Since the announcement of the ceasefire in the Middle East on April 8, the global bunker market has entered a phase of temporary stabilization, accompanied by a moderate downward correction. “The market is stabilizing, but downward pressure remains dominant,” said Sergey Ivanov, Director, MABUX.

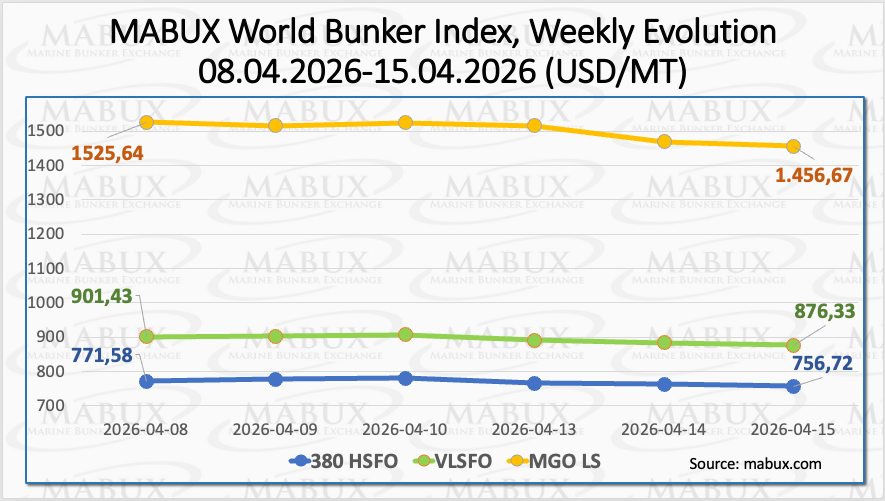

By the end of the week, the 380 HSFO index declined by US$ 14.86, falling from US$ 771.58/MT to US$ 756.72/MT. The VLSFO index dropped by a further US$ 25.10, from US$ 901.43/MT to US$ 876.33/MT, breaking below the US$ 900.00 threshold. The MGO LS index recorded the most significant decrease, down by US$ 68.97 from US$ 1,525.64/MT to US$ 1,456.67/MT, also breaching the US$ 1,500.00 level.

MGO LS continues to represent the most volatile segment of the global bunker market. At the time of writing, no clear directional trend has yet emerged in the dynamics of global indices.

