27, reaching US$512.46/MT. The MGO index also strengthened by US$29.05, climbing to US$786.13/MT.

”As of the time of writing, the global bunker market showed no clear price dynamics, with movements remaining moderate and mixed across key fuel grades”, commented Sergey Ivanov, Director, MABUX.

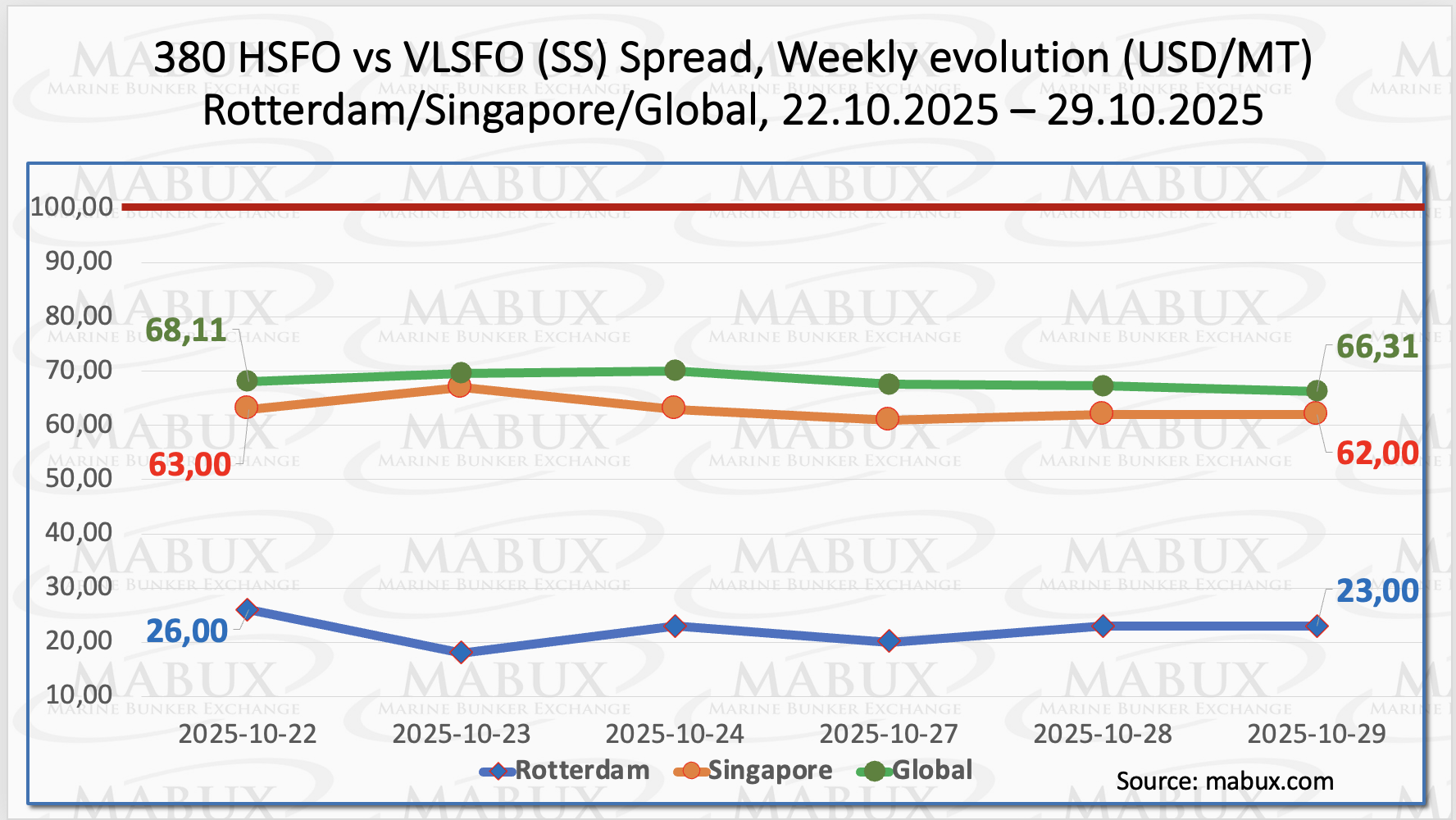

The MABUX Global Scrubber Spread (SS) — the price difference between 380 HSFO and VLSFO — continued to narrow, declining by US$1.80 (from US$68.11 last week to US$66.31), and remained consistently below the psychological threshold of US$100.00 (SS breakeven level).

In contrast, the average weekly value of the index showed a marginal increase of US$0.83. In Rotterdam, the SS Spread also continued to contract, losing US$3.00 (down to US$23.00). During the week, the spread temporarily fell to US$18.00 — its lowest level since October 2024.

