The latest round of China-US trade talks got underway in Madrid this week, with progress on a Tik Tok deal possibly a good sign for broader trade discussions.

The Trump administration extended 30% baseline tariffs on all imports from China for another 90-days a month ago in order to encourage further negotiations. And though the move has not led to a significant surge of transpacific container volumes since, it may have slowed the rate of declining demand.

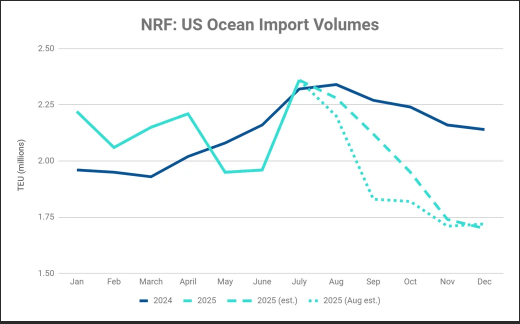

Frontloaded volumes that arrived ahead of tariff deadlines set for April and again for July and August have come at the expense of the typical strength of H2 US container imports relative to the first half of the year most years. The latest National Retail Federation US ocean import volume report estimates that H2 volumes will be down 10% year on year, with October imports 13% lower than a year ago and November and December volumes 20% lower.

The latest estimate for September import volumes, however, are 16% higher than the NRF’s September projections made at the beginning of August – just before the 90-day China tariff extension announcement – suggesting some positive impact on imports from the sustained 30% US tariffs on China.

Transpacific container rates to the West Coast increased slightly last week to $2,309/FEU, and are 34% higher than prices at the end of August. Rates to the East Coast climbed 4% last week to $3,368/FEU and have increased 24% so far this month. Prices climbed on early month General Rate Increases and were supported by some increase in demand ahead of the approaching Golden Week holiday in China and an increase in blanked sailings – and may have been helped by some volume increase due to the 30% China tariff extension.

The latest estimate for September import volumes, however, are 16% higher than the NRF’s September projections made at the beginning of August – just before the 90-day China tariff extension announcement – suggesting some positive impact on imports from the sustained 30% US tariffs on China.

Transpacific container rates to the West Coast increased slightly last week to $2,309/FEU, and are 34% higher than prices at the end of August. Rates to the East Coast climbed 4% last week to $3,368/FEU and have increased 24% so far this month. Prices climbed on early month General Rate Increases and were supported by some increase in demand ahead of the approaching Golden Week holiday in China and an increase in blanked sailings – and may have been helped by some volume increase due to the 30% China tariff extension.

Not everyone is convinced that the October 14th USTR port call fees on China-made vessels and operators will materialize, as the issue may be part of the ongoing US-China negotiations. But carriers are making moves to minimize their exposure nonetheless. And these adjustments may have also put some temporary upward pressure on rates as vessels and services were being shuffled.

Carriers will attempt additional mid-month GRIs for transpacific services this week, and though carriers are also increasing blanked sailings for the rest of September and October, demand trends have many observers anticipating rates will fall.

Asia-Europe container rates climbed 2% last week to $2,585/FEU, while prices to the Mediterranean dipped 4% to $2,833/FEU. Rates on both lanes have fallen about $200/FEU so far this week, signalling the coming end of this year’s peak season as Golden Week nears. Despite volume increases compared to last year though, rates significantly lower than the $5,000+/FEU prices seen last September reflect the effects of growing capacity on these lanes.

Steep US tariffs on imports from India are leading to reports of falling India-US air cargo demand as some shippers pause or cancel orders. Freightos Air Index South Asia – N. America rates have fallen 13% since July to $4.18/kg while prices to Europe have dipped only 2% to $2.92/kg. Ex-China rates were stable overall last week with prices to the US easing 1% to $5.24/kg, and rates to Europe ticking up 3% to $3.64/kg.

Judah Levine, Head of Research, Freightos Group (Nasdaq: CRGO)