The upward trajectory of bunker prices, driven by escalating tensions in the Middle East, reversed sharply on April 8 following reports of a two-week ceasefire. “The market has entered a corrective phase after a prolonged rally,” said Sergey Ivanov, Director, MABUX.

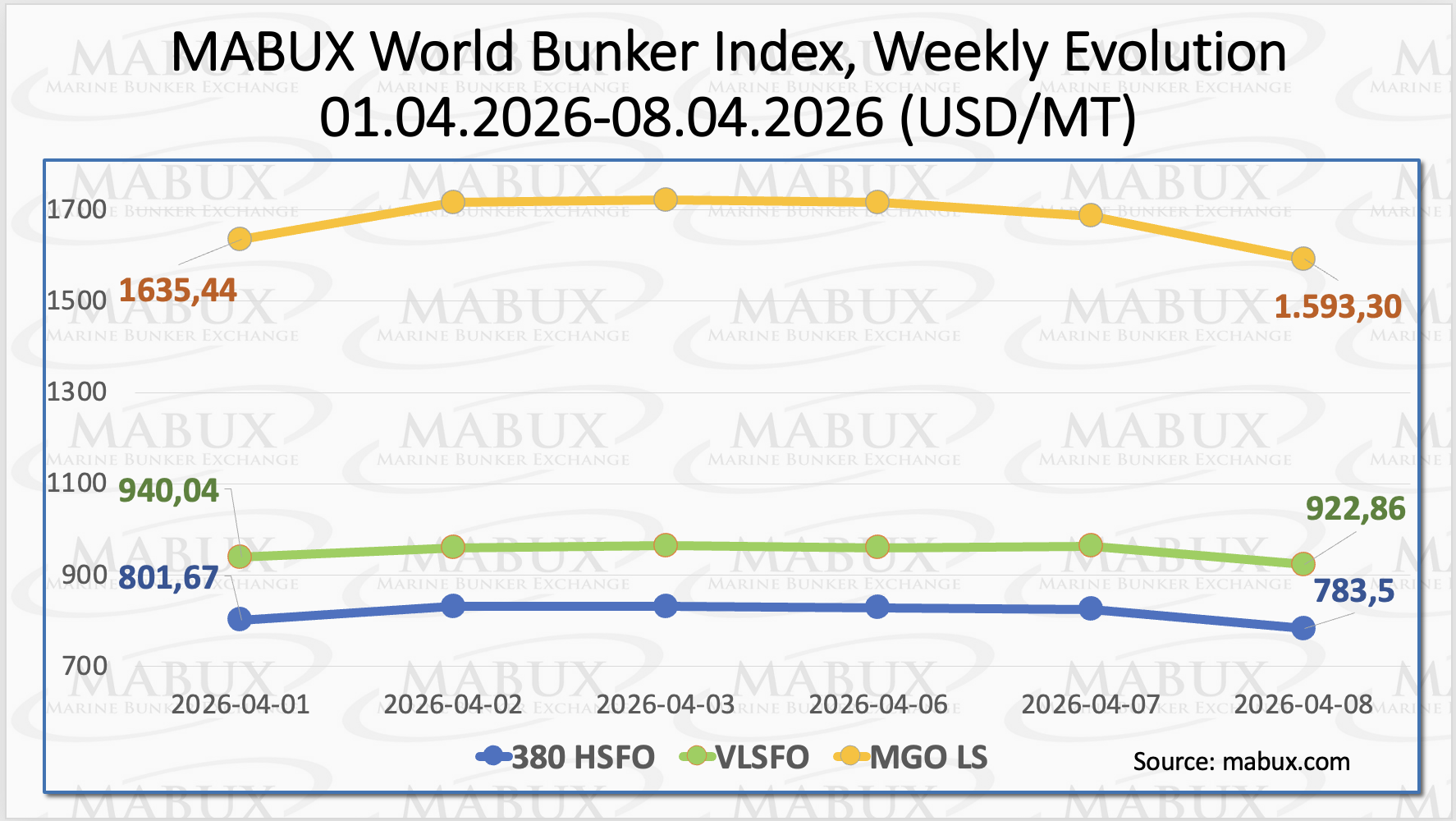

After an extended period of gains, global bunker indices entered a corrective phase, reflecting a shift in market sentiment. The 380 HSFO index declined by US$ 18.17, falling from US$ 801.67 per MT last week to US$ 783.50 per MT, once again moving below the US$ 800 threshold.

