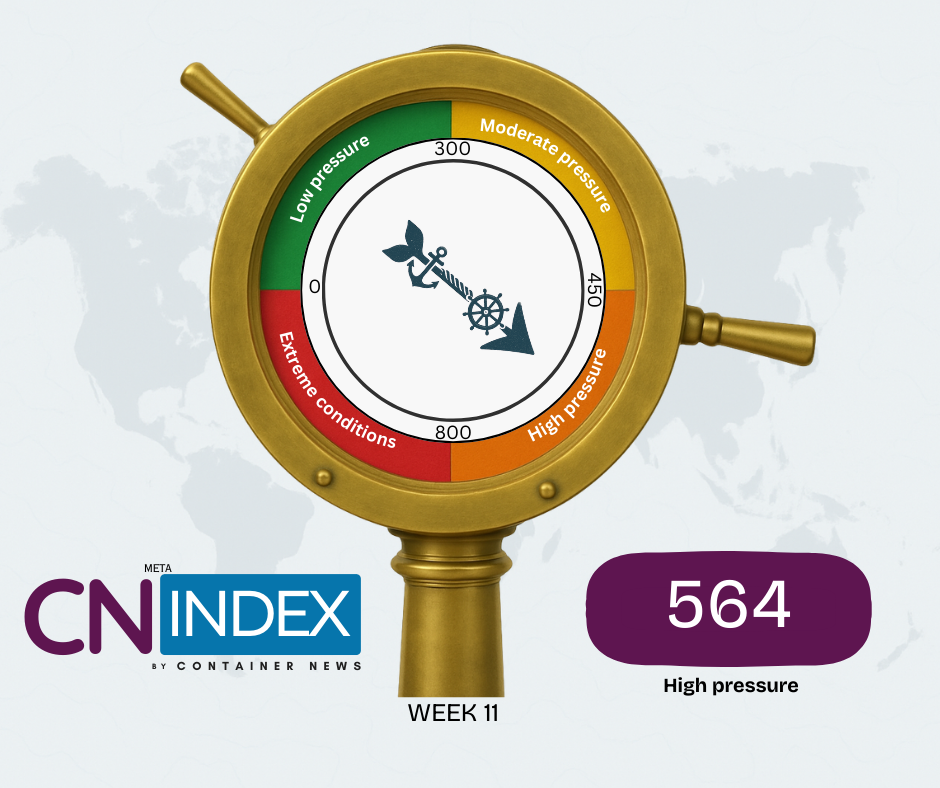

The CN Index increased this week, reaching 564, indicating that global container shipping remains firmly within the High Pressure range. The latest reading reflects a combination of strengthening freight rates across several trade lanes and persistently elevated geopolitical risks across key maritime corridors.

Freight Market Strength Returns on Select Routes

Freight rates across major trade lanes showed mixed but generally firmer movements this week. One of the most notable developments was the sharp increase on the Asia–South America East Coast corridor, which became the primary driver behind the rise in the CN Index. The surge highlights tightening capacity and strengthening demand dynamics on that route.

Elsewhere, the Far East–North Europe trade lane remained relatively stable compared with the previous week, while rates on the Asia–USEC and Asia–USWC corridors stayed softer but broadly steady. These movements suggest that while the trans-Pacific market continues to stabilize, other intercontinental corridors are beginning to absorb more demand and pricing momentum.

Regional trades also strengthened. Intra-Asia rates increased, while Mediterranean and Persian Gulf services recorded modest gains, reflecting improving utilization and more disciplined capacity management. Routes serving Africa and Australasia also edged higher, reinforcing the broader trend of moderate price recovery across secondary markets.

Geopolitical Risks Continue to Support Market Pressure

Geopolitical risks remain a significant contributor to overall shipping pressure. The Red Sea corridor continues to operate under elevated security risk, sustaining rerouting strategies and higher operating costs for carriers. Meanwhile, tensions involving Iran and the United States continue to elevate risk perception in the Strait of Hormuz, adding uncertainty to global maritime trade flows.

Although the Suez Canal remains operational, the broader regional security environment continues to influence carrier decisions and insurance costs. In addition, ongoing trade sanctions and geopolitical tensions continue to increase compliance complexity and operational planning challenges.

What the CN Index Is Indicating

At 564, the CN Index suggests that global container shipping pressure has strengthened slightly after several weeks of gradual easing. While freight markets had begun to stabilize, rising regional demand and persistent geopolitical risk are reinforcing upward pressure across the system. The index indicates that the market remains tight and sensitive to both demand shifts and geopolitical developments.