The global bunker market continues to exhibit pronounced volatility amid the escalating conflict in the Middle East, which is disrupting global supply chains and contributing to widespread bunker fuel shortages across all major hubs.

Over the past week, bunker indices have maintained an upward trajectory, with signs of stabilization near recently reached highs. According to Sergey Ivanov, Director, MABUX, “The market remains highly sensitive to geopolitical developments, with supply disruptions continuing to drive extreme price volatility.”

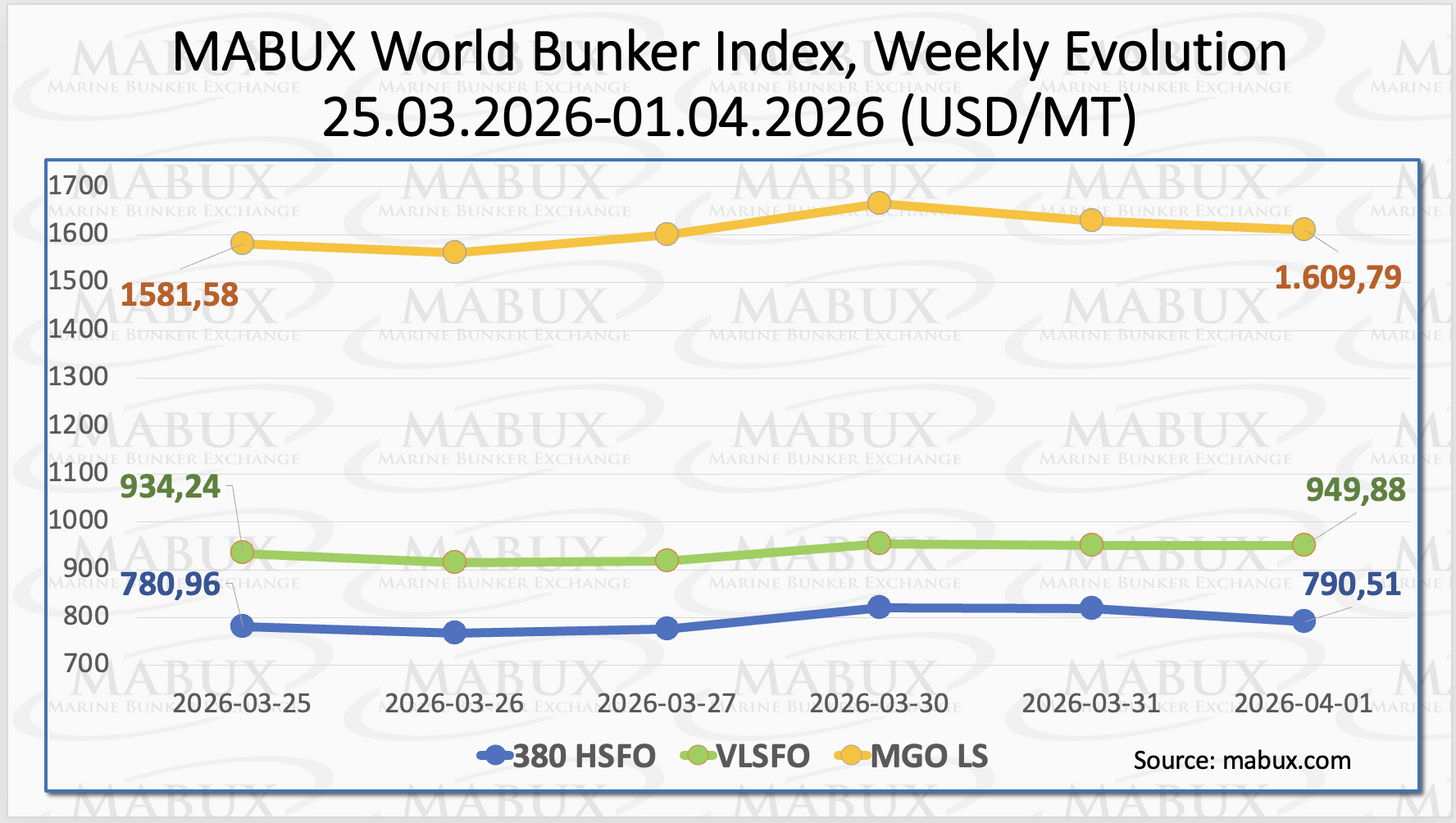

The 380 HSFO Index increased by US$ 9.55, rising from US$ 780.96/MT to US$ 790.51/MT. The VLSFO Index gained US$ 15.64, advancing to US$ 949.88/MT from US$ 934.24/MT the previous week.