The average weekly value in Rotterdam decreased by US$4.00. In Singapore, the 380 HSFO/VLSFO price differential slipped by US$1.00 (from US$63.00 to US$62.00), with the weekly average also easing by US$1.00.

The downward trend in the SS spread across the global bunker market persists, reinforcing the economic attractiveness of using conventional VLSFO over the HSFO + scrubber combination. No significant changes in SS spread dynamics are anticipated next week.

Electricity generation from gas-fired power plants in the EU increased by almost 50% in the first half of October compared to the same period last year. This significant increase was primarily driven by low hydropower generation (down 28%) and weaker winds, which led to a decline in wind power generation of almost 13% year-on-year.

Increased demand for gas generation led gas storage facilities to switch from injection to withdrawal much earlier than in previous years. This naturally impacted storage accumulation: net gas injections in the first half of October decreased more than tenfold compared to last year.

Wind power generation is becoming a key driver of winter gas demand in Europe, and the impact of wind speed on short-term gas price dynamics is likely to continue to increase in the coming years, as gas-fired power plants play an increasingly important role in the European energy system.

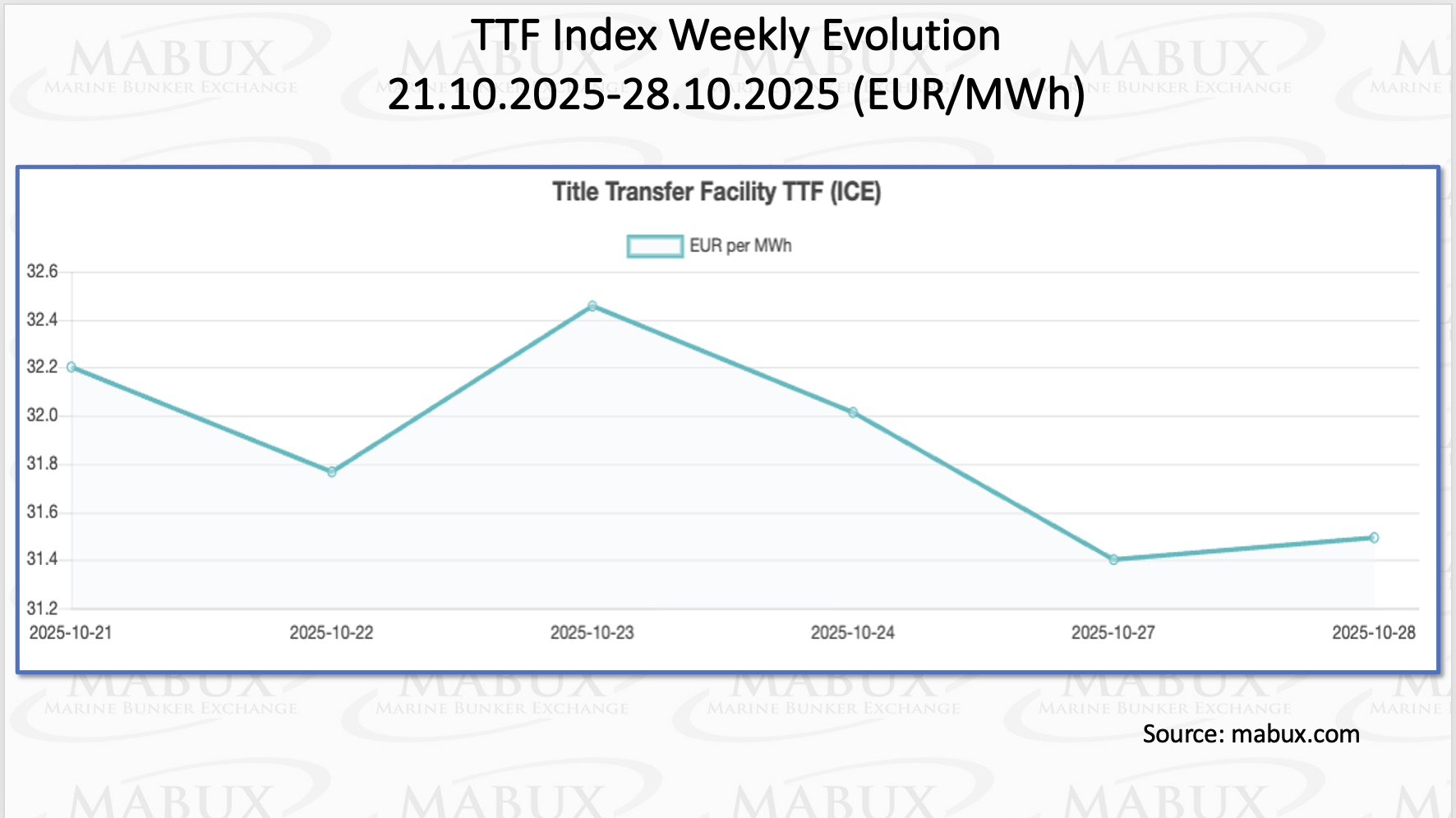

As of October 28, European regional gas storage facilities were 82.85% full, showing a marginal increase of 0.02% compared to the previous week. The storage occupancy rate thus remained virtually unchanged and continues to stand 11.52% higher than the 71.33% level recorded at the beginning of the year.