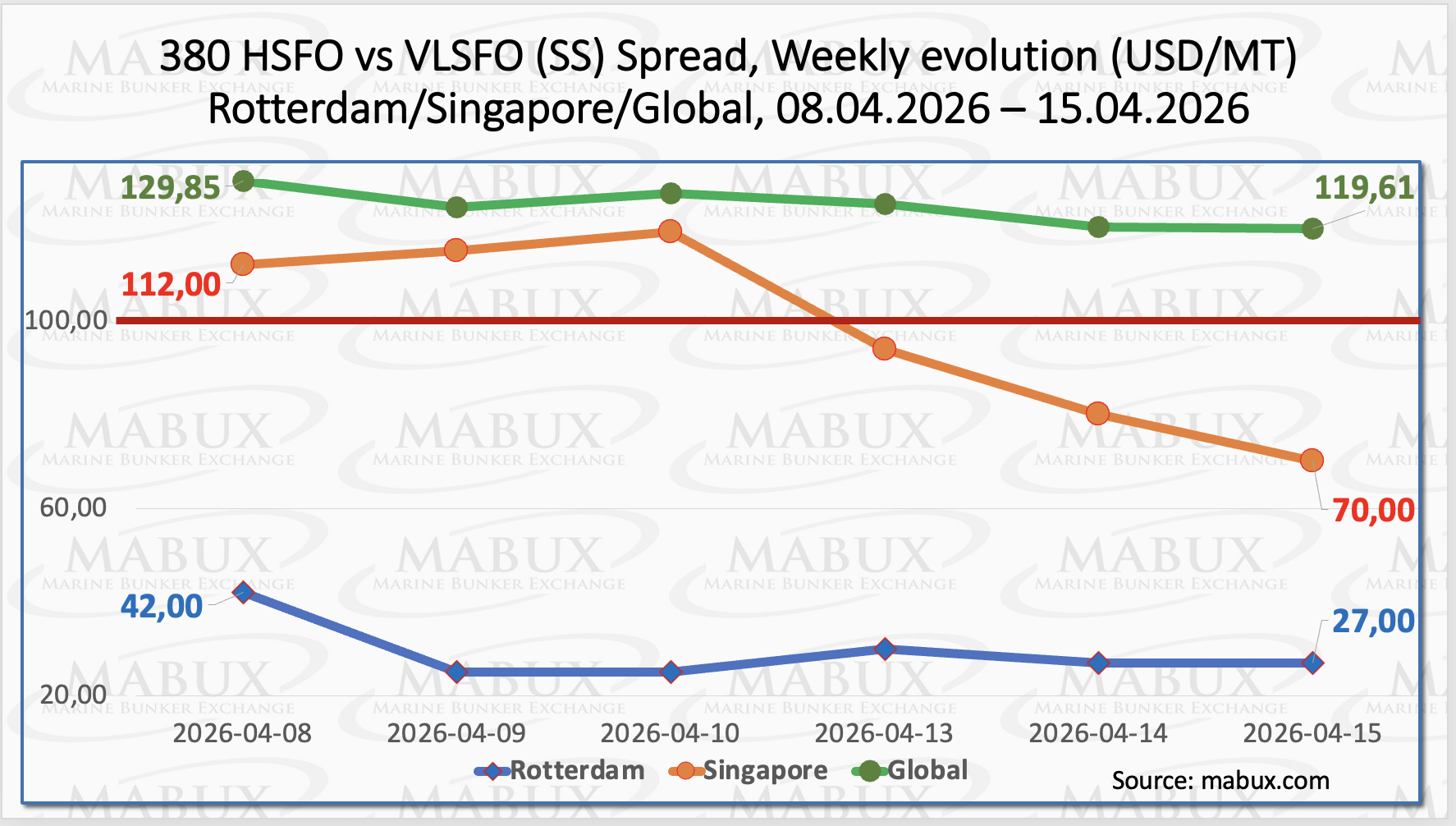

The MABUX Global Scrubber Spread (SS)—the price differential between 380 HSFO and VLSFO—entered a contraction phase, declining by US$ 10.24 from US$ 129.85 to US$ 119.61, thus falling below the US$ 120.00 mark. Despite this decrease, the spread remains comfortably above the psychological threshold of US$ 100.00 (SS breakeven). The weekly average of the index also edged down by US$ 10.22.

At the port level, Rotterdam recorded a decline in the SS Spread of US$ 15.00, from US$ 42.00 to US$ 27.00, briefly touching the US$ 25.00 level. The weekly average in Rotterdam decreased by US$ 2.67. In Singapore, the spread narrowed more sharply, dropping by US$ 42.00 from US$ 112.00 to US$ 70.00, thereby breaking below the US$ 100.00 mark. The weekly average in Singapore also fell significantly, down by US$ 42.17. “We expect the SS Spread to continue its downward movement,” Ivanov added.

The MABUX Global Scrubber Spread (SS)—the price differential between 380 HSFO and VLSFO—entered a contraction phase, declining by US$ 10.24 from US$ 129.85 to US$ 119.61, thus falling below the US$ 120.00 mark. Despite this decrease, the spread remains comfortably above the psychological threshold of US$ 100.00 (SS breakeven). The weekly average of the index also edged down by US$ 10.22. At the port level, Rotterdam recorded a decline in the SS Spread of US$ 15.00, from US$ 42.00 to US$ 27.00, briefly touching the US$ 25.00 level. The weekly average in Rotterdam decreased by US$ 2.67. In Singapore, the spread narrowed more sharply, dropping by US$ 42.00 from US$ 112.00 to US$ 70.00, thereby breaking below the US$ 100.00 mark. The weekly average in Singapore also fell significantly, down by US$ 42.17. “We expect the SS Spread to continue its downward movement,” Ivanov added.

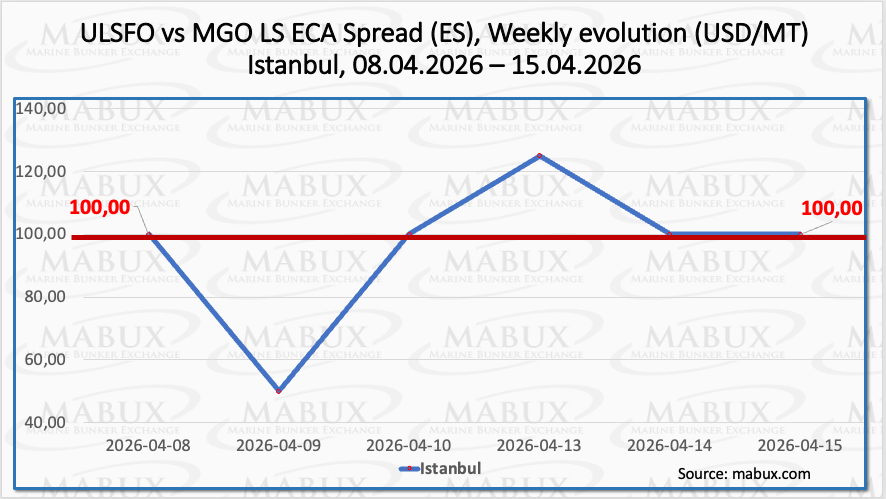

The Istanbul ECA Spread (ES) closed the week unchanged at US$ 100.00. However, against a backdrop of heightened market volatility, the index exhibited significant mixed fluctuations within a broad range of US$ 50.00–125.00. The weekly average declined by US$ 27.50. The calculation of the Venice ECA Spread has been temporarily suspended due to the absence of regular market quotations. Amid the ongoing de-escalation of the conflict in the Middle East, we expect the ECA Spread to remain near current levels in the short term, while continuing to display mixed fluctuations.