Meanwhile, the MGO LS Index recorded the most significant growth, climbing by US$ 28.21 from US$ 1,581.58/MT to US$ 1,609.79/MT. Notably, this marks the first time the MGO LS Index has exceeded the US$ 1,600.00 threshold, setting a new all-time high for the entire MABUX data series since 2001.

At the time of writing, the global bunker market remains characterized by sharp, multidirectional price fluctuations, reflecting ongoing uncertainty and heightened geopolitical risk. Sergey Ivanov commented that despite signs of stabilization, the market lacks the conditions necessary for a sustained trend.

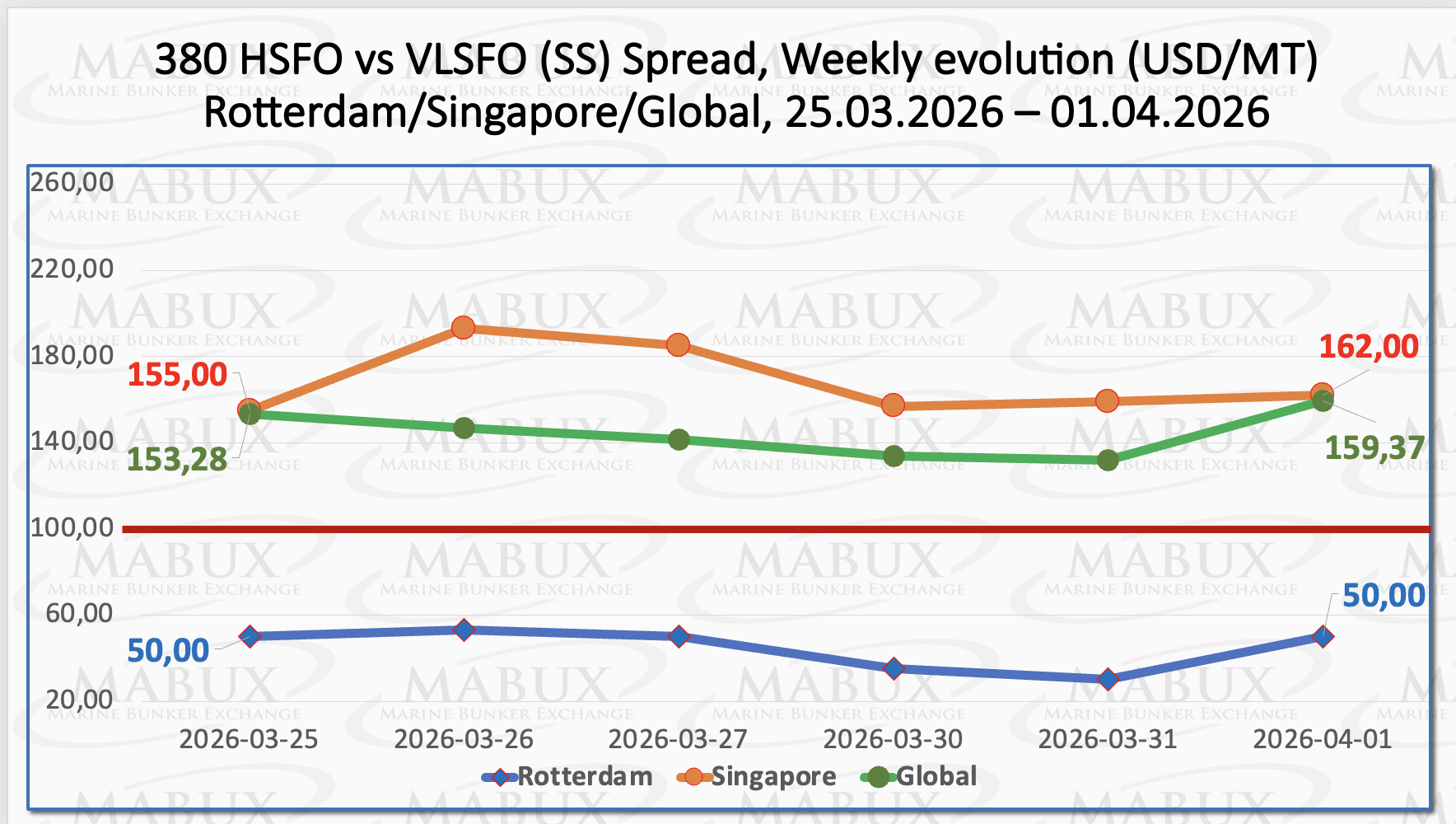

The MABUX Global Scrubber Spread (SS)—the price differential between 380 HSFO and VLSFO—widened by US$ 6.09, increasing from US$ 153.28 last week to US$ 159.37. The spread remains firmly above the psychological breakeven threshold of US$ 100.00. However, the weekly average of the index declined by US$ 5.27, indicating underlying instability despite the headline increase.