The VLSFO index also decreased by US$ 18.18, from US$ 940.04 per MT to US$ 922.86 per MT. Meanwhile, the MGO LS index recorded a more pronounced drop of US$ 42.14, declining from US$ 1635.44 per MT to US$ 1593.30 per MT, and similarly breaking below the US$ 1600 mark. At the time of writing, the global bunker market remains under downward pressure, with corrective dynamics continuing to dominate price movements.

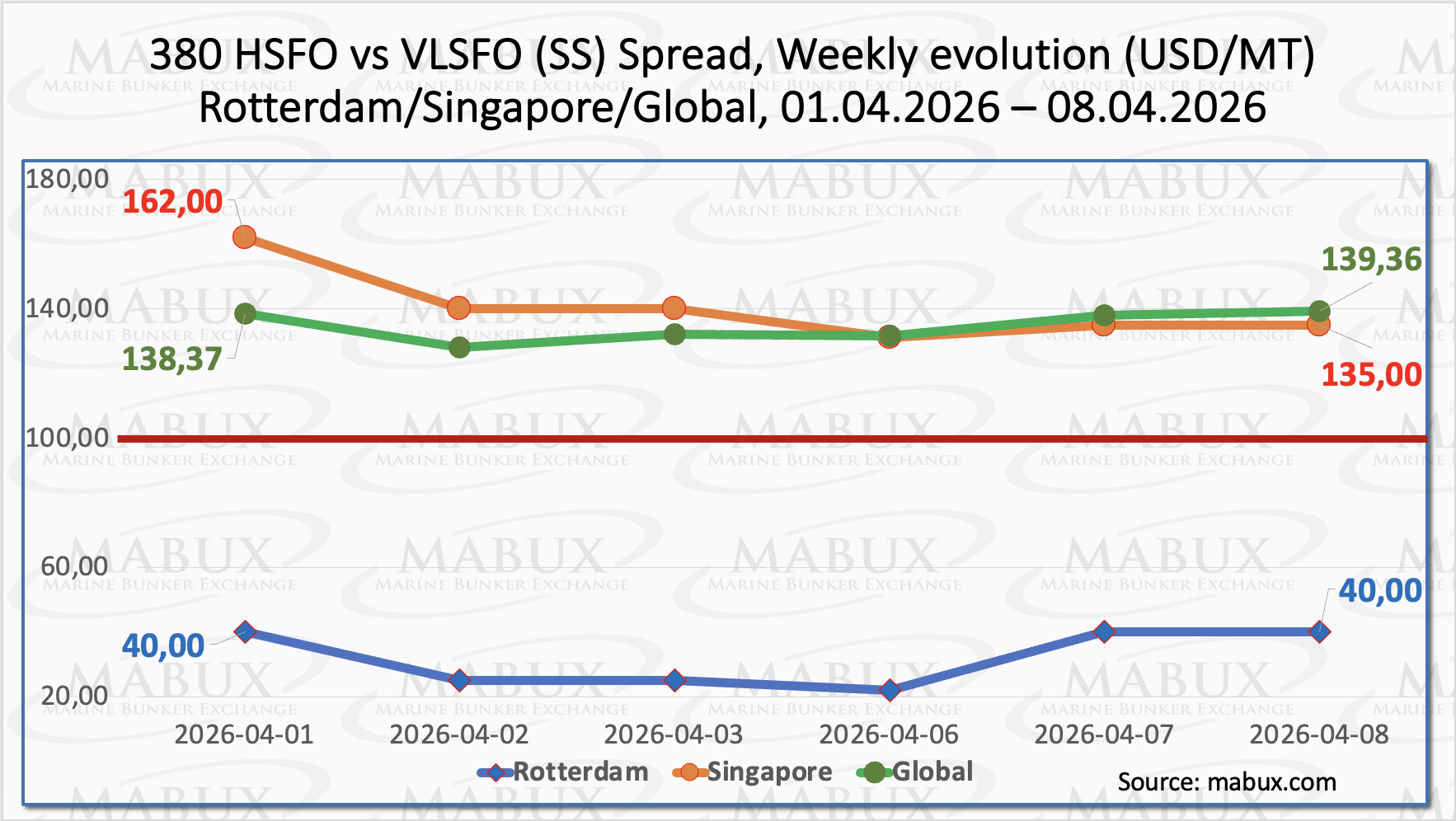

The MABUX Global Scrubber Spread (SS)—the price differential between 380 HSFO and VLSFO—edged up marginally by US$ 0.99, rising from US$ 138.37 last week to US$ 139.36, and remaining well above the psychological breakeven threshold of US$ 100.00. However, the weekly average of the index declined by US$ 9.95, indicating underlying weakening momentum. In Rotterdam, the SS Spread remained unchanged at US$ 40.00, although it briefly narrowed to US$ 22.00 during the period.

The port’s weekly average spread also decreased by US$ 12.67, reflecting a softening trend. In Singapore, the SS Spread contracted more significantly, declining by US$ 27.00 from US$ 162.00 last week to US$ 135.00, with an intraperiod low of US$ 131.00. The weekly average spread in the port also dropped by US$ 28.00. “We expect the spread to continue narrowing in the coming week,” Ivanov added, pointing to sustained corrective pressure across the market.