Europe’s gas prices have softened in recent weeks; however, the market appears to be underpricing emerging supply-side risks. Structural pressures are expected to intensify in the coming months, driven by below-average storage levels and ongoing disruptions to LNG flows—particularly from Qatar amid heightened geopolitical tensions in the Middle East. This leaves Europe increasingly exposed as it competes with Asia for constrained global supply. Even in the event of a ceasefire, normalization of LNG flows is likely to be gradual, suggesting that market tightness and elevated price levels will persist through the summer period and potentially extend beyond.

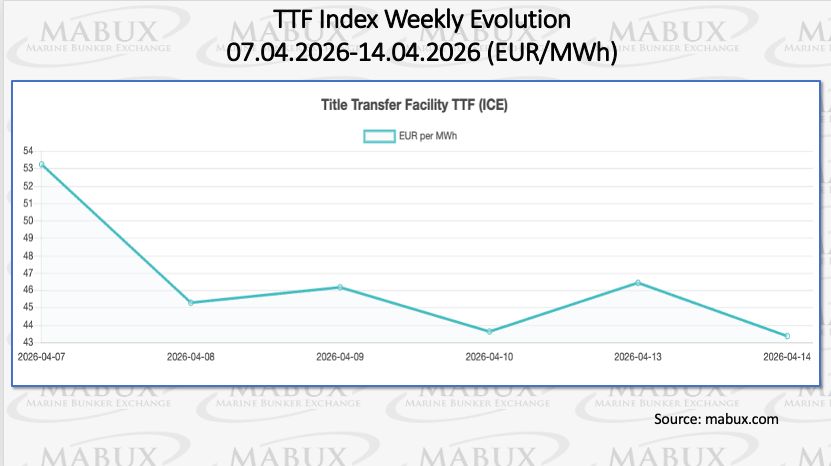

As of April 14, the level of natural gas in European underground storage facilities showed a slight increase, reaching 29.55% of total capacity, up by 0.94 percentage points compared to the previous week. However, current storage levels remain significantly lower—by 31.91%—than those recorded on January 1, 2026 (61.46%). At the end of Week 16, the European gas benchmark TTF recorded a notable decline, falling by EUR 9.882/MWh from EUR 53.247/MWh to EUR 43.365/MWh, thereby dropping below the EUR 50.00/MWh threshold.

The price of LNG as a bunker fuel at the port of Sines (Portugal) continued its downward trend, declining by a further US$ 102.00 week-on-week to US$ 1,047/MT (from US$ 1,149/MT previously). As a result, the price differential between LNG and conventional marine fuel narrowed to US$ 440 in favor of LNG, compared to US$ 476 the week before. On April 13, MGO LS at the port of Sines was quoted at US$ 1,630/MT.

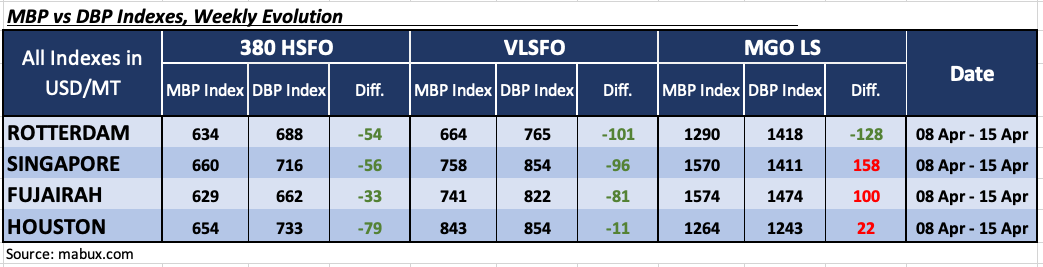

Amid the ongoing conflict in the Middle East, the MABUX Market Differential Index (MDI)—which reflects the ratio between market bunker prices (MBP) and the MABUX digital bunker benchmark (DBP)—demonstrated the following trends across the world’s largest hubs: Rotterdam, Singapore, Fujairah, and Houston:

• 380 HSFO segment: All ports remained undervalued. Discount levels increased by 13 points in Rotterdam, 19 points in Singapore, and 24 points in Fujairah, while Houston recorded a decrease of 14 points.

• VLSFO segment: All ports were also undervalued, with MDI discounts widening by 12 points in Rotterdam, 46 points in Singapore, 44 points in Fujairah, and 6 points in Houston.

• MGO LS segment: Rotterdam remained the only undervalued port, with the average discount increasing by 25 points. The other three ports continued to be overvalued; however, overvaluation levels declined significantly—by 239 points in Singapore, 92 points in Fujairah, and 34 points in Houston.

“Amid the ceasefire, we do not expect major shifts in MDI dynamics in the near term,” Ivanov commented. Overall, the balance between overvalued and undervalued ports remained unchanged during the week.

“The ceasefire has brought temporary stability, but volatility remains high,” Ivanov said. The current two-week ceasefire agreement in the Middle East conflict zone has contributed to a relative stabilization of the bunker market, with a downward correction emerging as the dominant trend. We expect this trend to persist into next week; however, the market is likely to remain highly volatile and sensitive to geopolitical developments.