In Rotterdam, the SS Spread remained unchanged at US$ 50.00, while its weekly average edged down by US$ 2.83. In Singapore, the spread expanded by US$ 7.00, rising from US$ 155.00 to US$ 162.00, and briefly spiked to US$ 193.00during the week. Nevertheless, the port’s weekly average decreased significantly by US$ 31.17.

Sergey Ivanov added: “Persistent volatility continues to distort SS Spread dynamics, making it difficult for the market to establish a clear direction.”

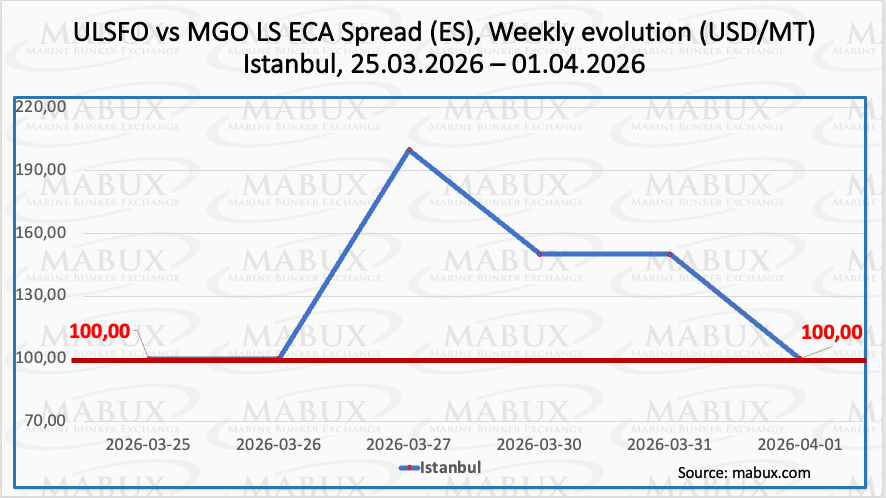

The Istanbul ECA Spread (ES) closed the week unchanged at US$ 100.00, despite surging to a peak of US$ 200.00 amid heightened market volatility. The weekly average also remained stable overall. The Venice ECA Spread remains suspended due to the absence of consistent market quotations. Ivanov said that distillate markets remain particularly vulnerable to supply shocks under current geopolitical conditions.