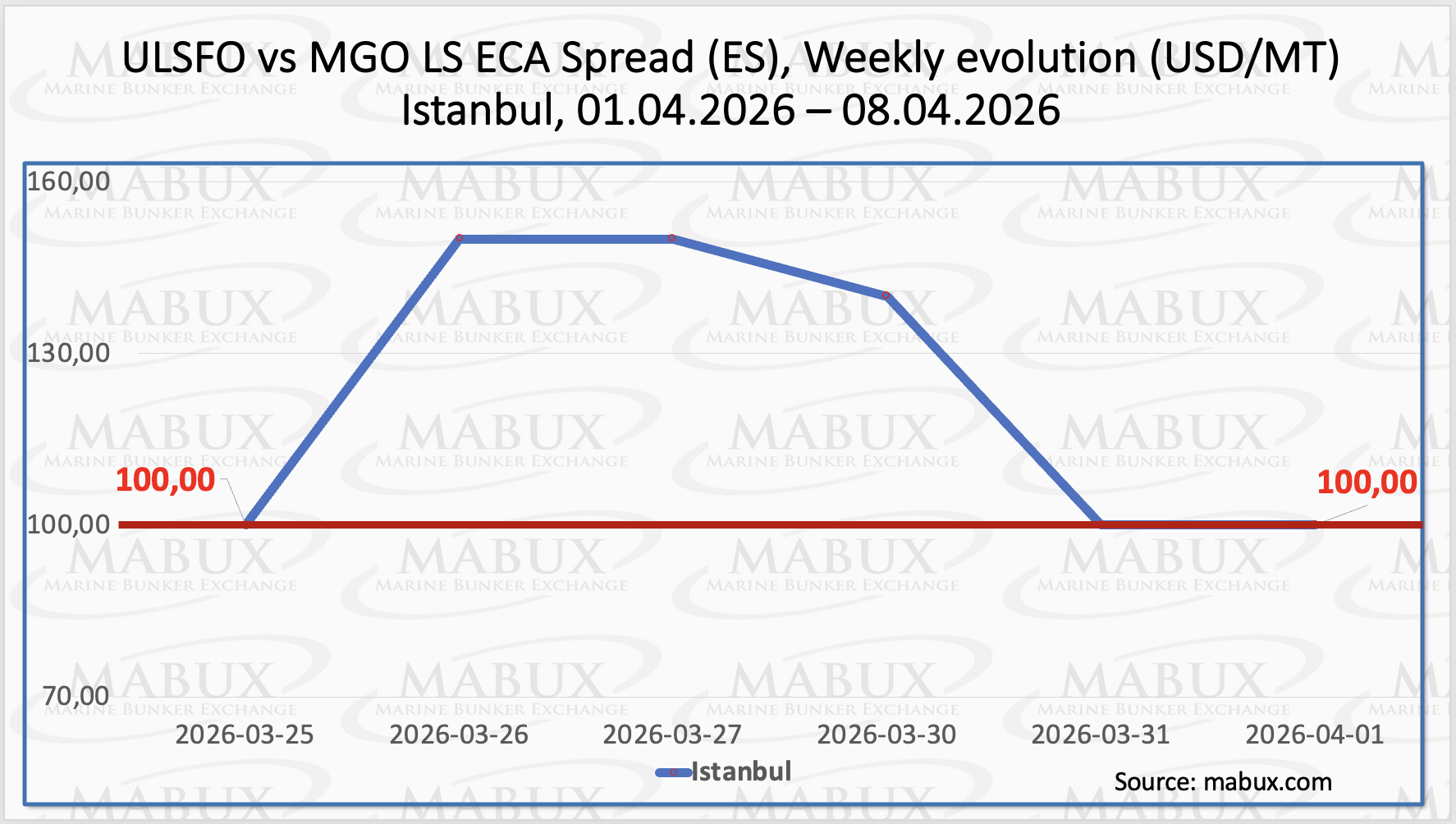

The Istanbul ECA Spread (ES) remained unchanged over the week at US$ 100.00, despite peaking at US$ 150.00 amid heightened market volatility. The weekly average declined by US$ 10.00, indicating a partial easing of upward pressure. The Venice ECA Spread remains temporarily suspended due to the absence of consistent market quotations. Amid the ongoing de-escalation of tensions in the Middle East, the ECA Spread is expected to hold near current levels in the short term.

The ongoing military standoff in the Middle East continues to exert upward pressure on the EU gas market. A significant share of European gas imports originates from Persian Gulf producers, particularly Qatar. However, supply flows have been disrupted by Iranian attacks on regional energy infrastructure, with growing concerns that volumes may not fully recover even in the event of a near-term de-escalation.

At the same time, tightening inventory levels are increasing the sensitivity of both European and Asian markets to weather-related demand fluctuations and unplanned outages. The spot market is also showing signs of reduced liquidity, as market participants increasingly shift toward the relative security of long-term contractual arrangements.

