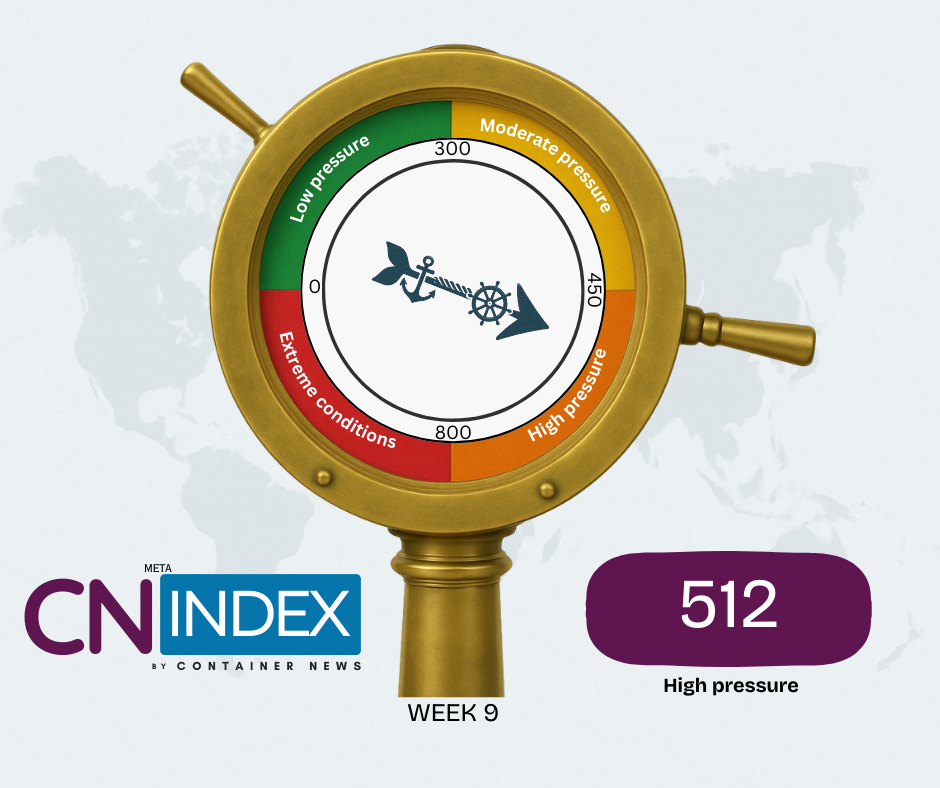

The CN Index declined to 512 this week, signaling that global container shipping remains in the High Pressure range, although conditions continue to ease incrementally. The latest reading reflects softer freight rates across major East–West trade lanes, combined with a modest reduction in geopolitical risk intensity.

Freight Rates Continue to Moderate

Pricing on the primary intercontinental corridors moved lower again. Rates on the Asia–USEC and Asia–USWC routes declined week on week, suggesting improved capacity availability and a more balanced demand environment following earlier volatility. The Far East–North Europe corridor also recorded softer pricing, reinforcing the gradual cooling trend across the Asia–Europe trade.

While freight levels remain above long-term structural averages, the pace of decline indicates that peak tightness has likely passed for now. Regional trades, including intra-Asia, Mediterranean, and Persian Gulf routes, remained relatively stable but subdued compared with earlier highs. Overall, the market component continues to drive the easing trajectory of the CN Index.

Geopolitical and Structural Factors

Geopolitical risks remain elevated but stable. The Red Sea continues to represent the most significant operational concern, while broader trade and sanctions dynamics maintain upward pressure on compliance costs and routing decisions. War-risk premiums in the Black Sea and security considerations in parts of West Africa persist but showed no material escalation this week.

Beyond pricing and security, structural industry developments also shaped sentiment. Hapag-Lloyd’s acquisition of ZIM signals further consolidation among global carriers, reinforcing long-term capacity discipline.

Meanwhile, the U.S. Supreme Court ruling overturning sweeping global tariffs imposed under the IEEPA removes a layer of trade-policy uncertainty that had weighed on forward planning. In parallel, continued post–Lunar New Year capacity management suggests carriers remain focused on balancing supply and demand as volumes stabilize.

What the CN Index Is Signaling

At 512, the CN Index indicates that global container shipping pressure is easing but remains firmly in high territory. Freight markets are softening, yet geopolitical risk and disciplined capacity management continue to prevent a rapid normalization of conditions.