At the close of Week 44, the European TTF gas benchmark declined moderately by €0.706/MWh, down to €31.494/MWh from €32.200/MWh a week earlier.

According to MABUX assessments, the price of LNG as a bunker fuel at the port of Sines (Portugal) continued its moderate upward trend over the week, increasing by US$10.00 to US$745/MT, compared to US$735/MT the previous week. The price differential between LNG and conventional fuel shifted slightly in favor of LNG, standing at US$40, versus US$38 in favor of conventional fuel a week earlier. On the same day, MGO LS was quoted at US$785/MT at the port of Sines.

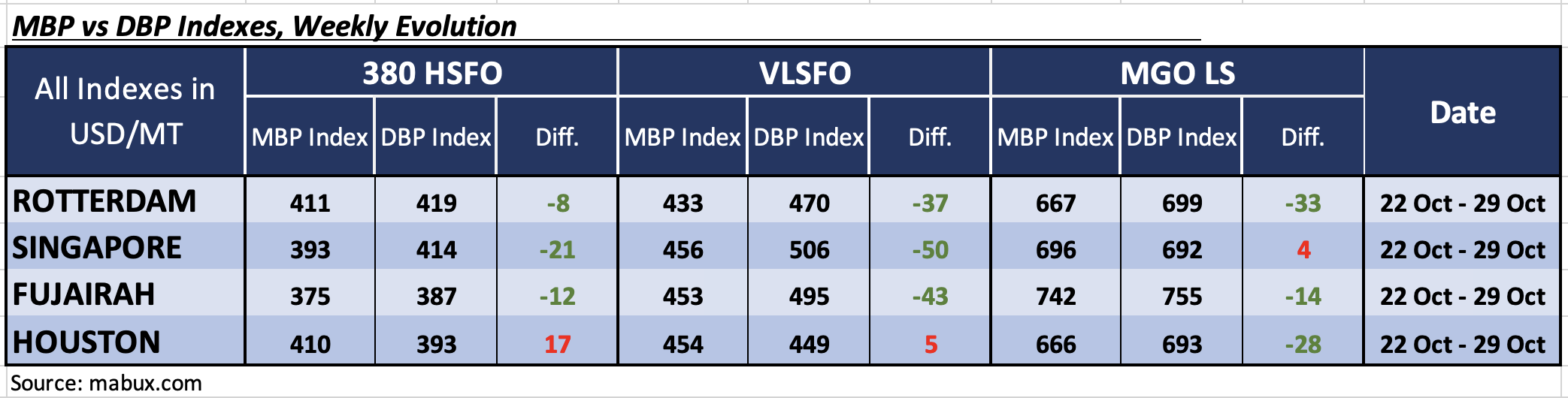

At the end of Week 44, the MABUX Market Differential Index (MDI) — representing the ratio of Market Bunker Prices (MBP) to the MABUX Digital Bunker Benchmark (DBP) — reflected the following price trends across the world’s major bunkering hubs: Rotterdam, Singapore, Fujairah, and Houston:

• 380 HSFO segment: Fujairah returned to the undervalued zone, joining Rotterdam and Singapore. Average weekly MDI values rose by 2 points in Rotterdam, 6 points in Singapore, and 13 points in Fujairah. Houston remained the only overvalued port in this segment, with its MDI falling by 6 points. The MDI in Rotterdam continues to hover near the 100% correlation between MBP and DBP.

• VLSFO segment: Houston also remained in the overvalued zone, with its average MDI close to a 100% correlation between MBP and DBP. All other ports were undervalued, with weekly MDI averages rising by 9 points in both Rotterdam and Singapore, and by 5 points in Fujairah.

• MGO LS segment: Fujairah moved into the undervalued zone, joining Rotterdam and Houston. MDI values increased by 28 points in Rotterdam, 33 points in Fujairah, and 24 points in Houston. Singapore remained the only overvalued port, with its MDI decreasing by 16 points and approaching the 100% correlation threshold.

Sergey Ivanov, Director, MABUX said that by the end of the week, the balance of overvalued versus undervalued ports shifted further toward undervaluation, as Fujairah became undervalued across all fuel grades. The undervaluation trend is expected to persist in the global bunker market over the coming week.

”We believe that, despite the emerging signs of a downward correction, the upward trend in bunker prices is likely to maintain its potential in the coming week” added Ivanov.