As of April 7, the level of natural gas in European underground storage facilities recorded a marginal increase for the first time since the beginning of the year, reaching 28.61% of total capacity (+0.56 percentage points week-on-week).

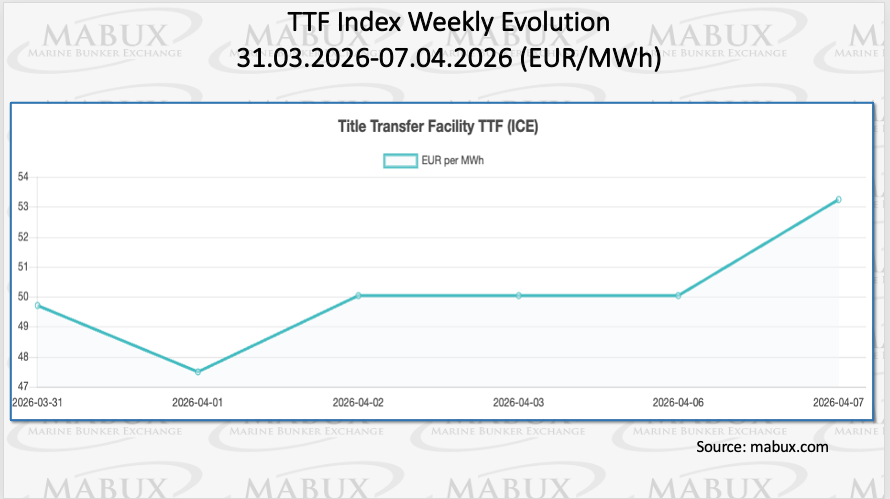

Despite this uptick, storage levels remain significantly lower—by 32.85%—compared to the level observed on January 1, 2026 (61.46%). At the end of Week 15, the European gas benchmark TTF posted a notable increase, rising by EUR 3.547/MWh to EUR 53.247/MWh, compared to EUR 49.700/MWh the previous week, thereby moving back above the EUR 50.00/MWh threshold.

The price of LNG as a bunker fuel at the port of Sines (Portugal) declined by a further US$ 163.00 this week, falling to US$ 1,149/MT from US$ 1,312/MT the previous week. At the same time, the price differential between LNG and conventional fuel continued to widen significantly, reaching US$ 476 in favor of LNG (compared to US$ 195 a week earlier). As of April 6, MGO LS was quoted at US$ 1,625/MT at the port of Sines.