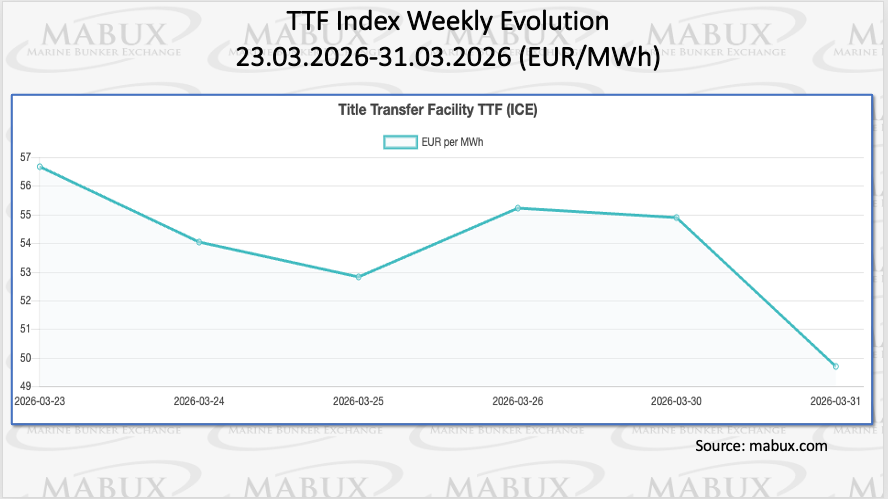

According to Standard Chartered, European gas prices are expected to maintain a firm upward trajectory amid ongoing geopolitical uncertainty. TTF benchmark prices could exceed €80/MWh—levels last observed in 2022—should the US–Iran conflict remain unresolved by the onset of the summer injection season. Moreover, strength along the forward curve, extending towards 2028, suggests that the market is pricing in a prolonged period of elevated gas prices.

As of 31 March, European underground gas storage levels continued their downward trajectory, declining to 28.05% of total capacity, a decrease of 1.24 percentage points week-on-week. Storage levels are now 33.41 percentage pointsbelow those recorded on 1 January 2026 (61.46%). A relatively severe winter across continental Europe contributed to stronger-than-anticipated heating demand, accelerating the depletion of inventories. At the same time, the European TTF gas benchmark declined by EUR 6.98/MWh to EUR 49.70/MWh, compared to EUR 56.68/MWh the previous week, remaining close to the EUR 50.00/MWh level.

The price of LNG as a bunker fuel at the port of Sines (Portugal) declined sharply by US$ 152, falling to US$ 1,312/MTfrom US$ 1,464/MT the previous week. At the same time, the price differential between LNG and conventional fuel shifted in favor of LNG, widening to US$ 195, compared to a US$ 21 advantage for conventional fuel a week earlier. As of March 30, MGO LS was quoted at US$ 1,507/MT in the port of Sines.

Sergey Ivanov commented: “Price swings in LNG and conventional fuels reflect broader instability in global energy markets, particularly under supply constraints.”

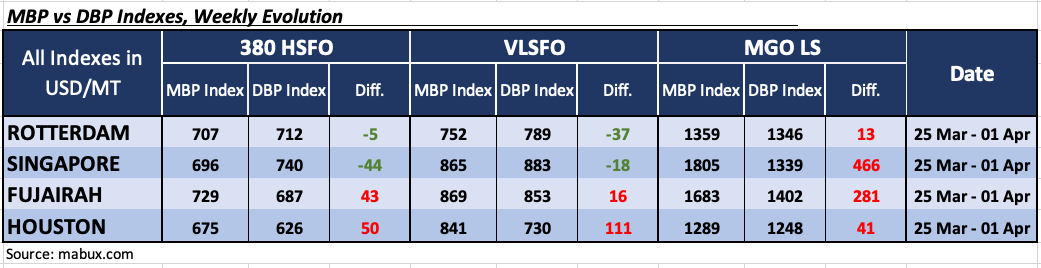

Amid the ongoing escalation of the conflict in the Middle East, the MABUX Market Differential Index (MDI)—which reflects the ratio between market bunker prices (MBP) and the MABUX digital bunker benchmark (DBP)—demonstrated mixed dynamics over the week, with no consistent trend observed across the major global hubs of Rotterdam, Singapore, Fujairah, and Houston:

• 380 HSFO segment: Rotterdam and Singapore shifted into the undervalued zone, with their MDI levels increasing by 57 and 114 points, respectively. Fujairah and Houston remained in the overvalued zone, although their premiums narrowed by 144 and 18 points.

• VLSFO segment: Rotterdam and Singapore also entered the undervalued zone, with discounts widening by 62 and 147 points. Fujairah and Houston remained overvalued, with Fujairah’s premium declining sharply by 219 points, while Houston recorded a marginal increase of 8 points.

• MGO LS segment: Rotterdam returned to the overvalued zone, resulting in all four hubs being classified as overvalued. Premiums increased by 43 points in Rotterdam and 26 points in Houston, while declining by 30 points in Singapore and 54 points in Fujairah.

The pronounced volatility in the MDI and divergence in valuation trends are primarily driven by sharp price fluctuations amid persistent supply tightness in global bunker markets. Sergey Ivanov concluded: “As long as geopolitical tensions persist, bunker markets will remain highly unstable, with strong price support but no clear directional trend.”