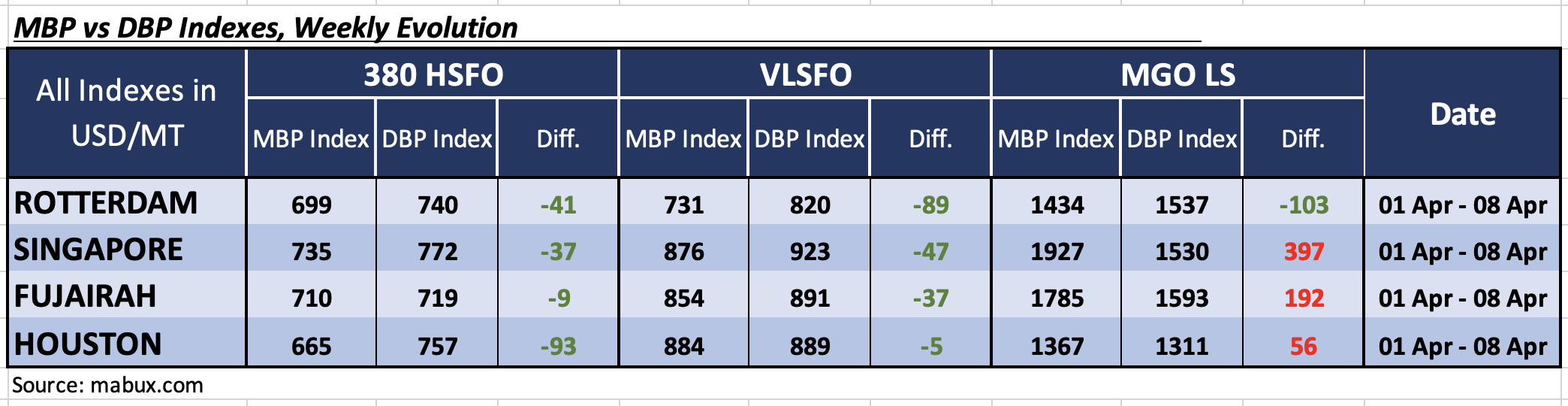

Amid the ongoing Middle East conflict, the MABUX Market Differential Index (MDI)—which reflects the ratio between market bunker prices (MBP) and the MABUX digital bunker benchmark (DBP)—displayed a clear shift in valuation dynamics across the world’s biggest hubs: Rotterdam, Singapore, Fujairah, and Houston:

• 380 HSFO segment: Fujairah and Houston moved back into the undervalued zone, resulting in all four ports being assessed as undervalued. Discount levels widened by 36 points in Rotterdam, 53 points in Fujairah, and 143 points in Houston, while Singapore recorded a marginal contraction of 7 points. Notably, Fujairah’s MDI approached full (100%) correlation between MBP and DBP.

• VLSFO segment: Fujairah and Houston similarly shifted into undervalued territory, joining Rotterdam and Singapore. The MDI discount increased across all ports: by 52 points in Rotterdam, 29 points in Singapore, 53 points in Fujairah, and 116 points in Houston. Houston’s MDI also approached near full (100%) correlation between MBP and DBP.

• MGO LS segment: Rotterdam returned to the undervalued zone, becoming the only port in this category assessed as undervalued, with the average discount widening by 116 points. The remaining three ports were overvalued. However, overvaluation levels declined by 69 points in Singapore and 89 points in Fujairah, while Houston recorded a 15-point increase.

“Following the ceasefire announcement, valuation dynamics have shifted notably toward undervaluation,” Ivanov commented. Following the announcement of a two-week ceasefire in the Middle East, MDI dynamics have increasingly shifted toward undervaluation, particularly in the 380 HSFO and VLSFO segments. We expect this undervaluation trend in bunker fuels to persist into the coming week.

“The ceasefire has reversed the previous upward momentum, but the outlook remains fragile,” Ivanov said. The two-week ceasefire agreement reached on April 8 in the Middle East conflict zone has reversed the downward trend in the global bunker market. We expect that bunker indices may resume their decline in the near term, provided all parties adhere to the agreed terms. Conversely, any violation of the ceasefire could trigger a renewed upward movement in prices.